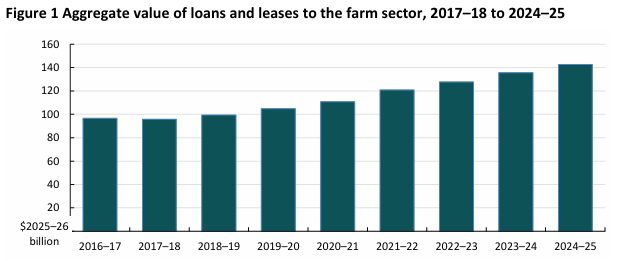

LENDING to the farm sector has increased by 5 percent in real terms, to $142.5 billion, according to the latest data.

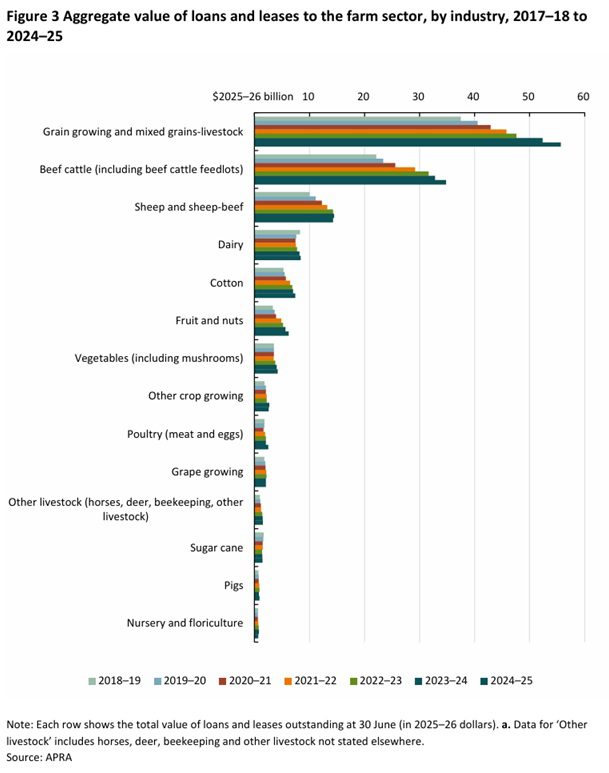

Lending rose across all states and territories, except the Northern Territory, with strongest growth in Western Australia (8.2pc) and South Australia (7.5pc), according to the 2023-24 Australian Prudential Regulation Authority (APRA) lending data.

Executive Director of ABARES Dr Jared Greenville said that the use of debt by farmers was an important part of farmers developing their business and for ensuring ongoing working capital.

“A lot of farmers are taking on debt so they can invest back into their businesses,” Dr Greenville said.

“Some of the increase was because farmers needed working capital or were unable to reduce debt.

“Overall, most debt is manageable with less than 0.1pc of the nearly 147,000 farms loans in operation loans subject to debt mediation and foreclosure.”

There was an increase in overdue payments, with loans and leases more than 90 days past due rising from $1.18 billion in 2023-24 to $2.1 billion in 2024-25.

There was an increase in overdue payments, with loans and leases more than 90 days past due rising from $1.18 billion in 2023-24 to $2.1 billion in 2024-25.

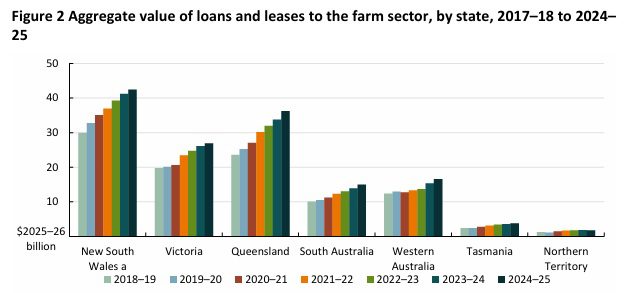

At an industry level, lending shares are broadly consistent with the size or output of each industry.

At an industry level, lending shares are broadly consistent with the size or output of each industry.

Meaning industries with larger land use and higher levels of production naturally account for a greater proportion of overall lending within the agricultural sector.

Lending to farms in the broadacre sector (beef cattle, grain growing and sheep and wool production) dominates overall agricultural lending in Australia, as broadacre farming is the dominant sector in terms of agricultural land use and production.

In 2024–25 aggregate lending increased in 11 of the 14 industry groups.

The broadacre cropping industry had the largest increase, with lending up by $3.3 billion.

Longer term trends in ag lending

Aggregate lending to the farm sector has increased as the farm sector has grown. In the short to medium term changes in aggregate lending are influenced by changes in the profitability of the farm sector.

Farmers tend to borrow more during periods of lower profits, and reduce borrowing when profits are higher.

There are exceptions, such as the period between 2019–20 and 2022–23 when aggregate farm debt increased significantly despite a strong increase in the net value of farm production.

This increase in debt reflected new investment in the sector funded by borrowing, coinciding with increases in agricultural land values, historically low interest rates, high average equity rates (the ratio of owned capital to total capital), and generally favourable agricultural commodity prices.

The increase in net new lending to the farm sector over the last decade also reflects a rapid increase in the price of key farming inputs, particularly land and machinery inputs.

Agricultural land prices have grown at an average rate of around 10pc per year, while tractor prices have increased at an average rate of around 12pc per year.

When new investments are funded through borrowing, rising prices lead to a greater amount of debt needed to purchase the same quantity of inputs.

As a result, part of the increase in net new lending to the farm sector is due to higher input prices, rather than an increase in the ‘quantity’ of new investment.

While the increase in net lending to the farm sector in 2023–24 likely reflected continued new investment, it is also the case that the sharp decline in farm profitability in 2023–24 will have also contributed, by delaying the repayment of existing loans and increasing the need for working capital or carry-on finance.

Higher interest rates would have also limited the capacity of some farmers to reduce the principal on loans.

Aggregate farm profitability increased in 2024–25 compared with the previous year, but stayed below 2021–22 and 2022–23 levels.

Part of the increase in overall net lending in 2024–25 reflected constraints on the capacity of some farmers to reduce debt, while other farmers may have needed additional working capital to get through the year.

The general outlook for the agriculture sector remained favourable however, so some of the increase in agricultural lending in 2024–25 would have been to fund new investment.

The full report can be found here.

Source: ABARES

HAVE YOUR SAY