SE Asia Report: From Jakarta to Hanoi – Contrasting Fortunes for Our Northern Neighbours

140th Edition: September 2025

Key Points:

- Indonesia’s demand is holding strong, supported by stable prices and new programs

- Vietnam’s livestock herds are shrinking under import pressure and high feed costs

- Australia’s disease-free status continues to underpin strong regional trust

Regional Trends and Overview

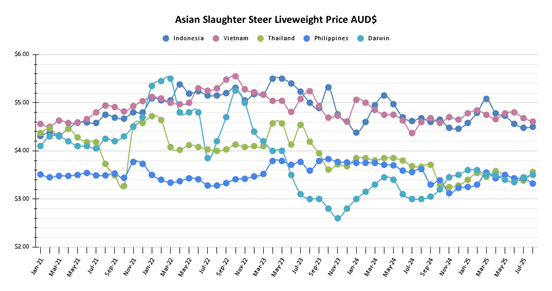

Regional Price Graph

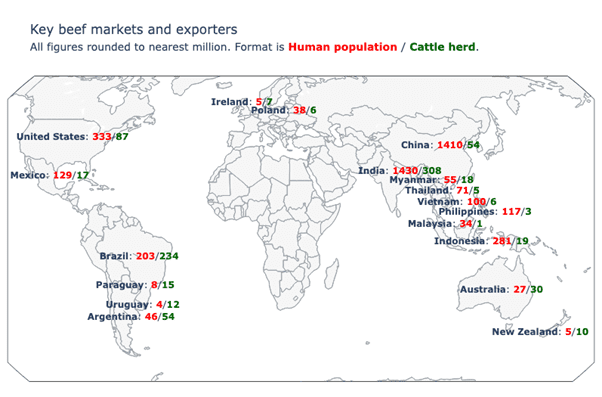

Picture: Global human and cattle(plus some buffalo) populations for major beef/cattle exporters and importers (Note: Bovine population numbers are difficult to measure accurately so these numbers should be read as ballpark figures).

Regional Herds in Perspective

When considering the fortunes of beef production and consumption in Southeast Asia, I always find that looking at total population numbers helps maintain some perspective.

It is only one piece of the puzzle and does not capture the vast differences in consumption, but it sets the scale of the supply challenge.

Dr Michael Patching

India is the outlier, with more than 1.4 billion people and over 300 million bovine, most of which are not eaten by a largely vegetarian population allowing for exports of cheap buffalo meat.

Myanmar has a relatively large herd that flows into Thailand, Vietnam and Malaysia as live cattle, while Indonesia shows the starkest gap with 280 million people and fewer than 20 million cattle.

Even small changes in beef consumption there create massive increases in demand, and with herds spread across thousands of islands, local production has little chance of keeping up. The Philippines faces the same structural limits, and elsewhere herds are flat or declining as land access and rising feed costs put pressure on beef producers.

For exporters like Australia the big populations in our neighbourhood with rising incomes are the ones least able to supply themselves and that underpins our strong position as a supplier of live cattle and beef.

For exporters like Australia the big populations in our neighbourhood with rising incomes are the ones least able to supply themselves and that underpins our strong position as a supplier of live cattle and beef.

The map above also highlights the natural privilege we have in Australia of being surrounded by sea, and not just surrounded but with a meaningful gap to our northern neighbours.

That distance has given us a biosecurity shield since settlement, when the long sea voyages meant only healthy livestock survived and our foundation herds started out relatively disease free.

We have largely maintained that disease-free status ever since (touch wood), and it remains one of our greatest trade advantages. But geography cuts both ways.

Our neighbours are close enough to remind us how fragile that position can be, with FMD and LSD present just to our north.

Indonesia: Slaughter Steers $4.50 AUD per kg live weight (IDR 10,786 = $1 AUD)

Prices

Live cattle prices across Indonesia have edged slightly higher, with Lampung recording a modest rise and Java maintaining its premium over other regions. In Lampung, bulls and steers lifted by about IDR 1,000/kg, now trading between IDR 48,000 – 49,000/kg (AUD 4.45 – 4.54/kg), while heifers remain steady at IDR 47,000 – 48,000/kg (AUD 4.36 – 4.45/kg).

On Java, bulls and steers also firmed by roughly IDR 1,000/kg (AUD 0.09/kg), now fetching IDR 50,000–52,000/kg (AUD 4.64 – 4.82/kg), while heifers continue to hold at IDR 49,000 – 50,000/kg. (AUD 4.54 – 4.64/kg) The firm pricing on Java still reflects stronger local demand and possibly tighter supply in central markets. Overall, cattle values have recovered slightly.

Photos: Local meat and livestock sales in Indonesia

Indonesia’s Unrest Spurs National Disquiet

Protests that erupted across Indonesia in late August and early September have escalated into one of President Prabowo Subianto’s greatest early challenges. What began as demonstrations over rising land taxes, parliamentary perks, and the death of a ride-hailing driver in police custody has rapidly grown into broader unrest. Several government buildings have been torched, homes of senior officials looted, and a heavy security response has been deployed, including military involvement. Market confidence has slipped, with the Jakarta stock index and rupiah both under pressure.

KITA SEHAT’s $100 Million Health Program Gives Boost to Animal Disease Response

Last month I flagged the KITA SEHAT program as one to watch, with early announcements hinting at some level of animal health involvement. The full design is now public, and while the program’s primary focus is on human health, stunting prevention and primary care reform, it also includes a meaningful stream of work on veterinary systems. As part of the $100 million, eight-year package, there is funding earmarked for disease surveillance, emergency preparedness, lab capability and professional development for paravets in selected provinces. The stated aim is to improve the animal health system overall, not just target zoonoses. That is a welcome shift in tone. The challenge, as always, will be translating national ambitions into outcomes at the district level, where vet services remain underfunded and uneven. Still, from an Australian perspective, it is encouraging to see veterinary capacity retained as part of the One Health approach and backed by long-term support. It will not be the magic pill for controlling LSD or FMD, but it should help close some of the more obvious gaps in surveillance and response capability, particularly outside Java.

Vietnam: Slaughter Steers $4.61 AUD per kg live weight (VND 17,234 = $1 AUD)

Vietnamese Herds Hollowing Out Under Weight of Cheap Imports

Vietnam’s beef and cattle sector is under serious strain, and the numbers coming through this month confirm what I have been hearing from feedlot operators and traders in recent times. Herd sizes in the south have thinned out considerably, with some operations reducing numbers by more than half compared to four years ago. High feed costs remain the main constraint, made worse by the reintroduction of a 5 percent VAT on animal feed earlier this year, which removed a key exemption the industry had relied on. Add in a weakening dong against the US dollar and producers are getting squeezed from both sides. Meanwhile, imports are surging. Brazilian pork is undercutting local product by 20 to 30 percent, and supermarket chains are selling frozen beef from Canada and Australia at just 60 to 80 percent of domestic prices. Vietnamese processors are still banking on the local preference for freshly slaughtered meat, but with chilled supply chains slowly expanding, that cultural edge may not last.

The latest herd figures confirm the trend. As of June, cattle numbers were down 0.6 percent year-on-year, and buffalo were down 3.4 percent. On paper, the national beef herd is supposed to remain stable at around 6.5 to 6.6 million head, and official forecasts even suggest a modest rise by 2026. But those projections rest on assumptions that feel increasingly detached from current conditions. Many smallholders are pulling out entirely, while others are holding on with minimal restocking. On the dairy side, growth has essentially stalled, with the national herd sitting at just two-thirds of the 2025 target. For a country that once aimed to be more self-reliant in livestock production, the outlook is firmly import-driven.

For Australia, this shift presents both opportunity and risk. Demand for imported beef will likely keep climbing if the local herd keeps going backwards, but the transition won’t be smooth. Vietnam still lacks the cold chain to fully shift from fresh to frozen, and any system that leans heavily on imports without reliable distribution is asking for trouble. Live cattle have been plugging that gap for years, supplying local abattoirs and fresh markets where fresh beef still holds a strong position against imports due to its perceived freshness. That’s not likely to change overnight, but nor is it a growth story. Volumes might hold steady, but it’s hard to imagine a big bounce. Longer term, as chilled logistics improve and habits shift, that market could tighten.

Photos: Could storage exists in some Vietnamese abattoirs but is generally on a relatively small scale like the one pictured here.

Philippines: Slaughter Steers $3.32 AUD per kg Live weight (₱37 = $1 AUD)

Prices

Livestock and meat prices have largely held steady, with wet market beef at ₱390/kg ($10.44 AUD) and supermarket rates unchanged at ₱440/kg ($11.78 AUD).

Slaughter steer prices have eased slightly to ₱124/kg ($3.32 AUD) live weight, while pork carcass remains firm at ₱240/kg ($6.42 AUD). Broiler is steady at ₱170/kg ($4.55 AUD), with supermarket-branded Magnolia broiler now trading at ₱247 ($6.61 AUD).

Photos: Local meat and livestock sales in Mindanao

Philippines imposes temporary ban on cattle, buffalo imports from France and Italy

The Philippines has introduced a temporary ban on the importation of live cattle and buffalo from France and Italy, following confirmed outbreaks of exotic animal diseases in both countries.

Italy’s National Reference Centre for Exotic Animal Diseases reported an outbreak in Orani, Nuoro, Sardegna on 18 July, while France’s veterinary office confirmed an outbreak in Chambéry on 23 June.

The Department of Agriculture (DA) said the bans were a precautionary measure to protect local herds and the wider livestock sector from the risk of disease incursion. Import shipments of live cattle, buffalo, and related genetic materials will be temporarily suspended until further notice.

Meanwhile, the latest figures from the Philippine Statistics Authority (PSA) show mixed signals in the country’s livestock production. Cattle output grew by 2.0 percent in the second quarter of 2025, while carabao production declined by 2.9 percent.

Australia: Feeder Steers Darwin $3.50

The northern dry season is winding down and cattle numbers remain strong, consistent with industry expectations of stable live export supply through 2025.

Live export capacity is holding steady, supported by a well-timed and manageable dry season that extended mustering opportunities and maintained paddock access across much of the north.

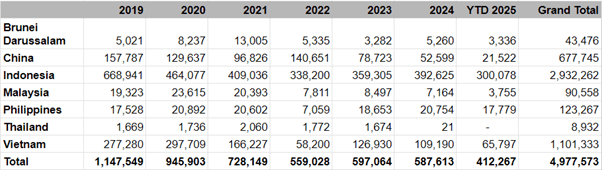

Recent data show Australian exports to Indonesia hit nearly 300,000 head from January to July, around 17 per cent above the recent five-year average and the largest year-to-date total in six years.

Seasonal forecasts support this performance. Despite drier outlooks in southern regions, northern conditions have remained favourable enough to maintain turn-off and export schedules.

Year 2025 cattle exports – comparison across SE Asian markets

Source: DAFF website