SE Asia Report: Strong first half for indonesia, but regional trade still finding its pace

138th Edition: July 2025

Key Points:

- Live cattle imports back in favour with Indonesian government.

- Thai-Cambodian border tensions risk disrupting regional cattle flows into southern Vietnam.

- Philippines sees steady cattle trade and strong growth in local dairy production.

Regional Trends and Overview

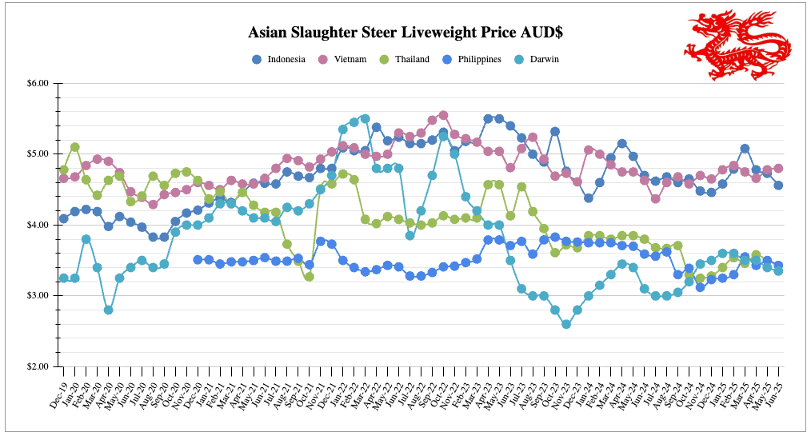

Regional Price Graph

We have been publishing this price graph for over five years now and there are some important take aways.

Firstly, while prices may appear to fluctuate in the region they are mostly a) related to changes in exchange rate with Australia b) only for a short period of time.

Within this reporting we are also largely dependent on the information we can obtain from our sources (there is no central price record), and so if this is taken into account then the reality is the price movements in the region are very small. I would confidently attribute that to the multiple cattle sources – local and imported – that exist in all of these countries, of which Australia is just one.

By far the most volatile livestock prices come from countries that would be considered as cattle exporting nations, namely Thailand and Australia. It is no new statistic that there is a large price variation out of northern Australia depending on the prevailing conditions. The interesting and important observation is that the markets that we are exporting our livestock to are not dependent on our cattle and process Australian, local, and regional cattle to make their local cattle prices relatively stable compared to Australia.

Policy is moving faster than cattle in Southeast Asia

Across key importing countries, the first half of 2025 has seen governments take a more assertive stance on food security.

From Jakarta’s removal of live cattle import quotas to Beijing’s quietly firming beef price signals, policy ambition is back in focus.

But in the paddocks and feedlots, the tone remains more cautious. Australian exporters have enjoyed a steady rebound in live cattle volumes over the past 18 months, but without stronger support from secondary markets to complement Indonesia’s solid demand, expectations for significant new growth remain muted.

But in the paddocks and feedlots, the tone remains more cautious. Australian exporters have enjoyed a steady rebound in live cattle volumes over the past 18 months, but without stronger support from secondary markets to complement Indonesia’s solid demand, expectations for significant new growth remain muted.

China continues to send mixed messages. Domestic cattle prices have risen steadily since Q2, yet breeder shipments from Australia are still sluggish. It’s not just a question of demand, it’s also about confidence. Past cycles of oversupply still linger in the minds of Chinese importers, many of whom are now taking a more conservative approach.

Tensions along the Thai-Cambodian border have disrupted cross-border trade and triggered cattle sell-offs in Buri Ram. If the situation drags on, it could affect the flow of Thai and Cambodian cattle into southern Vietnam.

Indonesia is the standout mover this month. The government’s decision to scrap import caps marks a notable shift in policy direction. Not long ago, live cattle importers were seen, literally, as a cartel in the eyes of the government. Now, they’re being framed as essential to national food security and herd rebuilding.

Indonesia: Slaughter Steers $4.56 AUD per kg live weight (IDR 10,603 = $1 AUD)

Prices

In early July, live cattle prices across Indonesia showed modest regional variation, with Java maintaining a slight premium over other regions. In Lampung, bulls and steers were trading between IDR 49,000–50,000/kg, equivalent to approximately AUD 4.62–4.71/kg, while heifers were slightly lower at IDR 47,000–48,000/kg (AUD 4.43–4.53/kg). On Java, bulls and steers were fetching IDR 51,000–52,000/kg (AUD 4.81–4.90/kg), with heifer prices in the range of IDR 49,000–50,000/kg (AUD 4.62–4.71/kg). The firm pricing on Java reflects stronger local demand and possibly tighter supply in the central market areas.

Industry and Trade Developments

Dairy ambitions draw headlines, but scale remains elusive

Indonesia’s latest shipment of 1,573 dairy cattle from Australia—split between PT Japfa (via PT Santosa Agrindo Lestari and in partnership with PT Greenfields) and PT Kironggojoyo—received significant local media attention, with at least half a dozen articles covering the event. While these imports are part of the government’s ambitious National Dairy and Meat Production Improvement Program (P2SDN), which targets one million head over five years, the scale of this individual shipment underscores how far there is still to go. At this rate, it would take hundreds of such consignments to meet the target. The fact that a single delivery is generating such fanfare suggests that progress to date has been more performative than substantive. That said, the Indonesian Quarantine Agency is clearly making an effort to communicate their biosecurity diligence, with detailed quarantine protocols and public reassurances that the animals are disease-free.

Indonesian feedlotters are now breedlotters as well

The Indonesian Ministry of Agriculture recently reported on a site visit by senior officials to PT Sapi Liar Indonesia (SLI), a feedlotter in Cikalong, West Java, as part of its push to reduce reliance on beef imports by encouraging domestic breeding. The visit highlighted the government’s expectation that feedlot companies do more than just fatten cattle—they are now being asked to take a hands-on role in growing the national breeding herd. PT SLI has begun incorporating breeders into its operation, with 150 head now allocated—just under the 3% minimum of its 4,000-head capacity required by regulation—and is working with the Ministry’s Livestock Embryo Center (BET) to carry out artificial insemination using Lembang BIB semen. However, only about 60% of the cows were assessed as having strong reproductive potential, prompting plans to tighten selection on future imports. The report made it clear that imported breeders aren’t just to meet regulatory quotas—they must be productive and contribute to local cattle development, particularly through partnerships with smallholder farmers. The fact that Ministry officials are going on-site to inspect facilities and coordinate technical work shows just how hands-on they want to be, and the level of access they now expect from private businesses. This marks a shift in the feedlotter’s role, adding complexity and cost to a model originally designed for finishing cattle, not managing breeding programs—but it’s evidently the new direction the industry has had to adapt to.

Quota removal signals intent, but impact may be limited

In June 2025, Indonesia announced the removal of quota restrictions on live cattle imports, aiming to enhance food security and support the livestock industry. While this policy change eliminates hard caps on import volumes, it does not necessarily equate to unrestricted imports. Importers still need to obtain permits and other approvals. While it’s a strong signal that the Indonesian government is factoring live cattle into its food security strategy, quotas haven’t meaningfully constrained imports in recent years. Under the Indonesia-Australia Comprehensive Economic Partnership Agreement (IA-CEPA), the tariff rate quota (TRQ) for Australian live male cattle was set at 672,669 head in 2024 and rose to 700,000 in 2025, with a 0% in-quota tariff and 2.5% out-of-quota tariff. That 700,000 head level remains the benchmark “year 6 onwards,” effectively setting a soft cap on volumes going forward. In practice, few expect the market to test that ceiling—2024 permits were issued for around 650,000 head, but actual cattle exports to Indonesia totalled only 537,274. Given current economics, and longer-term forecasts pointing to rising Australian cattle prices, there’s little appetite—or margin—for pushing beyond it. Time will tell whether this policy shift translates into real volume growth, but for now, the signal is more important than the substance.

Vietnam: Slaughter Steers $4.80 AUD per kg live weight (VND 17,045 = $1 AUD)

Industry and Trade Developments

Live cattle pricing in Vietnam continues to show a clear premium for imported animals. Thai cattle are trading around VND78,000/kg, equivalent to approximately AUD 4.58, with Myanmar cattle close behind at VND77,000–79,000/kg (AUD 4.52–4.63). Local cattle are selling slightly lower at VND69,000–71,000/kg (AUD 4.05–4.17), while buffalo are fetching between VND50,000–53,000/kg (AUD 2.93–3.11). Australian cattle remain at the top of the pricing spectrum, with bulls selling for VND81,500–82,000/kg (AUD 4.78–4.81) and steers slightly lower at VND80,500–81,000/kg (AUD 4.72–4.75). On the meat side, Australian carcasses are priced at VND175,000/kg (AUD 10.27), and boxed beef ranges from VND190,000–230,000/kg (AUD 11.15–13.50).

Adding to supply dynamics, Thailand is set to dispatch a first batch of about 2,300 live cattle to Vietnam in August. an indication of increasing regional sourcing that could further amplify pricing competition.

Feed cost relief is also emerging: Vietnam recently cut import tariffs on key feed ingredients like corn and soybean meal to zero, aiming to lower animal-feed production costs, an important offset for livestock industry pressures.

Border tensions threaten regional cattle flows

Tensions along the Thai-Cambodian border have escalated following a skirmish in late May which left one Cambodian soldier dead, prompting villagers in Buri Ram province to sell off cattle at reduced prices amid fears of evacuation. Border crossings like Chong Sai Taku have been closed by Thai authorities citing security concerns, while Cambodia has retaliated by suspending imports of Thai goods, including fuel and electricity. These restrictions have sharply curtailed cross-border trade, with daily movement at Buri Ram’s Sai Taku checkpoint dropping to under 100 Thai nationals and 40 Cambodians. The uncertainty has hit local economies hard—especially livestock farmers and small traders—despite a recent Joint Boundary Commission meeting failing to deliver any clear resolution. The situation comes amid wider political turbulence in Thailand, following the suspension of Prime Minister Paetongtarn Shinawatra in early July. If prolonged, the disruption at the border could begin to affect the flow of cattle from Thailand and Cambodia into southern Vietnam, where both countries play an important role in regional live cattle supply chains.

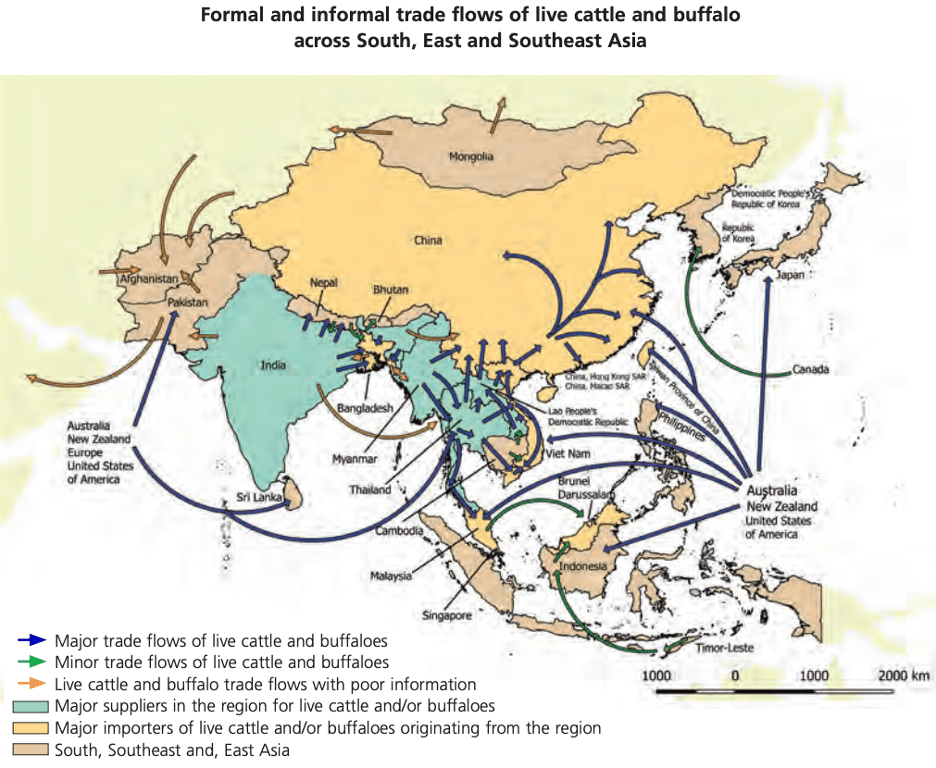

Image: Regional cattle flows

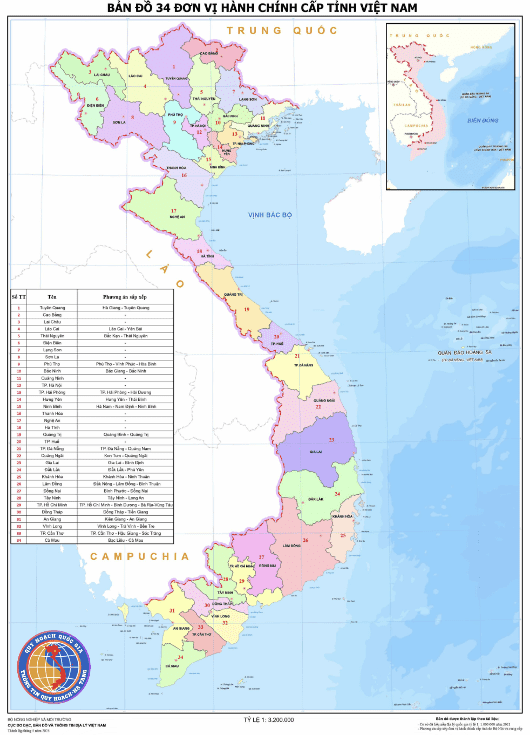

Major administrative reform alters provincial boundaries

Vietnam’s administrative reform, officially enacted on July 1, has reduced the number of provinces and cities from 63 to 34—a significant restructuring that merges many existing provincial units and dissolves the district level of local government. Among the affected areas are two provinces linked to our cattle project: Hung Yen, now merged with Thai Binh, and Quang Binh, combined with Quang Tri. These changes will shift provincial boundaries and potentially impact data collection sites, local authority engagement, and how future livestock value chain projects are administered. We’ll be watching closely to see how these adjustments affect ground-level operations and whether additional support or realignment is needed for stakeholders like NIAS, VNUA, and CRD. While Thanh Hoa and Nghe An remain unchanged, the broader move to a leaner three-tier system will undoubtedly influence how agribusiness—and live cattle logistics—function across the country.

For those trading into Vietnam the administrative border changes have functional importance as there are changes in addresses in the country all the way down to a district level. To understand the new district names follow this link.

Image: Vietnam’s New Provincial Map (34 Provinces and Cities)

Philippines: Slaughter Steers $3.43 AUD per kg Live weight (₱37 = $1 AUD)

Prices

Wet market beef prices remain steady at around ₱390/kg, though the AUD equivalent has eased slightly from ($10.92 to $10.60) due to exchange rate movement. While supermarket rates have remained at ₱440/kg, the AUD equivalent has softened from ($12.32 to $11.96), reflecting a slight exchange rate adjustment.Slaughter steer prices have edged up slightly to ₱126/kg live weight, though the AUD equivalent eased from ($3.50 to $3.43) due to currency fluctuations. Pork and broiler prices continue to firm slightly, with pork carcass now trading at ₱240/kg ($6.53 AUD), up from ₱228/kg ($6.39 AUD) last month. Broiler prices have also continued to edge up in recent weeks.

Photos: Local meat and livestock sales in Mindanao

Industry and Trade Developments

While live cattle volumes into the Philippines remain steady, much of the recent attention has turned to the dairy sector. According to the National Dairy Authority (NDA), the country’s milk production rose by 11% in the first quarter of 2025 compared to the same period last year, reaching 9.58 million liters. The growth is largely attributed to increased support for local dairy programs and herd expansion under government initiatives.

Encouragingly, the dairy cattle population has seen a 30% rise, with the NDA optimistic about achieving 2.5% local milk sufficiency by year-end. Industry sentiment remains cautiously positive, especially as broader livestock and beef imports continue to support food security and diversify protein sources in the market. However, importers note that currency movements and household purchasing power will remain key indicators to watch into the second half of the year.

Australia: Feeder Steers Darwin $3.35

Feeder steer prices out of Darwin have softened again this month, dipping to around $3.35/kg live weight. This comes in contrast to broader national trends, where feeder cattle prices have generally been on the rise. It’s a reminder that during the peak of the northern dry season, live export pricing can decouple from the rest of the country—particularly when supply for export-spec animals is at its seasonal high. Demand from Indonesia has eased slightly following a busy Qurban period, with buyers showing less urgency as they work through existing feedlot inventories. For now, the fundamentals still favour export volumes, but pricing pressure is unlikely to lift until supply tightens or offshore buying picks up again.

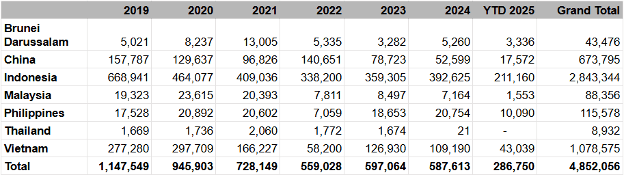

Year 2025 cattle exports – comparison across SE Asian markets

Source: DAFF website