144th Edition: February 2026

Key Points:

- Australian live feeder prices have now pushed above Indonesia’s effective government price cap.

- Indonesia again carried the bulk of 2025 volumes, but the Philippines and new breeder markets added welcome depth.

- Rising feeder prices are pushing exporters to focus more heavily on higher-margin breeder and dairy cattle.

Regional Trends and Overview

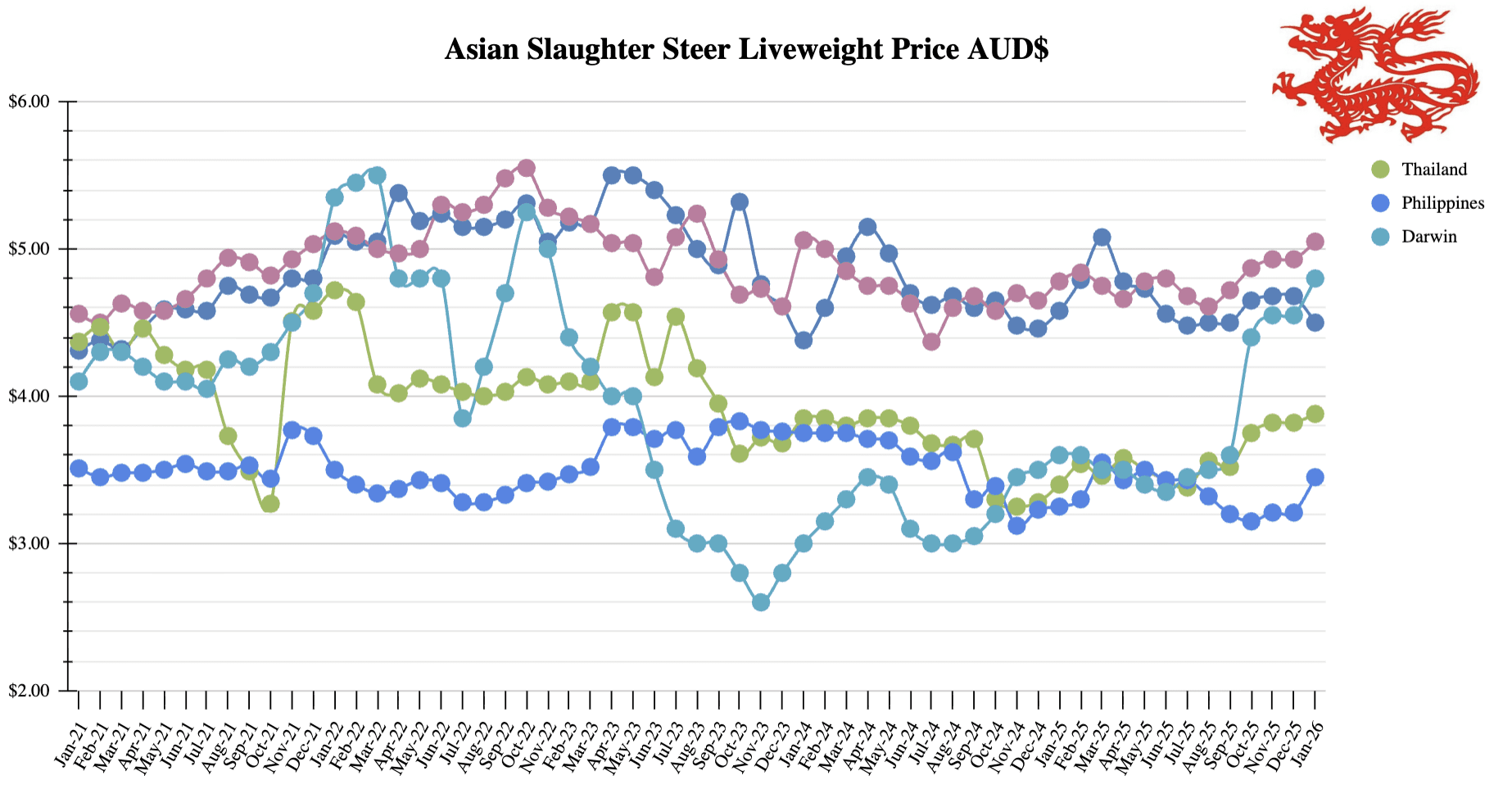

Regional Price Graph

2025 delivers strong volumes across a widening market base

By most measures, 2025 was a strong year for Australian live cattle exports.

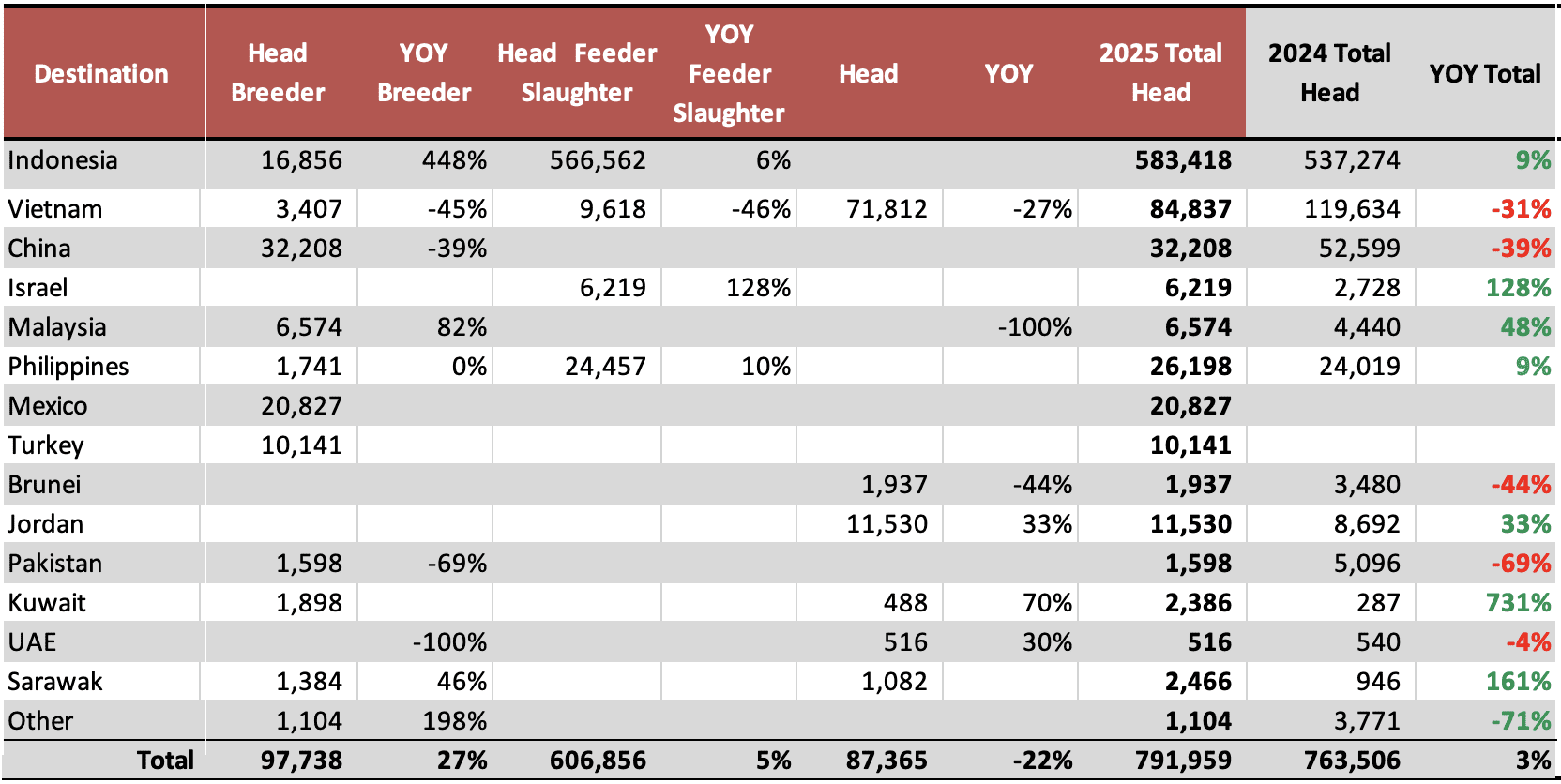

Total shipments lifted to just under 792,000 head, up around 3 percent, with solid momentum across multiple categories and the welcome addition of new breeder markets.

Dr Michael Patching

Indonesia again led the way, taking more than 583,000 head, but the year was not just about one market.

The Philippines continued to firm as an important secondary destination and arguably the Southeast Asian market with the most upside, while breeder flows diversified meaningfully beyond the traditional pathways.

Turkey emerged, importing 10,141 head across three shipments, while Mexico took 20,827 breeders over five shipments, adding depth and resilience to the overall export task.

While rising Australian cattle prices may mean 2025 proves close to the peak volume year of this cycle, the trade has shown it can still place cattle into a wider mix of markets when the fundamentals align.

The ability to move both feeders and breeders across multiple regions has underpinned volumes and helped smooth some of the volatility that comes with price-driven feeder demand.

Table: Total cattle exports by sea 2025 and 2024 calendar years Data source: DAFF website

Exporters shift focus as breeder margins attract attention

What also stood out through 2025 was the growing attention exporters are paying to the breeder trade. Indonesia continues to deliver impressive feeder volumes, but it remains a highly competitive, tightly managed market with relatively narrow margins and increasing political oversight. Breeders, by contrast, typically offer much larger margins, even if shipments are more sporadic and client relationships harder to repeat. That margin differential is becoming harder for exporters to ignore as feeder cattle prices rise and selling prices in some markets remain capped.

Within that breeder space, dairy continues to stand apart. Dairy cattle have long provided repeat customers in China, and that same pattern is now emerging more clearly in Mexico and, in smaller volumes, Indonesia. Unlike beef breeders, dairy programs are often tied to longer term production strategies rather than short term price cycles, giving exporters a more reliable pipeline when relationships are established. It is still a more complex and selective trade, but as the feeder market becomes more competitive and margin constrained, it is no surprise more exporters are turning their eye to breeders as a way to balance risk and returns heading into the next phase of the cycle.

Indonesia: Slaughter Steers $4.50 AUD per kg live weight (IDR 11,829 = $1 AUD)

Prices

Indonesian live cattle prices have firmed marginally, led by small gains in Lampung, while Java continues to command a premium over other regions.

In Lampung, bull and steer prices are around IDR 1,000/kg higher, now trading at IDR 51,000–52,000/kg (AUD 4.33–4.41/kg), with heifers lifting to about IDR 50,000/kg (AUD 4.24/kg). On Java, bulls and steers are currently priced at IDR 53,000–54,000/kg (AUD 4.50–4.58/kg), while heifers remain steady near IDR 51,000/kg (AUD 4.33/kg).

The ongoing strength in Java prices reflects higher CIF costs following the lift in Darwin feeder prices in October last year, which is now flowing through for cattle completing their 120 days on feed.

Photos: Wet market beef sales at Yogyakarta

Australian live feeder price now above Indonesian government cap

Butcher and meat trader protests in Jakarta in late January were another reminder of how politically sensitive beef pricing has become. The government’s rapid restatement of the Rp 55,000/kg liveweight reference price at feedlot level (around AUD $4.65/kg) helped cool things down, but it also laid bare the problem. Current Australian live export steer prices are sitting around $4.80/kg here in Australia, compared with $3.55/kg at the same time last year. At today’s exchange rate, that equates to roughly Rp 56,800/kg before a single dollar of freight, financing or import cost is added. In other words, the Australian cattle price alone is already above the Indonesian market cap before the animal steps hoof on the boat.

The political sensitivity in Indonesia around beef prices is not new. The memory of the 2016 cartel case, when 32 companies were fined a combined IDR 107 billion, still sits in the background and helps explain why feedlotters moved so quickly to fall back into line. What matters more now is the position Indonesian feedlotters find themselves in. They are structurally geared to Australian cattle, because local cattle cannot be aggregated in sufficient numbers and the domestic herd has been badly depleted by disease in recent years. Those who have invested heavily in infrastructure, biosecurity and compliance should, in theory, be rewarded for supplying the only large-scale, reliable, disease-free cattle source into a market that still depends on fresh beef.

Instead, the numbers no longer work. Feedlotters have often imported cattle on thin or negative trade margins and relied on feeding performance to make it stack up, but that model needs some room between purchase and selling prices. With Australian cattle prices rising and selling prices capped, that room has disappeared.

Meat importers can switch origins when prices move; live cattle feedlots cannot. That imbalance is now at the centre of the strain showing up on Jakarta’s streets.

Brazil shows how quota access is now won

The structure of Indonesia’s 2026 beef import quotas also makes more sense when viewed through a political lens rather than a purely commercial one. State owned enterprises have been allocated 250,000 tonnes, including 100,000 tonnes of Indian buffalo meat, 75,000 tonnes of boxed beef from Brazil, and a further 75,000 tonnes from other suppliers including Australia, the US and New Zealand, while private importers have seen their allocation slashed from 180,000 tonnes last year to just 30,000 tonnes. That outcome did not happen in a vacuum.

Brazil’s President Lula da Silva personally visited Jakarta in late 2025, with beef and food security clearly on the agenda, backed up by follow-on engagement from senior Brazilian agriculture officials. In an era where President Prabowo, like many global leaders, is taking a hands-on role in managing import volumes and food prices, that sort of direct, head of state level lobbying matters.

A few well timed conversations with the decision maker at the top can outweigh years of quiet trade. For those watching from Australia, it is a reminder that access is increasingly shaped as much by diplomacy as by competitiveness, and that countries willing to do the political work are often the ones that get the quota.

Photos: Presidents Prabowo and Lula strengthen Indonesia–Brazil cooperation in Jakarta talks.

Rupiah breaks a long-held range

One of the more important shifts of the past couple of months has been the Indonesian rupiah breaking out of its long-held range against the Australian dollar.

For nearly 15 years the IDR mostly sat around 10,000 to the AUD, a period that coincided with the most stable and reliable phase of Australian live cattle supply into Indonesia. The move to around IDR 11,789 to the AUD is different, because it directly alters the economics of the trade.

Cattle are bought in Australian dollars and rolled into a USD CIF price alongside freight, but cattle remain by far the dominant cost. A weaker rupiah against the AUD therefore flows straight into higher landed costs in local terms, compounding the impact of already higher Australian live export steer prices and tightening margins for Indonesian importers at the worst possible time.

KITA SEHAT quietly embeds animal health into Indonesia’s health reform

The KITA SEHAT program is now formally underway after being signed in August 2025 as an AUD 100 million, eight year Australia–Indonesia partnership. While the focus remains human health, animal health system strengthening is now clearly written into the design, including surveillance, laboratory capacity and workforce development, rather than being treated as a narrow zoonoses add-on.

Ordinarily this is the kind of program that would barely rate a mention in a Beef Central market report, but with LSD and FMD sitting just to our north, these slow, unglamorous investments in animal health systems start to matter a great deal more.

Vietnam: Slaughter Steers $4.61 AUD per kg live weight (VND 17,234 = $1 AUD)

Shrinking ESCAS abattoir capacity limits any upside when prices turn

One of the more worrying developments in Vietnam is how far ESCAS slaughter capacity has contracted. An industry source told me there may now be fewer than 30 active ESCAS abattoirs operating nationally, down from a peak of more than 200. While volumes into Vietnam have always been driven mainly by price, slaughter capacity for Australian cattle is increasingly the real constraint. Once that capacity disappears, it is proving very difficult to rebuild.

A decade ago, ESCAS facilities could come on quickly when the numbers stacked up. Compliance was simpler, capital requirements were lower and approvals faster. That has changed. Tighter waste management, food hygiene and animal and human health requirements mean reopening or building abattoirs is now slower, more expensive and more complex. Vietnam will still respond when Australian cattle prices cycle lower, but with prices unlikely to ease soon, there is little incentive to reinvest. The risk is that when cattle do become competitive again, rebuilding these supply chains will be far harder than it was ten years ago.

Substitution continues to undermine wet market confidence

Food fraud is another ongoing risk hanging over wet market beef sales in Vietnam, and it is one I have been conscious of for many years during my time working in the market with MLA.

The recent arrests in Ho Chi Minh City of a group producing fake beef from pork, using blood and banned chemicals to imitate colour and texture, are simply the latest example of what the trade commonly refers to as “substitution”. This is not a new problem.

It has been a persistent challenge to consumer confidence and to the perception of meat quality in traditional markets, where traceability is limited and enforcement uneven. Each incident reinforces doubts about what is really being sold as beef, and over time that erodes trust in wet market channels that have historically underpinned demand for live cattle and fresh slaughter.

Photos: Pork and beef are commonly sold side by side in Vietnam’s wet markets, often with a significant price gap between the two.

Philippines: Slaughter Steers $3.45 AUD per kg Live weight (₱41 = $1 AUD)

Prices

Livestock prices in the Philippines are still tracking sideways, with only modest adjustments across categories.

Wet market beef knuckle has softened slightly to ₱350 per kilogram ($8.50 AUD), while supermarket beef knuckle has edged higher to ₱415 per kilogram ($10.07 AUD). Slaughter steer prices have moved up more noticeably to around ₱121 per kilogram (about $2.94 AUD), while pork carcass values have firmed to ₱240 per kilogram ($5.83 AUD).

In poultry, supermarket broiler prices have lifted to ₱170 per kilogram ($4.13 AUD), while branded products such as Magnolia have eased back to around ₱247 per kilogram ($6 AUD). Overall, conditions remain stable, with supply well matched to demand and no strong signals yet pointing to a change in price direction.

Photos: Local meat and livestock sales in Mindanao

BAI boosts cattle breeding through artificial insemination

The Philippines’ Bureau of Animal Industry (BAI) has distributed cattle semen to village-based artificial insemination technicians in Tarlac under the Department of Agriculture’s Unified National Artificial Insemination Program (UNAIP).

The initiative aims to improve the genetic quality of local cattle herds by expanding access to artificial insemination services at the village level. By training and equipping technicians closer to farmers, the program is designed to lift productivity and incomes among small-scale cattle raisers, who make up the bulk of the national herd.

The move comes as the Philippines continues to rely heavily on imported beef, with domestic production constrained by herd size and limited breeding efficiency.

Australia: Feeder Steers Darwin $4.80

On the Australian side, December saw a sharp lift in shipments, with 72,192 head exported to Indonesia as importers alike moved to stock up ahead of Eid and the usual pause associated with Indonesia’s January import permit process.

That front-loading reflected both seasonal demand and a degree of caution after the disruptions of recent years. Import permits were released relatively quickly in January, much to the relief of the trade, and after a brief lull, vessels have begun moving again over the past few weeks, restoring some momentum to the program.

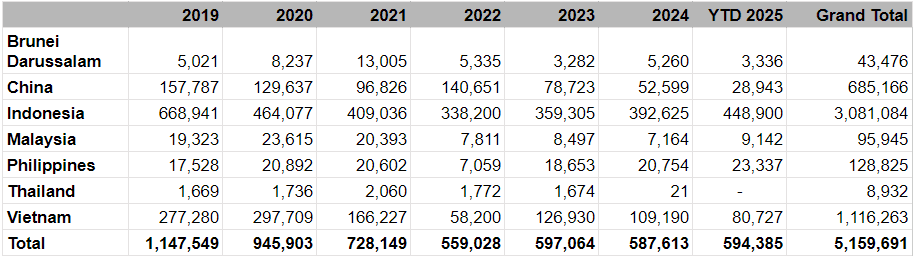

Year 2025 cattle exports – comparison across SE Asian markets

Source: DAFF website