132nd Edition: December 2024

Key points:

- SE Asia report to enter a new phase in 2025 as I move back to Perth

- The future of Indian Buffalo Meat(IBM) imports to Indonesia up in the air

- Cross-border cattle movement into Vietnam from Myanmar and Thailand continues, exacerbated by political instability and lax enforcement, increasing disease risks.

- Aussie dairy cattle expected to help with Philippines efforts to achieve 5% milk self-sufficiency by 2028.

A quick note to readers that I move back to Perth in a few weeks after 14 years abroad. The SE Asia report will continue with the network of contributors we have through the region and a number of ongoing projects, especially in Vietnam and Indonesia.

A quick note to readers that I move back to Perth in a few weeks after 14 years abroad. The SE Asia report will continue with the network of contributors we have through the region and a number of ongoing projects, especially in Vietnam and Indonesia.

I am looking forward to being on home soil in 2025, with a renewed focus on making animal welfare easier for livestock businesses and industry through Impetus Animal Welfare.

Looking back on 2024

The Southeast Asian livestock and beef trade in 2024 highlighted a region grappling with a growing need to secure protein supply, of which imported cattle and beef is a major component, and a desire to protect local producers. Political shifts, climate events, and persistent disease threats created a volatile environment, testing the resilience of supply chains and trade relationships.

Indonesia’s growing focus on food self-sufficiency, driven by their new President Prabowo Subianto, is emblematic of a broader regional desire to reduce import dependency, despite the reality of this being very challenging to achieve for many countries with limited capacity to increase their own livestock herds and production. While this type of agenda aims to bolster domestic industries, it also creates significant uncertainty for exporters to these markets navigating new rules, quotas, and preferences for local supply chains. Yet, for those who can align with these priorities—through investments in disease management, breeding programs or general food security support—there remains ample opportunity.

Vietnam’s reliance on cross-border cattle imports and the durability of trading networks in spite of movement restrictions illustrate the gaps in the region’s regulatory frameworks. These issues, combined with rising demand and limited local production capacity, highlight a structural challenge: how to balance growth with biosecurity and traceability. Conversely the Philippines’ investment in dairy infrastructure signals an increasing willingness among regional players to take the long view, prioritising resilience over short-term gains.

For the Australian industry, 2024’s greatest lesson may be the importance of being seen not just as a supplier but as a partner in regional development. Whether through improving disease management, investing in local supply chains, or offering technical expertise, the key to enduring relevance lies in helping Southeast Asia navigate its complex transformation.

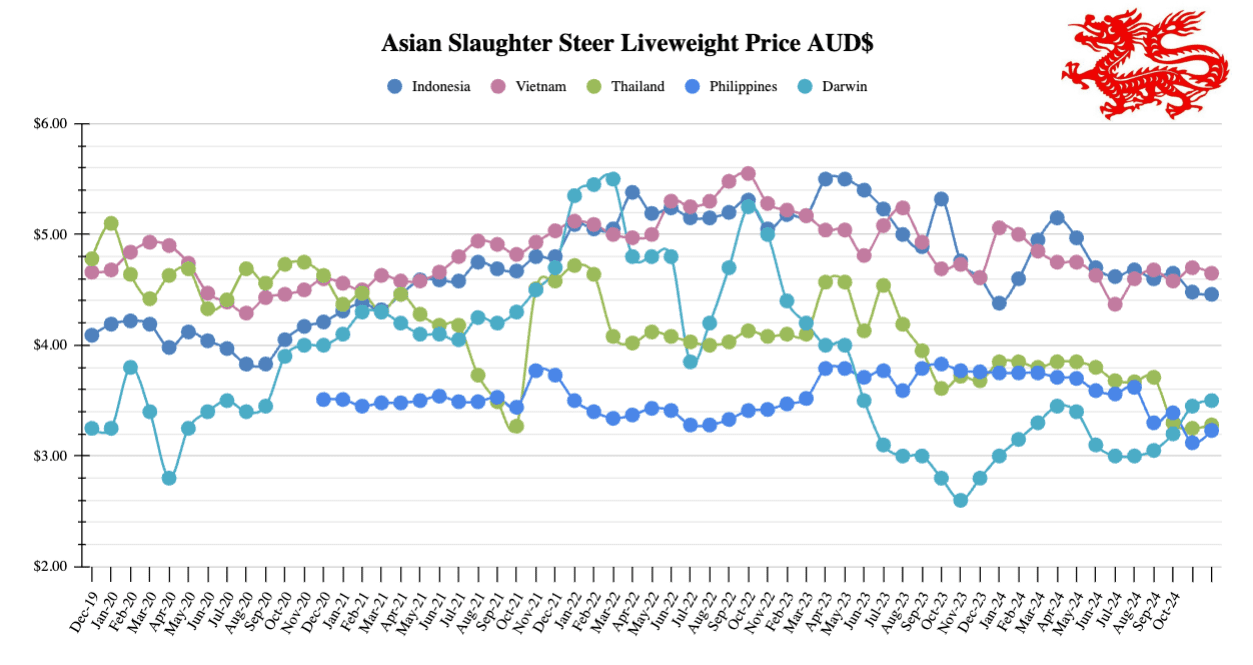

Indonesia: Slaughter Steers $4.46 AUD per kg live weight (IDR 10,344 = $1 AUD)

Beef Prices

Beef and carcass prices have barely moved, sitting at around IDR 130,000 ($12.57 AUD) and 90,000 ($8.70 AUD) respectively. The price of broiler chickens is averaging around IDR 36,000 ($3.48 AUD) per kg, down very slightly from last month.

Two priorities are taking the focus of Australian exporters of live cattle and beef to Indonesia. One is the concern over the timing of import permit releases in 2025. The other is 2025 quota’s for the import of Indian Buffalo Meat(IBM), and which organisation will be given the role of distribution. For several years Bulog, which has been responsible for food distribution and price controls, has held the role and by the numbers has been successful in filling its quota most years. In 2024 the role was handed to PT Berdikari and PT Perusahaan Perdagangan Indonesia (PPI) who appear to have not utilised those permits fully, with IBM imports down substantially. The effect on the market in 2024 has been mitigated by a large backlog of product still working its way through the system from 2023, but if the situation continues it could open the door for importers of Australian cattle to claw back some market share. The Indonesian government has recently stated that it is considering Bulog’s future purpose and considering reforms which would see Bulog report directly to President Prabowo and play a larger role in food supply and price control.

Prabowo’s Reforms Shape Agricultural Policy and Trade Outlook

Indonesian President Prabowo Subianto has fast-tracked his food self-sufficiency target from 2028 to 2027—a highly ambitious timeline considering the scale of reforms proposed. Central to his plan is the Free Nutritious Meal (MBG) program, which aims to deliver benefits to 80 million Indonesians by 2027. This is being supported by sweeping changes like streamlined fertiliser distribution and an overhaul of state enterprises, including Bulog. This may speed up the government’s plans to import large numbers of beef and dairy cattle to support the MBG program.

It also looks like the Indonesian Ministry of Agriculture (MoA) has reinstated the requirement for feedlot operators to import 3% of their capacity as breeding cattle. Paused during the COVID-19 pandemic, this policy is aimed at bolstering the nation’s cattle population for both beef and dairy production and has created headaches for beef cattle importers and exporters to comply with while remaining profitable.

Dairy and Sheep Meat Reforms

Indonesian media is reporting that the government has stopped issuing sheep carcass and lamb import recommendations which is one step in the process to import meat. They cite concerns over cheaper imports undercutting domestic prices. Surprise warehouse inspections and a new requirement for importers to periodically report their stock inventories signals the government’s intention to keep a tight hold on import volumes.

Protests from dairy farmers have prompted new rules requiring importers to source fresh milk locally as part of their quotas. While benefiting from duty-free imports under the ASEAN-Australia-New Zealand Free Trade Agreement (AANZFTA), the government is now reversing policies from the 1997-1998 IMF-mandated reforms, which saw milk imports surge from 40% to 80% of consumption. Agriculture Minister Amran Sulaiman has called this a “turning point” for the dairy sector, aiming to reduce reliance on imports.

Both of these moves indicate that the newly formed government will take an active role in trade and food security, following the long term trend of trade policies aimed at protecting local producers.

Pressures from VAT Hike and Trade Competition

A planned VAT increase from 11% to 12% set for January 2025, has raised concerns across the agricultural sector in Indonesia. Farmers and local producers, already under pressure from rising input costs and import competition, could face further challenges as consumer purchasing power weakens. The hike is expected to drive up costs for key inputs such as feed and fertilisers, both of which are major cost drivers for cattle feedlotters.

Vietnam: Slaughter Steers $4.65 AUD per kg live weight (VND 16,493 = $1 AUD)

The grey trade and black market trade of cattle through the Mekong region is getting more dangerous and more lucrative. The ongoing civil conflict in Myanmar, which erupted after a military coup in 2021 ousted Myanmar’s democratically elected government, has exacerbated the situation, forcing traders to rely heavily on illicit networks to move cattle across borders. Expensive and complex controls at many borders force local producers to sell to middle-men who know how to bypass these controls, or who have found work-arounds to documentation requirements, sometimes claiming cattle are locally bred once they arrive in a destination country, but had not yet been registered. The journey, which can span several days on a truck while the traders wait for the right time to move, often leaves the cattle weakened and more susceptible to illness, heightening the risk of disease transmission along the trading routes. Trading remains strong along these routes with Mynamar and Thai cattle readily available in Vietnam.

Philippines: Slaughter Steers $3.23 AUD per kg Live weight (P38.20 = $1 AUD)

Prices

The Australian Dollar has shown slight movement against the Philippine Peso, softening from P38.53 to P38.20 over the past month. In wet markets and supermarkets the beef rump prices sit at about P450 per kg ($11.78 AUD). Local cattle prices in Mindanao are still around P123 per kg ($3.22 AUD) live weight, and the hot beef meat price is approximately P310 per kg ($8.11 AUD).

Live pork prices are around P200 per kg ($5.23 AUD), and pork carcass goes for P260.00 per kg ($5.81 AUD). In wet markets, non-branded broiler chicken is priced at P180.00 per kg ($4.71 AUD), while in supermarkets, the Magnolia brand is priced at P230.00 per kg ($6.02 AUD).

Photos: Local meat and livestock sales in Mindanao

National Dairy Authority Drives Milk Sufficiency Goals

The National Dairy Authority (NDA) is advancing its agenda to achieve 5% milk sufficiency by 2028 under the Marcos administration. Efforts include importing dairy cattle for multiplier farms, artificial insemination programmes, and improving cattle nutrition. NDA Administrator Marcus Antonius Andaya reported that 600 dairy cattle from Australia are expected to arrive by mid-2025, with additional imports planned. Currently, only 1.54% of the country’s milk demand is met locally.

Australia: Feeder Steers Darwin $3.50

There is a rush of boats and cattle out of Darwin as Indonesian importers continue to fill their feedlots ahead of the uncertain period at the start of 2025 where they may have to wait for import permits to be issued. Many feedlots are already well stocked as they begin their 120 day feeding regimes leading in to Ramadan and Eid al Fitr in February and March 2025. Producers will be enjoying the interest from exporters which has pushed prices to their highest in six months and more than 15% higher than the same time last year.

Year 2024 to November for cattle exports – comparison across SE Asian markets

Source: DAFF