Richard Koch, Elders

Author Richard Koch is chief analyst with Elders. His regional roundup is based on dialogue with Elders regional livestock managers held each week.

FORMER chairman of the US Federal Reserve in the 1990s, Alan Greenspan, famously used the term “irrational exuberance” to suggest that the stock market might be overvalued.

While I’m not suggesting that cattle markets are widely overvalued, I think some of the sentiment that there is only blue sky ahead (based largely on falling US production) ignores some of the risks posed by looming market access issues and rising competition from South American beef. Beef Central touched on this topic briefly in Tuesday’s Weekly Kill report.

Cattle markets improved across Australia this week by 20-30c/kg with cows and heifers leading the charge as:

- turnoff out of nth NSW slowed,

- a widespread rainfall system brought rain to dry areas of the east coast with more in the forecast,

- temperatures remained mild leading to good pasture and fodder crop growth and,

- some QLD producers took stock and slowed sales having sold enough cattle to meet immediate cash flow requirements.

In my weekly hookups with Elders agents across Australia, the mood tends to swing based on what the market did last week, the prevailing seasonal conditions, the rainfall forecast and the local supply outlook.

So there was quite a bit of optimism this week “things are travelling along well” was the key sentiment. No doubt the factors above have an important and sometimes overwhelming influence on market sentiment, but sentiment based on these tends to be fickle and short-term in nature. The larger and sustained long-term trends are driven by global demand for Australian beef.

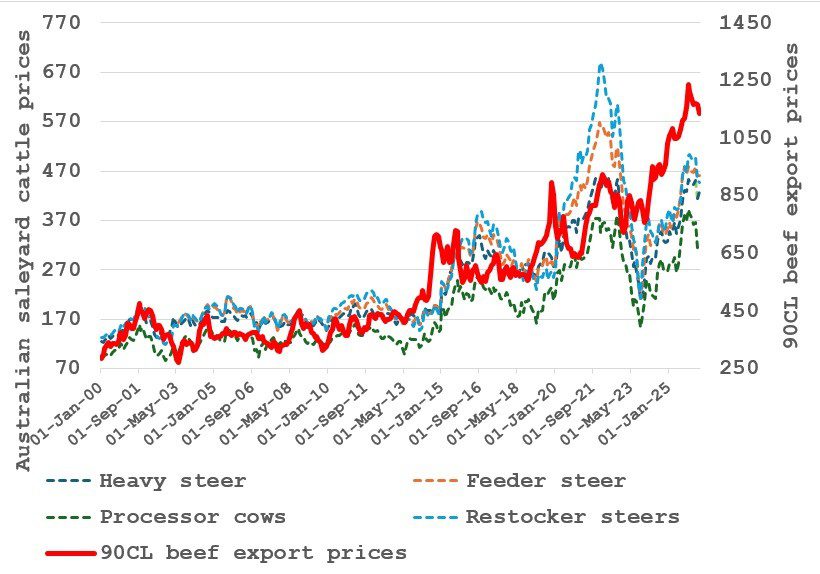

Sources: MLA, USDA. Click on graphs for a larger view.

This chart above shows the strong correlation between the export price of 90CL beef vs saleyard prices of major Australian cattle categories.

The other issue that tends to dominate thinking is that what happens in overseas markets is less important than what comes out of the sky in Australia. While this may have been true in yester years, as our feedlot and pasture management systems have evolved, we are less prone to violent fluctuations in supply and prices.

A case in point is that our markets held up relatively well despite a generational turnoff in cattle out of the New England. The worst recent example of where our markets disengaged from the global market was in 2023 where our processing sector was overwhelmed by supply due to some reckless long-term weather forecasting and processing capacity constraints.

A case in point is that our markets held up relatively well despite a generational turnoff in cattle out of the New England. The worst recent example of where our markets disengaged from the global market was in 2023 where our processing sector was overwhelmed by supply due to some reckless long-term weather forecasting and processing capacity constraints.

So, while it is important to understand local supply and demand dynamics and keep an eye on the sky, part of my job is looking ahead and assessing factor that could impact future demand for Australian beef.

While not wanting to be the bearer of bad news, as an economist rather than a stock agent it would be remiss of me to not inform Beef Central readers of several looming market access developments that could negatively affect the bright demand outlook for Australian beef in H2 2026 as espoused by our regional agents further below:

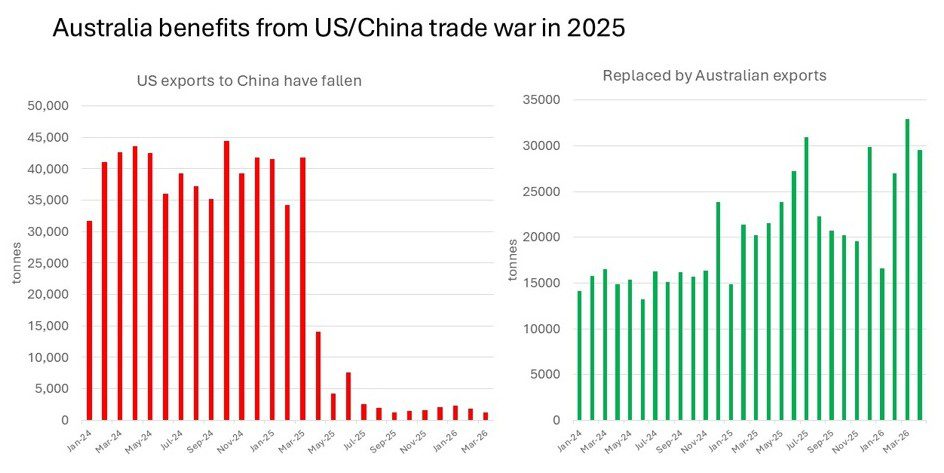

China has renewed the export licenses of 425 US beef plants which it let lapse in March 2025. Australian exporters have virtually replaced US beef in China which has been a key driver ion the strength of our local prices in 20025 and so far in 2026. Australian exporters will be directly affected by China giving access to US beef exporters with increase in competition for grain finished product. In the near term, however, the biggest concern for Australian exporters is lack of quota in China (see below)

China’s Ministry of Commerce (MOFCOM) has announced Australian beef imports have reached 80% of China’s 2026 safeguard quota as of Saturday, May 14. Up to 30,000 tonnes per month (21% of all exports) of Australian beef previously destined for China will need to be diverted to other markets (presumably at lower values) in H2 2026.

Trump is considering suspending the TRQ (Tariff Rate Quota) on imported beef into the US which would allow Brazilian beef tariff free access to the US market (currently the Brazilian out of quota tariff is 26.4%). The betting is that trump will do something and impose a temporary additional tariff free quota, like what he has done with Argentina with a bunch of trade off trade-offs to the domestic cattle industry. Brazil has been lobbying hard and the fact that US access to China has been restored has increased the chances of this happening with Trump needing a win on cost-of-living pressure before the November mid-terms. Given tight supplies of lean beef in the US, prices should be hold relatively firm, however the reduction in the tariff on Brazilian beef will affect Australia’s competitive positioning in the US vs Brazilian product.

Australia will likely trigger its Korean safeguard in late July, well ahead of the September 12 date of 2025 (our above quota tariff jumps to 24pc). Previously this has been managed by placing product in bond to be used against the following year’s quota. It is uncertain if Korean importers will be willing to carry bonded product for up to 5 months. Last month we exported 21,000 tonnes to Korea (16pc of all exports).

Brazil has already filled half its annual 1.1 million-tonne tariff-protected beef quota to China and is on pace to exhaust the limit before mid-2026, after which any additional shipment will face a 55% surcharge that effectively shuts down the trade with its largest customer. Industry estimates put 400,000 to 600,000 tonnes of Brazilian beef that needs to be redirected from China to other destinations in the second half of 2026. Live-cattle futures in São Paulo have already begun to ease as ranchers price in the coming domestic-market overhang. There is the strong likelihood that this product will find its way to the US again intensifying competition vs Australian product.

Kimberley stations keen to offload cattle

Turning back to regional livestock market influences this week, there is a flush of cattle being offered out of the Kimberley with offers at $3.60/kg for a Brahman feeder steer ex-Broome vs Darwin at $4/kg. The market is holding but the push by Kimberley operations to get cattle on boats before Darwin ramps up has them accepting lower rates.

There are no boats planned for Townsville over the next month with local feedlot and restockers holding sway over the live export operators with Townsville needing to be 35 cents cheaper than Darwin to work. The bullock market in Charters Towers has been hard to quote with few decent lines available but a good run of bullocks this week tested the market and were knocked down at $3.70/kg. Local works are interested in bullocks from 380kgs (preferably +400kgs) at $3.70/kg which is putting them out of reach for live exporters.

There is local restocking demand for heifers with any with weight selling well and even lighter store types, if they’re good quality, attracting interest. But secondary quality cattle are getting dealt with rather harshly.

The big news for the week for the northern Australian cattle industry is that Australian company Heytesbury – a large player in the northern live export industry – has bought 11 cattle ships (out of the 20 licensed carriers operating out of Australia). This is a huge vote of confidence for the longevity of the industry that should ensure it is well service with shipping capacity into the future.

Sth Qld markets lifts as northern NSW supplies taper

The Downs feeder market recovered 10-15c/kg to $4.70-4.80/kg as sth QLD graziers with one eye on the forecast and not liking the recent fall in prices ease down on selling. Some QLD operations have probably sold enough to generate enough cash flow for their immediate needs and with plenty of feed available are in no rush to chase the market.

With this slowdown, gaps are starting to open in kill schedules as southern operators become more active in northern markets and take some supply away from QLD processors.

QLD selling activity may change as the weather starts to get cold and the first frosts hit or the when the new financial year ticks over.

There is some supply starting to move out of the north-west now it has dried out, and access has improved with reports of a deal of 40 decks of cattle from an individual vendor to a Downs feedlot this week.

Some southern feedlots are in northern markets with a bid for flatbacks at $4.65/kg delivered Blackall for trucking south. The ever widening spread to southern Angus feeders making this trade possible

CQ market has rebounded after a tougher fortnight

Weather across CQ has been magnificent with a month of clear days without any rain which is seeing cattle moving. As the numbers started to flow a fortnight ago everything got a little bit tough, probably as supplies were running into the backend of the heavy turnoff out of northern NSW.

But the market has rebounded nicely. The lead run of good CQ weaner steers got back out to $5.40 to $5.50/kg in the yards when they were struggling to make $5/kg a week ago.

There is still plenty of opportunity on your light heifers, with gap too large to the equivalent steers in weaner markets.

It’s the same story on trade feeders – they were hard to sell a couple of weeks ago, but they’re back buying 320-380kg heifers at $3.75/kg with this market strengthening.

On slaughter cattle, heavy slaughter steers in CQ are back up to the mid-$4’s/kg from $4.20/kg a few weeks ago. Same with the cows which were 20 to 30c/kg better than last week, so everything’s positive and the numbers are flowing.

Anyone in the south or west looking for a better type flatback heifer there’s still plenty of good buying opportunities in CQ.

Northern NSW well and truly over the hump in numbers

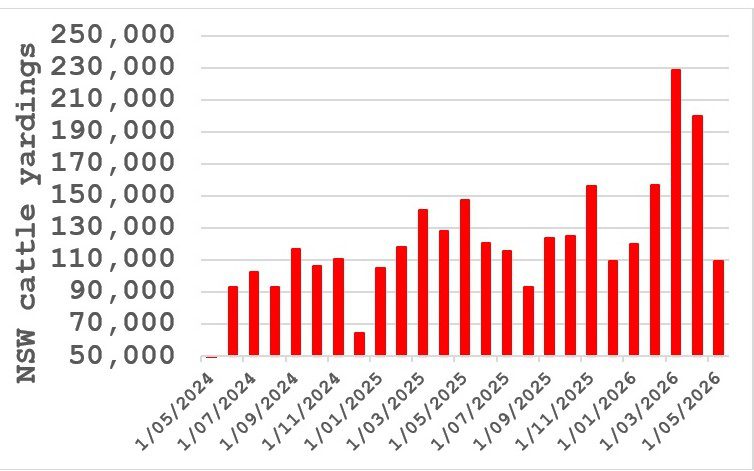

Gunnedah yardings were back to 2,500 about one third of what they were at the peak in the few months – this is being replicated all through northern NSW. Mexican buyers are all heading further north chasing supply as there is not a lot of stock left in any great numbers through nth NSW.

NSW monthly cattle yardings. Source: MLA

Markets have held up well considering. Cows are $7.80 on grids in the south, domestic retailers are in the high $8’s/kg and program grassfed cattle are still making $9/kg plus, so that’s all ticking along well.

Black feeder steers generally $5.15 to $5.30/kg but there will be some supply pressure in June, July and into August, as there will be no significant feeder numbers coming out of northern NSW for the balance of this year. The best quote I heard was $5.45/t into Riverina feedlots.

One of the biggest movers we saw last week was on 400-500kg feeder heifers. They’ve lifted the best part of 50 to 80c/kg, topping at $4.94/kg at Dubbo last Thursday.

Direct to feedlot prices on coloured heifers $4.50 to $4.70/kg, but that is under review this week, which is an indication that they’re not getting enough heavy steers.

Groundwater remains key issue across Victoria

Victoria generally received 10-40mm across the state over the weekend – a bit patchy but it hit most cattle regions.

The biggest challenge remains groundwater. Although there is green grass in paddocks, there has been little runoff rain with graziers concerned about what they’re going to do for water from the western district right through to Ballarat and up to Avoca – so a good chunk of Victoria. That’s just keeping would be restockers on the defensive.

Victoria is running out of kill cattle numbers quickly with cows a little bit dearer last week. Markets are getting hard to quote due to the variation in quality and numbers from week to week.

The season has turned around in the Eastern Riverina and if we get some rain out of this next change it will probably be one of the better autumns, they have had in while, The good thing about the Riverina is the country is well watered. With most having access to bore water or river water.

Haven’t heard much about calving percentages with most around here are Spring calvers anyway, but going on the lambing percentages you would assume fertility rates should be pretty good.

Another damp weekend in South Australia

It was another damp weekend across South Australia, perfect for slow old footballers. There was a bit more rain along the coast and lower parts of the south-east, and very timely, nice rain through the Mallee.

Not a lot of change in the livestock markets. Good cows are now $4/kg and a bit, heavy steers $5/kg, heifers $4.60-4.80/kg on the exceptional lines and and feeder steers and $5.20-$5.30/kg for good blacks.

Like in Victoria, our numbers are winding back and not a lot of cattle left out in the paddocks. It’s going to be a long, slow winter. But on a positive note, the grass is still growing, and grain cockies are now going flat stick now they can get back on country that got a bit wet on the weekend.

WA dryer than you think

Although not big cattle areas, WA needs rain from the central wheatbelt through to the Geraldton zone in the north. A lot of the crops have come up and are just sitting there looking just okay. But another dry week or so and they will be struggling. The south-west, and south coast are good but parts of The Great Southern (mainly sheep areas) are tightening.

WA store cattle prices have firmed over the last couple of weeks with graziers down south having them to put on grass where the season is good.

Steers under 280 kilos are making $4.50 to $6.10/kg to average $5.66/kg, up 50c/kg. Steers 280 to 380kgs, $5.15-5.70/kg to average $5.40/kg and steers 400kgs plus $4.30 to $5.24/kg to average $4.90/kg.

Heifers were also up under 280kgs, $3.50 to $5.92/kg, the average $5.19/kg, so they’re up 50c/kg. 280 to 380kgs, $4.70-5.30/kg to average $4.95 and 400kgs plus $3.60 to $5.12 to average $4.85/kg.

Cows haven’t changed too much. They’re sitting on $3.40 to $3.70/kg in the sale yards, consistently.

This week there is a 1400 head store sale at Boyanup which should meet with strong demand. But from now through to Spring, the feedlot buying will start to wind down until September when southern turnoff starts to increase again and then they will start gearing up for the weaners sales in October/November.

More rain in the north but southern Tassie dire

Tassie had more rain go through over the weekend. Basically, the northwest through to the Highlands and into the Durant Valley 10-20mm, but most other parts of the state missed out.

Central north of Tassie and through the Midlands into the southeast, is still struggling badly, with lack of moisture. Groundwater seems to be the main issue, particularly on that east coast and Midlands now. But the rest of the state has had a good Autumn.

In cattle markets, program yearlings sitting on around 850-ish. Better cows $7/kg dw to the works and $3.40 to $3.60/kg in the yards

The store cattle market got a little bit subdued with the seasonal flush of cattle before winter and most graziers with feed seem to have enough numbers. Heavy type steers around 400kgs can be bought for $4.60 to $5/kg for anyone with excess feed. Medium weights 300-400kgs $4.80 to $5.30, and the lighter types, anywhere from $5-6/kg

On heifers you probably just throw a blanket over them at $3.80 to $4.40 for all weights and all grades.

It’s starting to get a little bit cooler here, but other than that, tracking along well in most parts of the state.

HAVE YOUR SAY