147th Edition: May 2026

Key Points:

- Vietnam seeks emergency approval to import SAT-1 FMD vaccines as cross-border disease risk rises.

- Indonesian meat processors continue to lobby for their 2026 private beef quota to be restored from 30,000 to 180,000 tonnes.

- Sea freight stays under pressure, with Singapore bunker fuel at USD 850/mt still nearly double January’s USD 480/mt.

Regional Trends and Overview

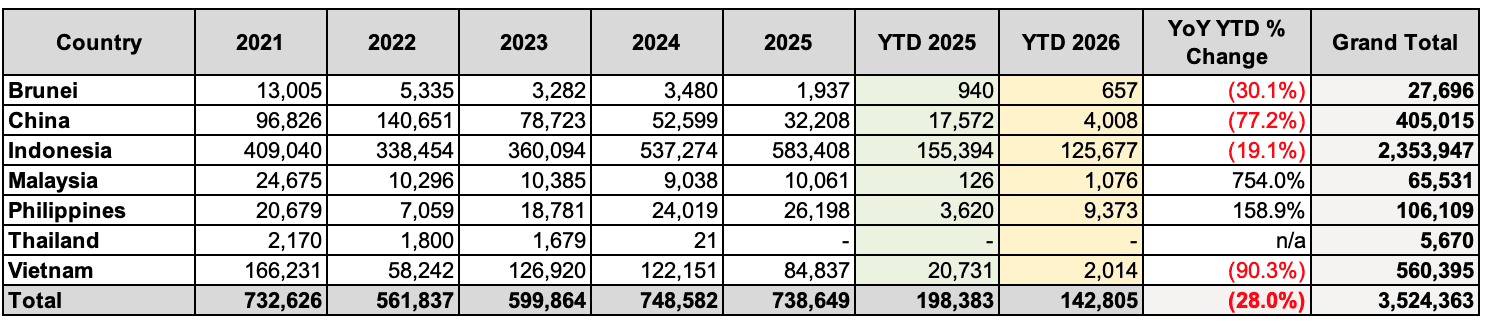

Australian cattle exports to Southeast Asia and China have totalled 142,805 head through the first four months of 2026, down 28 percent on the same period last year. The slow start reflects the extended northern wet season, the earlier 2026 Ramadan that pulled festival cattle into late 2025, and the Indonesian feedlot squeeze that took some heat out of the trade.

Dr Michael Patching

Where the volume sits across markets is more interesting. Indonesia accounted for 125,677 head, or 88 per cent of total YTD volume, down 19 per cent on the same period last year but still doing the bulk of the work. Vietnam has essentially stopped, with just 2,014 head for the year to date against 20,731 a year earlier. That is a 90 per cent fall and confirms what I have been writing about ESCAS abattoir capacity contracting and uncompetitive cattle pricing in that market. The Philippines is the standout in the other direction, lifting from 3,620 to 9,373 head, up around 160 per cent and already tracking at around 36 per cent of full 2025 volume in only four months. To me it still looks like the Southeast Asian destination with the most genuine upside.

Year 2026 cattle exports – comparison across SE Asean markets

Source: DAFF website

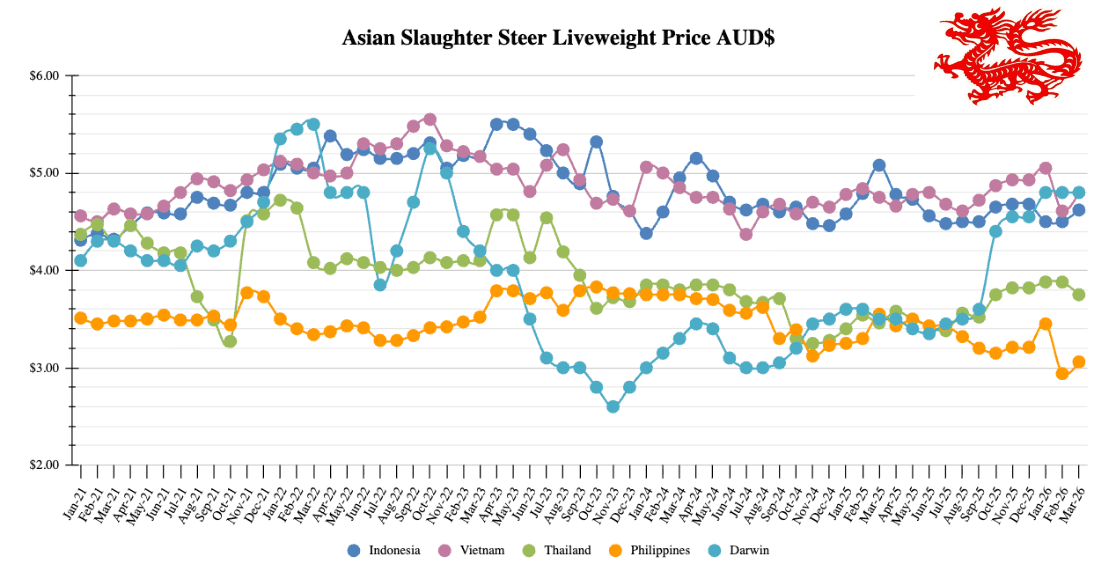

Regional Price Graph

Indonesia: Slaughter Steers $4.94 AUD per kg live weight (IDR 12,600 = $1 AUD)

Prices

Indonesian cattle prices continue to firm despite the easing in Darwin. Lampung slaughter steers are now around IDR 62,000 per kg (AUD 4.94), with Java steers a touch higher around IDR 64,500 (AUD 5.12). The retail picture has not improved either. Wet market beef knuckle is still running at around IDR 145,000 per kg (AUD 11.51), with supermarket knuckle near IDR 160,000 (AUD 12.70). Chicken sits around IDR 38,000 per kg (AUD 3.02), and the gap against beef just keeps widening. The chicken price holds because Indonesia’s poultry industry has structural advantages beef cannot match. Production is largely domestic, cycle times are measured in weeks rather than months, and feed conversion is roughly four times more efficient than for cattle. Beef is tied to imported Australian cattle, a rupiah-denominated price ceiling, and a long, capital-intensive supply chain.

Photos: Cassava harvesting (left), drying process (right)

Why cassava still sits at the centre of the feedlot ration

It is worth a step back this month to talk about something structural in the Indonesian system. Cassava is a common major input in Indonesian feedlot rations, in two forms. Gaplek is peeled and sun-dried cassava root sliced into chips. Onggok is the fibrous pulp left behind once tapioca starch has been extracted at processing factories. It plays a similar role to corn in American feedyards. Fresh cassava is highly perishable and carries naturally occurring cyanide, so roots are dug, peeled, sliced and dried on concrete pads or compacted soil, with the drying step also breaking the cyanide down. At around 85 per cent starch and energy-dense, gaplek typically sits at 20 to 40 per cent of feedlot concentrate rations, balanced against palm kernel meal, copra and soybean meal for protein and rice straw or king grass for fibre.

It is worth a step back this month to talk about something structural in the Indonesian system. Cassava is a common major input in Indonesian feedlot rations, in two forms. Gaplek is peeled and sun-dried cassava root sliced into chips. Onggok is the fibrous pulp left behind once tapioca starch has been extracted at processing factories. It plays a similar role to corn in American feedyards. Fresh cassava is highly perishable and carries naturally occurring cyanide, so roots are dug, peeled, sliced and dried on concrete pads or compacted soil, with the drying step also breaking the cyanide down. At around 85 per cent starch and energy-dense, gaplek typically sits at 20 to 40 per cent of feedlot concentrate rations, balanced against palm kernel meal, copra and soybean meal for protein and rice straw or king grass for fibre.

Indonesia is the world’s third largest cassava producer, with around one million hectares of it, mostly in Lampung in south Sumatra and across central Java where the biggest feedlots also happen to sit. The reason it is worth talking about now is that feed input costs have been creeping higher for the past 18 months. Cassava prices have risen as plantings shift to higher-value crops, and feedlotters now have to plan months ahead, buying in volume when seasonal supply is up and storing it through the lean part of the year.

APPDI presses for private quota to return to 180,000 tonnes

The political fight over the 2026 beef import quotas has come back into the open. Teguh Boediyana, executive director of the Indonesian Meat Producers and Processors Association (APPDI), is publicly pushing for the private quota to be restored from 30,000 tonnes to around 180,000 tonnes, the level allocated in 2025, arguing the current settings are slowing business expansion and putting jobs at risk. Whether anything shifts is another matter. The 2026 structure was signed off with political backing from the top, including the Brazilian quota that followed President Lula’s Jakarta visit last year, and Jakarta has little appetite for reversing it. For Australian exporters this is a boxed beef issue rather than a live cattle one, but restoration of private quota space is the only realistic way for our chilled product to compete in modern retail and food service.

Vietnam: Slaughter Steers $4.86 AUD per kg live weight (VND 19,100 = $1 AUD)

Vietnam moves on emergency SAT-1 vaccine imports

Vietnam’s Ministry of Agriculture and Environment has formally proposed to the Prime Minister, in a report dated 6 May, that emergency approval be granted for the import of SAT-1 foot-and-mouth disease vaccines. Currently licensed FMD vaccines in Vietnam cover only serotypes O, A and Asia1, leaving the herd unprotected against SAT-1, which the Ministry says is spreading geographically through cross-border livestock movements. The move is a step up from April’s focus on diagnostic kits at the border, and signals Hanoi is willing to spend on prevention rather than just surveillance. The same risk runs further south to Indonesia, where the herd is still rebuilding from earlier FMD outbreaks and another disease event would land hard on already thin local supply. Anything that tightens biosecurity at the Cambodia and Laos crossings makes the unofficial Thai cattle flows into Vietnam more difficult, slower and more expensive, and that is precisely the segment that has been competing with disease-free Australian cattle on price for a long time.

Philippines: Slaughter Steers $3.80 AUD per kg Live weight (₱44 = $1 AUD)

Prices

Philippine livestock prices have continued to drift in a familiar direction. Wet market beef knuckle is around ₱365 per kg (AUD 8.30), supermarket knuckle near ₱420 (AUD 9.55), with slaughter steers around ₱135 (AUD 3.08). Pork carcass is steady around ₱245 (AUD 5.57), and broilers sit near ₱170 (AUD 3.86), with branded chicken such as Magnolia trading closer to ₱247 (AUD 5.61). The slightly weaker peso this month is doing some of the work in the AUD conversions, but the local-currency picture has been very flat. With no major policy change in the past month, the Philippines section is genuinely quiet. The zero-tariff debate I covered in April is still ticking along in the background but has not moved decisively in either direction.

Australia: Feeder Steers Darwin $4.10

The headline number this month is the Darwin feeder price, which has come off the $4.50 highs of February and March to sit closer to $4.10 per kg liveweight. That is around a 9 per cent fall in roughly four weeks. Fairly typical for this time of year as supplies come on but still a welcome relief to our trading partners.

The dry season has set in across the Top End, mustering is in full swing, and the trade is busy. Several vessels have loaded out of Broome over the past month through the Kimberley Marine Support Base floating wharf, which opened last October and is now becoming part of the regular dispatch picture. The Broome route saves close to two days of sailing time on the Indonesia run compared with Darwin, and the 24/7 tide-independent loading is doing what was advertised.

The other piece in the freight picture is bunker fuel, where the volatility this year has been more notable than the level. Singapore bunker pricing peaked at around USD 1,100/mt in early March on the Iran conflict spike, fell back to USD 690/mt by mid-April, and has since rebounded to around USD 850/mt. That compares with about USD 480 at the start of the year, so even after the partial unwind the net effect is still a meaningful cost increase that flows through to CIF prices as charters roll over. On the short Darwin to Indonesia leg the USD exposure is less than longer voyages to say, Vietnam, but it is one more pressure point sitting on top of feedlot margins that were already paper-thin.

HAVE YOUR SAY