THE seedstock industry has performed better than expected in the drought-plagued 2019 bull sales year, underpinned by resilient buyer confidence fuelled by continued high slaughter and live export cattle prices.

While there have certainly been individual bull sales within most breeds this year that have recorded below average to disastrous results, on average the outcomes have exceeded expectations, given the vast areas of eastern Australia that are experiencing sustained, crippling drought.

That’s an encouraging sign for those providing the genetic material on which commercial beef producers will rebuild their future after the current phase of herd reduction is completed.

Most, but not all breeds saw substantial reductions in the numbers of bulls offered and sold this year, as stud-masters reduced their offerings, in line with current demand expectations.

In sheer female statistical terms, bull requirements are considerably less now than what they were two years ago, with early industry projections estimates suggesting the national beef herd in 2020 will dip as low as 24.9 million head.

Beef Central’s genetics editor Al Rayner said this inevitably had a beneficial impact on the quality of remaining bulls sold this year, with the ‘tail’ of the calf drop removed well before auction day.

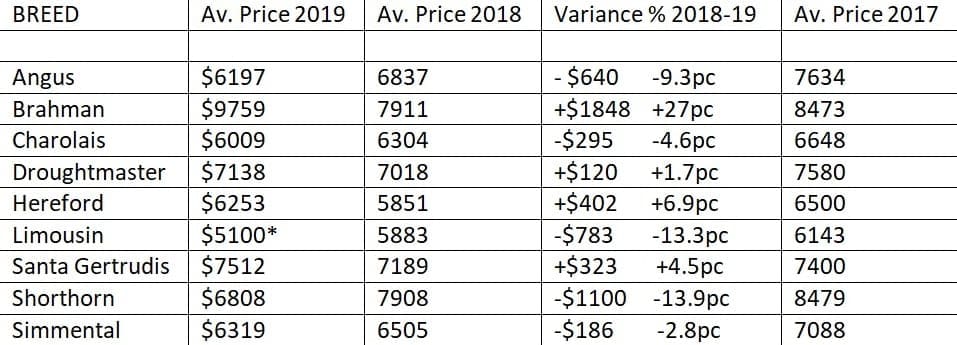

AVERAGE PRICE – auction sales 2019:

Background

Beef Central has conducted an annual analysis of auction bull sale results across Australia for larger breeds each year since 2011, based on average prices achieved for each breed, numbers of bulls sold, and where available, clearance rates.

Nine years’ worth of data clearly shows that two key attributes drive breed-scale bull sale performance: seasonal conditions and commercial cattle prices. In years when both are in favour, like 2016-17, prices hit historically high levels, underpinned by buyer confidence. When either is lacking, results are impacted, to varying degrees.

For example there is a clear correlation between the start of Australia’s current cattle price boom cycle in mid-2015, carrying through to today, with better average bull prices. It appears that seasons, on the other hand, tend to have a greater bearing on the number of bulls sold, and clearance rates achieved.

The statistics presented in this article on average prices for each breed, and a second article published today on numbers of bulls sold in 2019, show that this year’s drought has had a measurable impact on both price and clearance rates on some breeds, but certainly not all.

However the impact this year is somewhat masked by the fact that drought was already affecting large parts of the country last year, pushing some 2018 bull sale results lower. That, in turn, has tended to dilute the drought impact seen on prices and sale volume in 2019.

For that reason, the statistical tables included in today’s articles include a column for 2017 bull sale average prices and numbers sold, providing a truer impression of trends before the drought set in.

Firstly, a caveat on the statistics provided in today’s reports. Several breeds have reported that a number of studs were unwilling to share their results for 2019 sales – presumably because their outcomes were disappointing, due to drought.

That will inevitably skew results a little for those breeds, in two ways. It will artificially inflate average price, and potentially under-report the number of bulls sold. We’re confident that the statistical impact is only minor, however, given the modest numbers of ‘unreported’ bulls involved.

Broad spread in average price trends

There was a wide spectrum of results in average price trends between 2018 and 2019 for beef bulls sold this year.

As this table shows, five of the nine breeds listed saw declines in price, but most surprisingly, four showed increases in value.

In what was an extraordinary achievement in a desperately dry year, Brahman bull breeders notched up an incredible 27pc increase in value on 1893 bulls sold at auction in 2019. The average price figure of $9759 is easily the highest ever recorded for any breed in the nine years that this data has been recorded.

And unlike most other breeds, the Brahman result included about 10pc of the offering that were unregistered herd bulls. If the 179 herd bulls sold for an average price of $5785 a head are removed from this year’s Brahman auction statistics, the remaining registered Brahman bulls achieved an unbelievable average price of $10,174.

The previous high point for Brahmans, or for any breed for that matter, was the 2016 year when the breed averaged $8688 for a total of 2321 bulls sold – considerably more bulls than this year.

Australian Brahman Breeders Association manager Anastasia Fanning said continued strength in cattle prices, both for meatworks cattle and live export, had helped underpin confidence this year among buyers, despite the desperately dry conditions across Queensland, the Northern Territory and northern parts of WA.

No breed is as heavily exposed to the live export industry as Brahmans, and continued strong demand out of Indonesia for lighter cattle, and Vietnam for heavier cattle, has underpinned trade, with Indonesia steers currently worth 320c/kg liveweight ex Darwin. And with vessels now routinely loading from ports as far south as Port Alma, near Rockhampton, a greater proportion of Brahman-influenced cattle are exposed to live export competition.

Psychology of buying bulls

As this report has discussed in past years, there’s also a theory that bull buyers in the northern half of the continent tend to think defensively in their bull purchase decisions during dry times, opting for breeds offering environmental adaptation over meat quality or fertility. Conversely, in above average years, the appetite is more likely to grow for British or Euro options. The counter-argument to that, of course, is that it’s going to be 12 months before calves from bulls bought today hit the ground, and two years or more before many are sold, by which time today’s seasonal conditions are likely to be long gone.

Other breeds showing sold gains in average value this year over 2018 were Hereford (+$402 or 6.9pc), Santa Gertrudis (+$323 or 4.5pc) and Droughtmaster (+$120 or 1.7pc). Some of these results may have been coming off a low base, however, as all four breeds already showed declines in average price last year, for drought reasons.

Among other breeds, Angus recorded a $640/head decline in average value of bulls sold this year, a decline of 9.3pc, while Shorthorns suffered the biggest reduction of all breeds of $1100/head, or almost 14pc.

Peter Parnell

Angus Australia chief executive Dr Peter Parnell said despite the unprecedented adverse climatic conditions experienced by many Angus Australia members, 2019 had been a remarkably strong year for the breed.

“While the general trend for bulls sold at auction, and the average sale prices received for Angus bulls was lower than the past couple of years, this was not always the case,” he said.

“A number of Angus bull breeders had outstanding results either on par or beyond the results received in recent years. There was still strong demand for structurally sound Angus bulls with good phenotype and balanced performance figures, particularly from bull breeding herds that have strong marketing programs beyond their immediate local area,” Dr Parnell said.

“Overall, Angus breeders remain very positive about the future of the industry and the breed. Once we get relief in seasonal conditions there will be strong demand for Angus females, with many breeders wishing to re-build their depleted cow herds,” he said.

In the event of no rain relief, the industry would remain in a holding pattern with further reduction in the female herd having a negative impact on the bull market in 2020.

“All indicators are strong for Angus for the foreseeable future, once we get over the current major disruption in production caused by the devastating extreme drought. Angus brands are still very strong, with keen interest in the supply chain to expand existing brands and introduce new high quality Angus brands to both the local and export markets,” Dr Parnell said.

He said there was an observable trend that spring Angus sales in the northern areas of NSW and QLD were tougher than many of the earlier autumn sales.

“The reported sales in Queensland and northern NSW were the most affected in terms of numbers of bulls offered/sold, and average sale prices received. However, clearance sales were generally still very good,” he said.

“There were a couple of outstanding sales reported in NSW that defied the odds with record sale averages and this had a positive impact on the overall figures for NSW. Having said that, the numbers of reported bulls sold and bull sale averages in Victoria and South Australia were also lower than 2018 due to relatively tough season leading up to and during the autumn sales – even though these areas subsequently fared much better than the north as the year progressed.”

- Click this link to access today’s second statistical report on the number of of bulls sold at auction during 2019.

2020 autumn bull sales marketing

Stud managers wishing to promote their Autumn 2020 bull sales via ads on Beef Central’s genetics pages, daily email alert or home page should contact business development manager Rod Hibberd (pictured) at rod@beefcentral.com or phone on 0437 870 127. Ad spaces are limited, so make contact early to avoid disappointment.

Stud managers wishing to promote their Autumn 2020 bull sales via ads on Beef Central’s genetics pages, daily email alert or home page should contact business development manager Rod Hibberd (pictured) at rod@beefcentral.com or phone on 0437 870 127. Ad spaces are limited, so make contact early to avoid disappointment.

Leading up to Christmas, work will also start on compiling the full list of 2020 Upcoming Bull Sales, appearing as a tabulated list in Beef Central’s genetics section. We remind studmasters to submit their 2020 sale dates (via this form), if they are not already provided by respective breed societies.