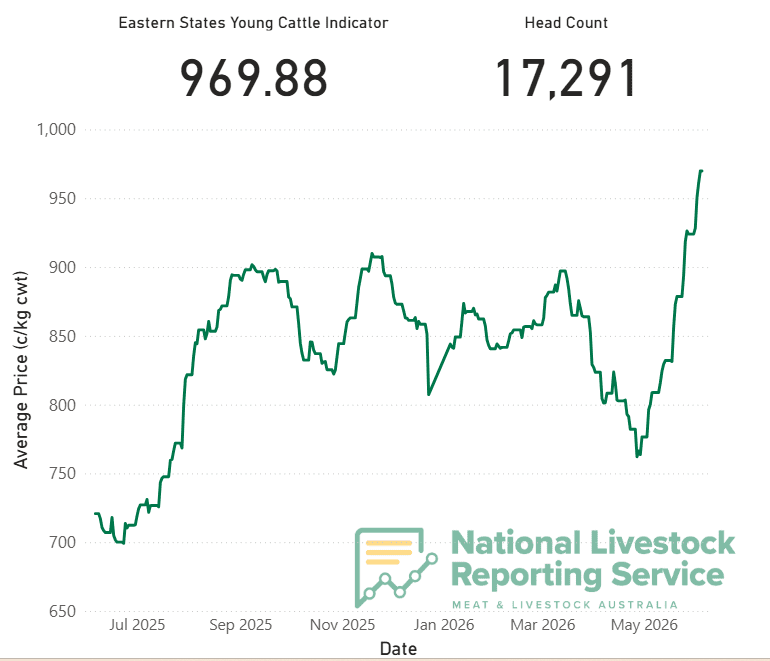

Australian cattle prices rebounded sharply in May after trending lower since mid-March. The shift reflects a classic supply-and-demand pivot: rain improved producer sentiment, cattle yardings tightened, and buyers for restocking, feeding and processing all came back into the market at the same time.

The most striking feature of the move is that it hasn’t been driven by one segment alone. Indicators across young cattle, feeder cattle and cows have all strengthened, and the National Young Cattle Indicator has reached $508.9c/kg liveweight (lwt), the highest level since 2022. That broad-based lift suggests the market is not simply reacting to one-off buying interest, but to a genuine shift in fundamentals.

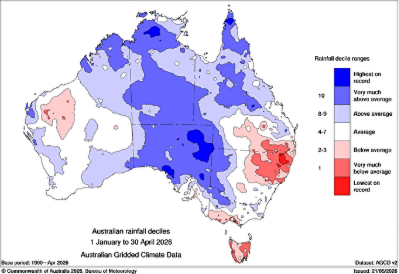

Figure 1: Rain decile from January to April 2026 and the monthly rain in May

Source: BOM

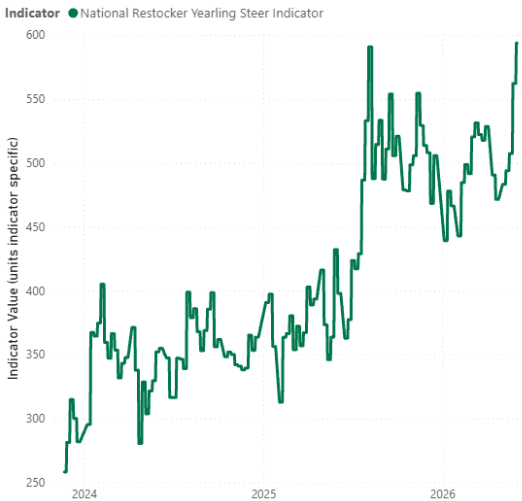

Rain was the immediate catalyst. In late May, widespread falls were recorded across the country, particularly in north NSW and southern Queensland, where they were most needed. This boosted restocker activity and reduced the number of cattle being offered. Market reports claim stronger competition almost everywhere, with some saleyards recording very large one-day jumps in young cattle prices as buyers chased lighter lines before paddock feed and confidence tightened further. For instance, the Restocker Yearling Steer Indicator jumped from 40¢ at Wagga week–on–week and 122¢ since the beginning of May, reaching a premium price to 594¢/kg lwt.

Figure 2: Restocker Yearling Steer Indicator – Wagga Wagga saleyard

Source: NLRS

Regional spreads have also widened. NSW has recorded some of the sharpest gains, especially in yards such as Wagga, Singleton, Tamworth and Forbes, where rain and lower numbers triggered aggressive restocker competition. Queensland has been firm too, with strong cattle prices in southern and central areas reflecting both local restocking interest and processor demand.

Supply has also been doing a lot of the work. After a heavy run of cattle earlier in the year, numbers available for sale eased as producers responded to seasonal uncertainty and stronger local demand. Lower yardings matter because the market has been running into winter with active feedlot and restocker demand still intact, which means fewer cattle available can quickly translate into much stronger prices.

That combination is important: high slaughter does not automatically mean weaker prices. In this case, strong processing throughput is being absorbed by export demand, which has allowed prices to rise even while kill numbers remain solid. In other words, the market has moved from being supply-led in April to demand-supported in May.

HAVE YOUR SAY