Writing in his company’s monthly property review, Herron Todd White’s Toowoomba-based valuer Bart Bowen looks into reasons why activity in the carbon space has slowed

ACTIVITY in the carbon space has generally slowed – not for a lack of interest though, as the sector continues to be the source of much conversation, differences of opinion, review and opportunity.

Some of the reduced activity stems from the expiration of a number of methodologies which had been the most widely-accepted and some of the highest-yielding in terms of ACCUs produced, particularly in the mulga belt of Queensland and northern New South Wales where human induced regeneration (HIR) had been prominent.

A new version of HIR is said to be incorporated in the new methodology called Integrated Farm and Land Management, though this replacement methodology has been in development for more than three years and remains under review.

The delay in release has been publicised as reason for the sale of a Northern Territory cattle property and a noticeable reduction in transactions in the NT.

That said, the opportunities carbon as a whole presents have continue to be a trend of discussion throughout 2024 and in 2025 to date.

A survey completed by the Carbon Market Institute found that almost two-thirds of Australian businesses (65 percent) expect Australian Carbon Credit Unit prices will be above $90 by 2035.

From my perspective, this would appear likely with more and more of the world focusing on ESG, and minimising our environmental footprint through carbon management certainly seems to be a dominant focus.

Furthermore, the safeguard mechanism in Australia appears particularly likely to see major polluters rely on ACCU generation to offset emissions. From 1 January 2025, larger companies (revenue greater than $500 million) are required to report emissions, with other in-scope entities being gradually phased in over the next two years.

Furthermore, the safeguard mechanism in Australia appears particularly likely to see major polluters rely on ACCU generation to offset emissions. From 1 January 2025, larger companies (revenue greater than $500 million) are required to report emissions, with other in-scope entities being gradually phased in over the next two years.

However, an emerging factor which could have serious implications is the growing awareness and non-acceptance of offsetting including the practice whereby a company captured under the safeguard mechanism may seek to purchase ACCUs to offset pollution they create rather than change their practices to reduce their emissions.

The downfall of Climate Active appears to be another example of changing and evolving market dynamics and expectations. More than 100 companies including Green Collar and the North Australian Pastoral Co have left the program, which was set up by the government to set standards and certify voluntary targets to reduce emissions or become carbon neutral.

Green Collar co-founder James Schulz told The Australian that the scheme had been hijacked by groups who can only look through the lens of good and bad. The government announced a review into Climate Active in 2023 though no reforms have been made since the review and pressure is being applied by opposing groups to scrap the scheme altogether.

Following the expiry of the HIR, the beef herd methodology has now also been suspended and will expire on 30 September 2025. Soil carbon methods are now in focus with the Emissions Reduction Assurance Committee undertaking a review, however the method was previously updated in 2018 and 2021 – illustrating that the carbon sequestration is still an emerging and developing industry, and legislative changes can move markets overnight.

Given this continually changing landscape, speaking with a variety of industry experts to ensure you receive balanced and independent opinions and perspectives is vitally important. Obviously, the variety of carbon farming/aggregator companies are at the forefront of establishing viable projects and are certainly well-placed to identify opportunities for generating income from the carbon industry, though this advice should be balanced by local real estate agents and, importantly, independent property valuers such as Herron Todd White.

Benefits of income diversification

Recent discussions with landholders have highlighted the benefits of the income diversification opportunities presented by carbon projects which are particularly valuable when rural income is challenged in times of drought or flood.

The example given by the landholder saw the maintenance of a baseline 3pc return on the initial purchase price of the land through the sale of ACCUs. This bought the landholder time to consider and restructure their business model following the significant correction in goat market prices.

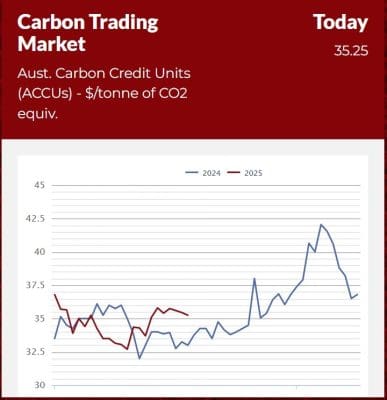

A strengthening in ACCU prices was experienced throughout 2024, particularly in the second half of the year, eventually reaching a 32 month high.

A strengthening in ACCU prices was experienced throughout 2024, particularly in the second half of the year, eventually reaching a 32 month high.

As seen in this graph from beef Central’s home-page industry dashboard, however, this is still a volatile market and obviously somewhat of a jump ship event occurred since reaching the high point in mid-November and prices have now corrected back below $38 per ACCU.

In south-western Queensland, the expiry of the HIR has certainly slowed demand for mulga property suitable under the old methodology, with transactions to aggregators speculating or looking to establish new projects on greenfield sites almost non-existent over the past six to twelve months.

That said, the credits produced under that method are certainly paying dividends and will likely help to underpin property market fundamentals in the region, providing a valuable non-rural production income stream if needed.

Similarly, the price point continues to support the development of projects under alternative methods, particularly vegetation methods, including (to paraphrase) avoided clearing, forestry and savanna fire management.

- See tonight’s separate Weekly property review, also focussed on carbon.