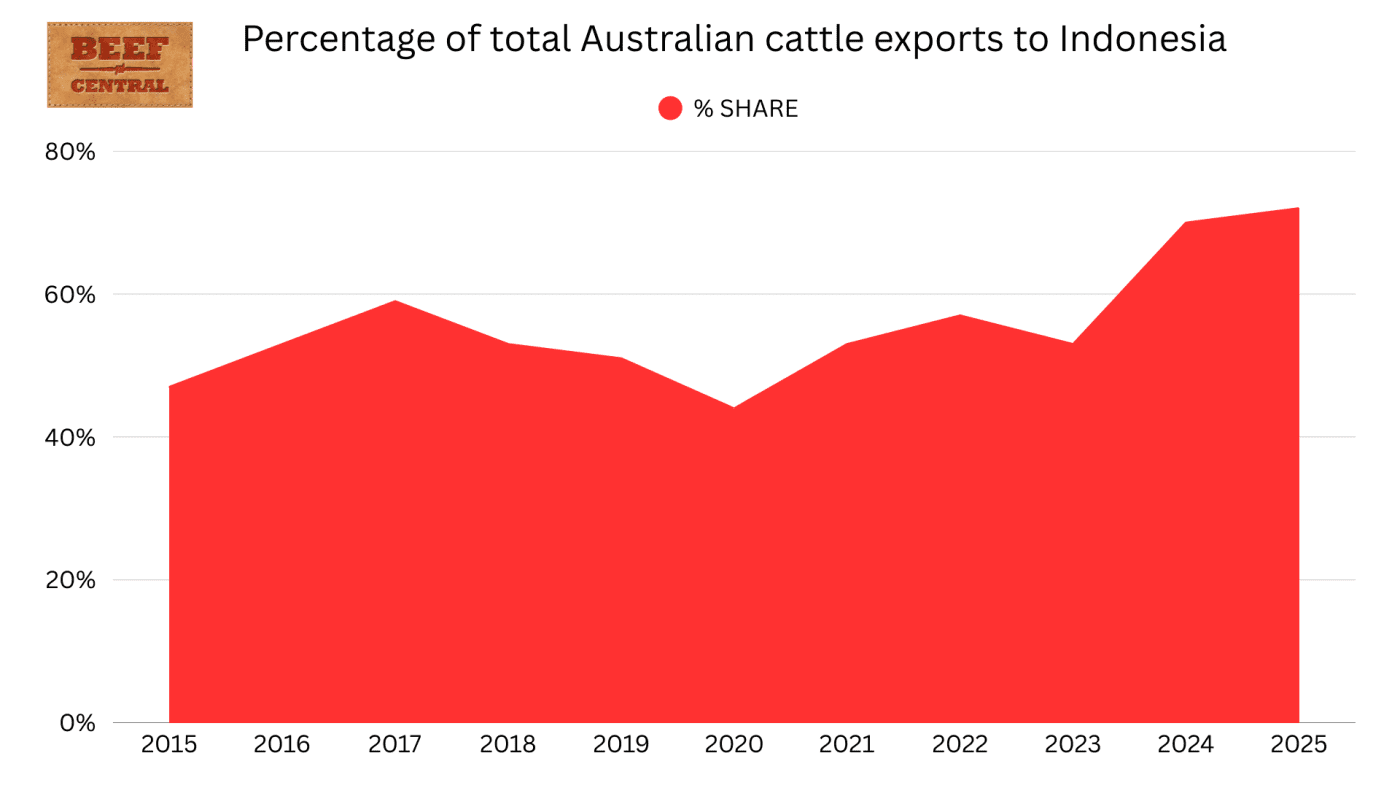

INDONESIA’S status as a powerhouse market for Australian export cattle has risen to even greater heights in 2025, taking almost three quarters of shipped stock this calendar year.

From January to November cattle exports to Indonesia totalled 510,565 head, according to latest DAFF data, accounting for 72 percent of the year-to-date total of 706,128 cattle shipped from Australia.

Shipping activity has stepped up in November and December as Indonesian importers move to fill feedlots in preparation for the main Ramadan/Lebaran beef consumption period in March/April 2026.

From a monthly average of 45,000 head through January to October, export volumes to Indonesia surged to 65,163 head in November.

An estimated 30,000 cattle may have already left so far this month and a final flurry of shipments through until December 31 under 2025 permits could see final numbers to Indo for the calendar year rise above 580,000 – a volume not reached since the high turnoff drought year of 2019.

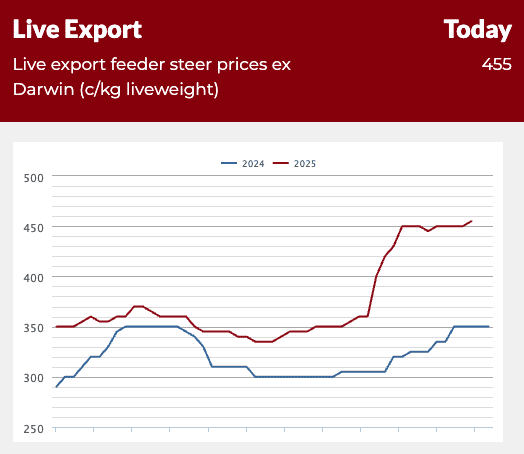

Prices have also responded to the jump in trade activity.

At the start of the year, export feeder steers stepping onto boats in Darwin were priced at $3.55/kg liveweight. That eased to 335c/kg as supply began to flow with the delayed start to annual mustering rounds in May, about a month late than usual due to a prolonged end to the wet season.

But as orders began to flow for the end of year shipments prices jumped by almost 100c from mid-September to mid-October, with current pricing at $4.55, and reports of some orders stretching out to $4.70 for top-up consignments.

Even with the higher prices, exporters have reported that there has been strong underlying demand from Indonesia, reflecting a resilient economic conditions, the Prabowo Government’s commitment to improving beef supply including through cattle imports, and the reductions that have occurred in Indonesia’s own cattle herd driven by the ongoing FMD and LSD outbreaks and culling programs.

In contrast to Indonesia, other key markets have continued to fall away in 2025.

Vietnam has been largely sidelined this year due to price sensitivity. Strong buying competition from southern processors and Queensland processors sourcing cattle in northern regions has pushed prices beyond Vietnam’s buying range.

Shipments to Vietnam have totalled 81,625 head so far this year, furthering a rate of annual decline from an upper level of almost 300,000 in 2020.

China has also retreated sharply as a destination for Australian cattle.

Unlike South East Asian markets which primarily buy feeder and ready-to-process cattle from northern regions, China primarily imports dairy heifers from southern Australia.

Shipments to China have dropped to 28,943 head in 2025, down from consistent annual volumes of well over 100,000 head prior to 2022. The decline has been attributed to weaker economic conditions and falling milk consumption in China.

In response to the downturn in China, Australian exporters have been actively working to find alternative markets for dairy heifers.

That has seen about 20,000 head across five shipments exported to Mexico since February, the first Australian cattle to that country since 2016.

A further 5000 head were exported to Turkey in 2025, marking Australia’s first shipment to that market since 2018.

Among the smaller markets, the Philippines has continued to re-emerge as a reliable customer, lifting its intake to almost 30,000 head in 2025.

While quite low volume, the Philippines market has grown year-on-year and has a preference for Bos Indicus cross composite-bred cattle, which are not in strong demand in Indonesia, providing a market outlet for northern cattle of that category. One reason given for this preference is that importers in the Philippines import and slaughter cattle in their own abattoirs and sell processed carcases, as opposed to fed cattle, which in turn leads to an increased focus on yield and carcase traits.

Keep an eye out in January for Beef Central’s 2026 Australian cattle export outlook.