115th Edition: August 2023

Regional Livestock Movements and Trends

This section is normally dedicated to commentary on the unofficial channels of cattle movements within Asia and their impact on disease and livestock prices through the region. This month the focus has drastically shifted to official channels from Australia into the region due to the suspensions relating to LSD detections of Australian cattle in Indonesia.

As has already been well reported on Beef Central and other media sources the positive test results for Lumpy Skin Disease (LSD) from some Australian cattle has resulted in the suspension of trade with four Australian quarantine depots into Indonesia and more recently a suspension of trade of cattle to Malaysia.

The Australian authorities claim that the cattle would likely be positive due to vaccination or local infection. The vaccination argument is less likely to be accepted by Indonesia as it appears the cattle were observed with infection on arrival, and more cattle have subsequently been detected at the port. This is likely to continue to complicate issues for trade as being able to prove the origin of the infection will be difficult if Australia continues to test negative.

According to Indonesian reporting, Australia was given 60 days to demonstrate LSD freedom before more widespread suspensions were put in place. Australian sources claim that they are well on the way to demonstrating this but there has been little reported on what this involves or the ramifications of the recent detections.

The Malaysian Department of Veterinary Services (DVS) has instructed Malaysian Quarantine and Inspection Services (MAQIS) not to approve import permits for live cattle and buffalo from Australia effective August 4th although there is a ship on the water at present. An announcement by Australia’s Chief Veterinary Officer Mark Schipp on Wednesday rightly points out that this move does not imply Australia has LSD.

So what is going on from an Indonesian and Malaysian perspective given they both have the disease?

There does not appear to be any direct political motivation behind the suspension, it appears to be genuinely for disease risk mitigation reasons although some clarifications are made on this in the Indonesian section, so read on. ‘But Malaysia and Indonesia both have the disease already?’ I hear you ask…

We tend to forget that every nation in the world is on a development pathway and we need to give the region more credit for the genuine desire to increase their disease preparedness and have effective biosecurity control in place. Remember, Indonesia previously obtained FMD freedom in 1986 and Philippines in 2005 and if you track FMD status then most nations in the region are positively moving through the WOAH FMD disease status, so there is a strong regional priority for biosecurity even though it may not appear so from the outside. Most importantly, disease status has economic impacts in productivity and limits the ability to export products. And political implications for farmers that have lost their income. So there is a strong desire to control disease.

We tend to forget that every nation in the world is on a development pathway and we need to give the region more credit for the genuine desire to increase their disease preparedness and have effective biosecurity control in place. Remember, Indonesia previously obtained FMD freedom in 1986 and Philippines in 2005 and if you track FMD status then most nations in the region are positively moving through the WOAH FMD disease status, so there is a strong regional priority for biosecurity even though it may not appear so from the outside. Most importantly, disease status has economic impacts in productivity and limits the ability to export products. And political implications for farmers that have lost their income. So there is a strong desire to control disease.

From an overseas perspective, market access limitations are a relatively normal situation. The Philippines have just lifted a ban on Japanese, Czech, and Hungarian poultry imports due to the fear of importing avian influenza even though the Philippines have had reports since early 2022. It is Australia’s responsibility to demonstrate freedom, the fact that we have also been locked out of Malaysia suggests that we are not doing enough in the region to assure our status, rather than just spruik our credentials.

The risk that Australia faces is that we only operate in the ‘official trade’ sphere. Politically this has meant that our regulations like ESCAS, and our food safety credentials etc have enjoyed widespread support and consequently we have seen a period of improved trade access. But official trade is the easiest (only) part of the trade that can be effectively regulated. So it is logical that these same credentials would be more exposed to observation and scrutiny. This is especially true as the countries try to improve their integrity systems, improve their disease response, and most importantly demonstrate to the international and local farmers that they are capable of rising to the challenge.

In the last 12 months Indonesia has been faced with African Swine Fever (ASF), Foot and Mouth Disease (FMD), LSD, and a current anthrax outbreak in Central Java. There is significant pressure to use this to demonstrate they are successful, especially in an election year.

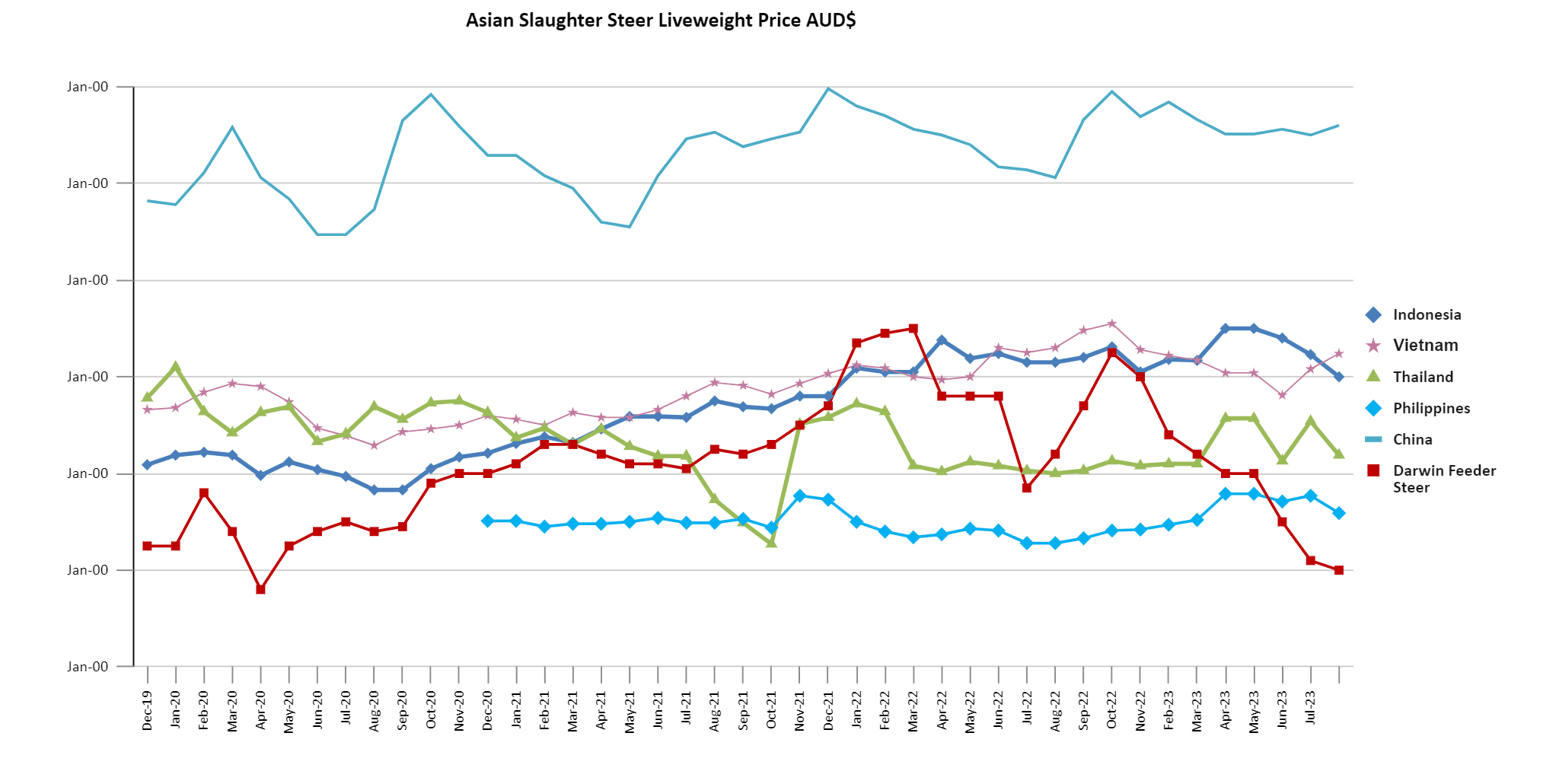

Indonesia: Steers AUD $5.00 / kg live weight (IDR 10,011.47 = 1 AUD)

In the regions of Jakarta and West Java, there has still been a slight decline in prices for both carcass and live cattle since Eid al-Adha last month. The price for Australian steers is between 48,500-50,000 IDR per kilogram live weight, with the carcass price at 100,000-102,000 IDR per kilogram.

Despite the decrease in prices and uplift in imports, there has still not been a significant increase in the volume of slaughter observed in Indonesian abattoirs. One of potential reasons is because of the rise in chicken consumption compared to July. Broiler chicken price per kilogram in the market has decreased last month from 45,000-50,000 IDR/kg to 36,000-37,500 IDR/kg on average. Drop in local corn prices compared to imported wheat prices are reducing feed costs and would be contributing to the cost reduction. The LSD issue is no doubt going to impact importer confidence, especially with the potential risk of a wider suspension looming.

The beef prices at the supermarkets and wet markets have been stable with no significant increase or decrease across the islands of Java and Sumatra.

Indonesia continues to navigate a complex landscape of disease risks, economic considerations, and animal welfare concerns. The decision to cease trade with Australia over the LSD issue demonstrates their desire to control disease risks as discussed already. However at the same time there is mounting pressure at a political level with the Indonesian Coordinating Minister for Maritime Affairs and Investment and the Head of the Quarantine Department at the Indonesian Ministry of Agriculture (MoA) both calling for increasing imports of cattle and meat from countries with known disease status. There has been an Indonesian delegation to Brazil which signed off on protocols for Brazilian cattle imports, and a similar push for a protocol for cattle to come from South Africa. It is important to note that this does not mean there will be imports from these countries as the economics of such a shipment still don’t make sense, especially given significant reductions in the cost of Australian cattle. But it does signal intent. This direction continues to raise critical questions in Indonesia about risk assessment and transparency for disease in a time where the government is clearly pushing for greater supply diversification to improve food security.

Ending the Dog and Cat Meat Trade

In a landmark decision, the regional secretary of the city of Tomohon, Indonesia announced on July 21st the cessation of the dog and cat meat trade at the Beriman Wilken Market (Tomohon Extreme Market) in North Sulawesi. The decision was marked by the evacuation of 25 dogs and three cats from the market. This significant move follows persistent efforts by local activists, organisations such as Humane Society International (HSI), Animal Friends Manado Indonesia (AFMI), and national and international celebrities to end this trade. The decision aligns with the broader movement to promote more hygienic and ethical animal food sources and showcases the country’s effort to move towards ethical and hygienic food sources, reflecting broader global shifts in attitudes towards animal welfare and public health and the growing impact of animal advocacy groups in Indonesia.

The Tomohon Extreme Market dog meat processing. Photo credit Theodora Sutcliffe

Vietnam: Steers AUD $5.24 / kg live weight (VND15,749 = 1AUD)

Price for Australian cattle into abattoirs in Vietnam has not changed in the last month, the only shift in price is due to exchange rate changes. Price for steers remains at VND 76,000-82,000 /kg liveweight and bulls from VND 83,000-84,000 /kg liveweight. Hot beef sold into wet markets is still wholesaling at around VND 205,000 (AUD $13).

I was fortunate to spend a week in Vietnam in the last month. It was great to see familiar faces and see what is happening in the country first hand, but since my last visit a few months ago it is becoming increasingly clear that the return to pre-COVID trading conditions is not likely in the short term. Near Hanoi I visited an abattoir that previously slaughtered over 25 per night (a good number for Vietnam) on a regular basis and was an important abattoir for many exporters. It is now only slaughtering 7 per night and the abattoir owner was quite despondent. Before COVID he had built a new processing floor in a shed next to the current abattoir, it is 95% finished and would improve slaughter output and processing quality but he just doesn’t have the energy in the current market to complete the job.

Near completed Vietnamese abattoir not commissioned due to impact of COVID and local slaughter volume downturn. Photo credit Michael Patching

The future of the trade to Vietnam will likely come from investment into a similar model as Thailand and the Philippines where companies are investing in closed loop supply chains (or similar hybrid models) to secure a niche market for consistent quality locally processed direct to specific customers. Unfortunately in Vietnam there are limited options for companies that are willing to co-invest in this approach and there are difficulties in making this transition for cut utilisation with low volume processing and no export markets.

Philippines: Slaughter Steers AUD $3.59 / kg liveweight (P. 36.2 = 1AUD)

Wet market and supermarket beef has remained constant at around P. 560/kg and P. 600/kg retrospectively for beef knuckle. Slaughter steer prices remain between P.130-145 /kg liveweight in Mindanao and hot carcass meat is around P.260 /kg.

Chicken prices into supermarkets have dropped slightly over the last few months and pork remains relatively stable. The Philippines has a heavy reliance on Brazilian chicken exports and the continued spread of the highly virulent strain of avian influenza in Brazil may have a significant impact in the coming months if that impact is not contained.

Thailand Steers AUD $4.19 (Tb 22.69 = 1 AUD)

Local bull prices remain at the Tb 95/kg ($4.14 AUD). With still a large range of prices for local cattle in some feedlots.

There were enough Thai cattle seen in Vietnam to assume that some traders have now found a way to navigate the Laos-Vietnam border system. Although prices of Thailand cattle were up to AUD $0.10 more expensive than Australian cattle.

Reports emerged in the last month that there was a trade delegation moving from Laos into Thailand to look at supply of livestock into the official trade into China, through Laos. With LSD now endemic in the region this appears to be an even more difficult task as there is a long process involved to be able to comply with strict Chinese biosecurity requirements

Feeder Steers Darwin $3.10, Townsville $3.00

Feeder steers average price continues to be reported at around the $3.10 mark out of Darwin but there is the normal wide range in cattle prices reported due to quality. The most recent LSD detections in Indonesia will surely put a dampener on the demand for cattle for live export in a time where we were starting to see a small resurgence in volumes entering all markets.

Some increase in reported prices out of Townsville with Brahman feeder steer price increasing to $3.00 and bulls to $2.80.

2023 Year to July figures for sea freight across Asia for our different ports from the DAFF website. Note that these are updated as information is made available and so may not be official end figures.

| NT | QLD | VIC | WA | Grand Total | |

| Brunei Darussalam | 2,834 | 2,834 | |||

| China | 40,855 | 4,464 | 45,319 | ||

| Indonesia | 113,033 | 56,595 | 1,250 | 30,298 | 201,176 |

| Malaysia | 1,554 | 1,554 | |||

| Philippines | 5,167 | 3,811 | 5,652 | 14,630 | |

| Sarawak | 1,381 | 1,381 | |||

| Thailand | 1,674 | 1,674 | |||

| Vietnam | 5,986 | 39,292 | 20,207 | 65,485 | |

| Grand Total | 128,574 | 98,942 | 45,916 | 60,621 | 334,053 |

Year to July for sea freight comparison across Asian markets from DAFF figures.

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | Grand Total | |

| Brunei Darussalam | 2,489 | 4,040 | 4,519 | 11,838 | 5,416 | 2,834 | 31,136 |

| China | 58,156 | 76,718 | 71,586 | 58,348 | 79,131 | 45,319 | 389,258 |

| Indonesia | 293,222 | 376,516 | 298,024 | 263,771 | 186,076 | 201,176 | 1,618,785 |

| Malaysia | 14,173 | 13,944 | 13,985 | 13,679 | 2,180 | 1,554 | 59,515 |

| Philippines | 7,430 | 11,470 | 9,324 | 13,231 | 0 | 14,630 | 56,085 |

| Sarawak | 1,110 | 2,227 | 1,000 | 1,700 | 748 | 1,381 | 8,166 |

| Thailand | 800 | 0 | 1,736 | 0 | 1,772 | 1,674 | 5,982 |

| Vietnam | 114,420 | 143,027 | 184,611 | 124,847 | 34,004 | 65,485 | 666,394 |

| Grand Total | 491,800 | 627,942 | 584,785 | 487,414 | 309,327 | 334,053 |