Analyst Simon Quilty addresses last week’s World Angus Forum in Brisbane

Current record-high global beef prices are “just the start of the journey” for the Australian beef industry over the next year or two, analyst Simon Quilty told an audience of Angus industry stakeholders in Brisbane last week.

Speaking to delegates attending the Global Angus Forum staged in Brisbane, Mr Quilty emphasised the crucial role that Australian would provide in ‘backfilling’ of product that would normally come out of the US, both into the US market itself, as well as other overseas destinations.

He said the global beef trade was now moving from a supply-driven market seen in the past two and a half years, to a demand-driven market dynamic.

Mr Quilty, who works with Global Agritrends, has painted an overwhelmingly positive picture about the medium term outlook for Australian beef at recent speaking engagements, including this recent presentation to the Wagyu industry in Perth.

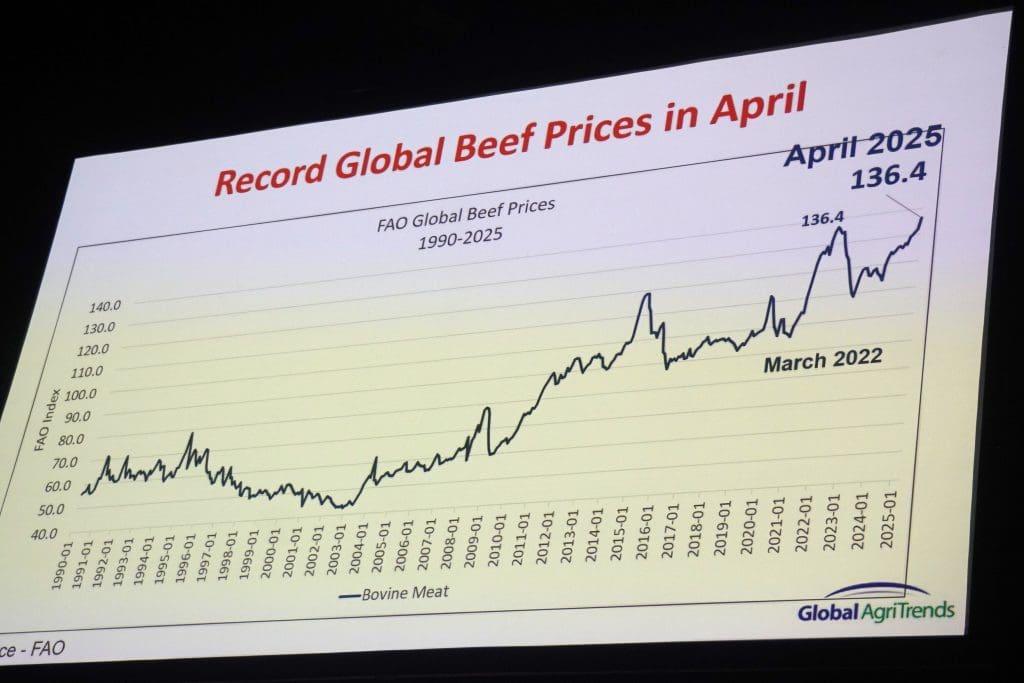

At the Brisbane Angus gathering, he presented recent statistics issued by the Food and Agriculture Organisation suggesting global beef prices had hit a record-equalling high in April (see graph).

“The last time prices were at this level in 2022 (136.4 on the FAO’s index) it was not sustainable,” he said. “That’s because it was driven (artificially) by COVID.”

“Supply became incredibly tight at the time (due to processing challenges, logistical issues and other matters) which led to the enormous peak in pricing in 2022, actually depressing cattle prices at the time.”

The second fact was stimulus money from governments at the time, driving economies around the world and pushing beef prices to record levels. When the stimulus money dried up in 2023, suddenly consumer spending was not what it was (see drop at right hand of graph).

The second fact was stimulus money from governments at the time, driving economies around the world and pushing beef prices to record levels. When the stimulus money dried up in 2023, suddenly consumer spending was not what it was (see drop at right hand of graph).

On top of that, COVID chaos meant large inventories built up globally, driving prices even lower into early 2023.

Today, however, the global beef market was in a completely different environment.

“The current peak in beef prices is the start of the journey – not the middle or the end,” Mr Quilty said. “It’s here, and this time, it’s sustainable.”

“I see tight global supplies of beef – not just in North America, but also South America – and I think Australia by the end of this year. At the same time I see exceptionally strong global demand.”

Tariffs, tariffs, tariffs

Mr Quilty provided a brief summary of the current tariff situation, much of which as been covered in Beef Central earlier.

Ten percent tariffs imposed by Trump on the rest of the world (barring China and a few others) effectively told the world, “The US is here to negotiate,” he said.

One of the major messages was that some of those countries that potentially would have gone into a downturn as a result of the extreme high tariffs, would now potentially not go into a downturn.

“The global marketplace, I think can manage a 10pc US tariff, and in particular Australia,” he said.

“I think it is in Trump’s interests to secure trade deals and not to have tariffs, and this is perhaps a catalyst. There were enormous drops in stock markets immediately after the tariffs were imposed, but today, things have quietened down. As we go forward, I expect to see more and more confidence returning to meat markets, as more and more trade agreements get put in place.”

US processor license delays

Mr Quilty said beyond US/China tariff wars, the real issue in terms of beef trade between the two countries was the delay in renewal of five-year licences for some hundreds of US beef processing operations to have access to China.

“Most were due in February and March this year – just by chance. What’s happened is that the Chinese authorities have not renewed 300 or so US beef processor licenses. Shipments out of the US were 3000t per week – they are now about 50t/week. Effectively it is a ban by the Chinese on US beef.”

How long is that ban likely to continue? Chinese delegations are due to visit beef supply countries, including Australia and the US this month, as part of a review of Safeguard policy across all Chinese imports.

That review is due for delivery in August, and Mr Quilty said Global Agritrends believed the current ban on US supply would last at least until then.

Australia was the only country in the world to have a safeguard agreement with China, setting a precedent for other countries to be forced into a similar arrangement.

“I see opportunities for Australia, as a result of this,” he said.

“We have seen enormous demand in the past month or so out of China for Australian beef, because America and Australia dominate the grainfed imported beef market into China.”

US a competitor for beef, as well as customer

Looking at tariff impacts on Australian beef, Mr Quilty said while the US was our largest export customer, taking just short of 400,000t last year, it was also our major export competitor.

“The markets we compete heavily in are Japan, Korea and the grainfed segment of China.

“In Japan, the US and Australia share 81pc of imported market share. In Korea, it’s as high as 92pc. The two of us almost have a monopoly on those markets.

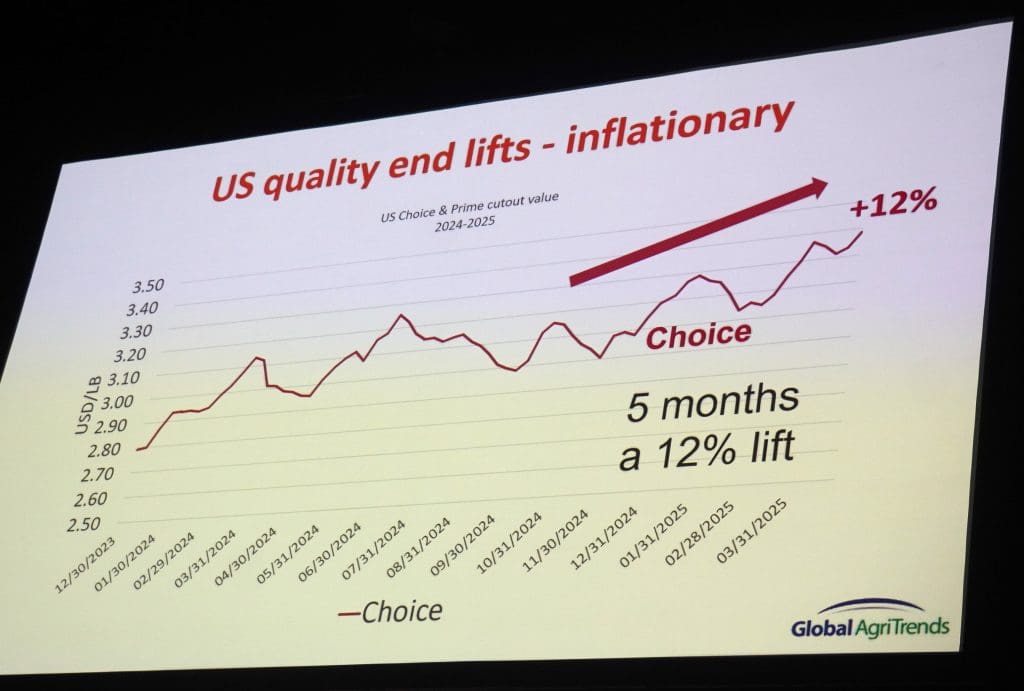

The introduction of Trump tariffs meant meat prices in the US were on the rise, now near record levels. As a result, the offerings out of the US into other markets like Korea and Japan had risen. However as the US moves closer to herd rebuild stage, US supply will inevitably tighten.

“Australia sits in a unique position, because our key markets in Japan and Korea are seeing higher prices. And as a meat trader into those markets, it creates opportunity for us – at higher prices, we are more competitive, and we have the ability to ship more volume, because American offerings are more expensive, due to the higher domestic beef prices in the US impacted by tariffs.

The same holds for China, but US competition in that market was a ‘moot point,’ while ever China’s license restrictions on US beef processors were in place.

Tariffs are going to create opportunities for Australia in Asia, Mr Quilty said.

On top of that, essential items into the US such as our lean grinding beef jumped US20c/lb in the first few days after the US tariffs were announced, because the market needed the product, despite the tariff burden.

“Those prices (10pc tariff) were passed forward to the importer and end-customer in the US. The impact on Australia has been negligible,” he said.

When it came to the cuts business, and especially higher-end cuts, the trade was a little more problematic. Already this year, USDA Choice grade beef this year had lifted 12pc, and would continue to rise.

“To me, even on cuts, as prices increase, the US marketplace will absorb that 10pc tariff cost.”

Mr Quilty made a statement at the time that the tariffs were implemented that Australian cattle and sheep prices within a month would rise, because of our ability to pass forward the tariff to US customers.

“Effectively we’ve seen that occur,” he said.

Liquidation continues in Australian herd

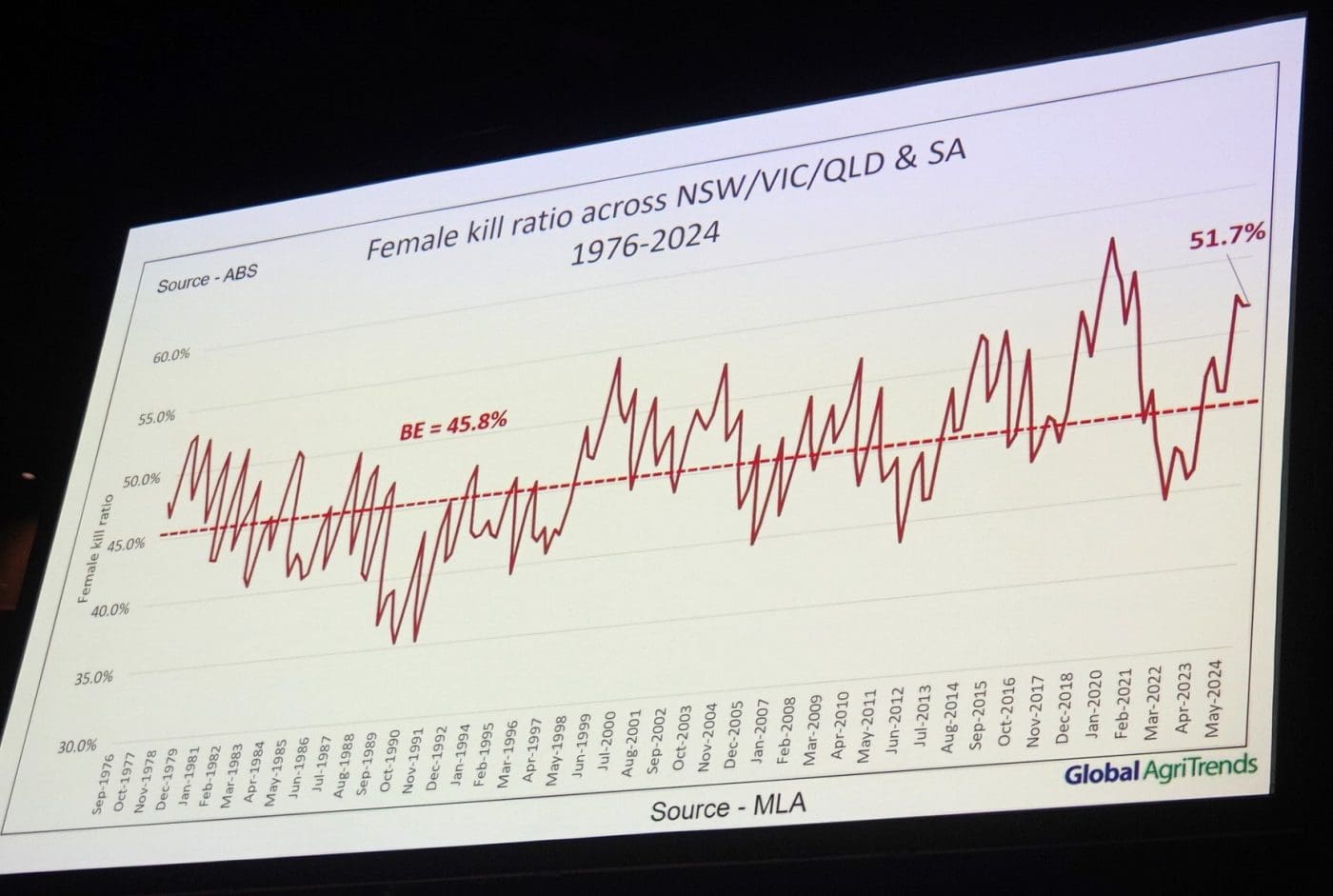

Driven by drought in some southern regions of Australia, Mr Quilty said he believed the Australian beef herd was still in liquidation phase.

The female slaughter ratio for the region NSW/QLKD/VIC/SA in the December quarter sat at 51.7pc, above the ‘equilibrium’ level for this region of 45pc (slightly different from the national figure of 45.8pc.

When female slaughter sits above that dotted line the industry was killing more than it was retaining, suggesting liquidation. There had been seven quarters of liquidation so far, the graph suggested. If it persisted, eventually herd numbers would begin to fall. He thinks by July this year, the trend will begin to move below the 45pc breakeven dotted line.

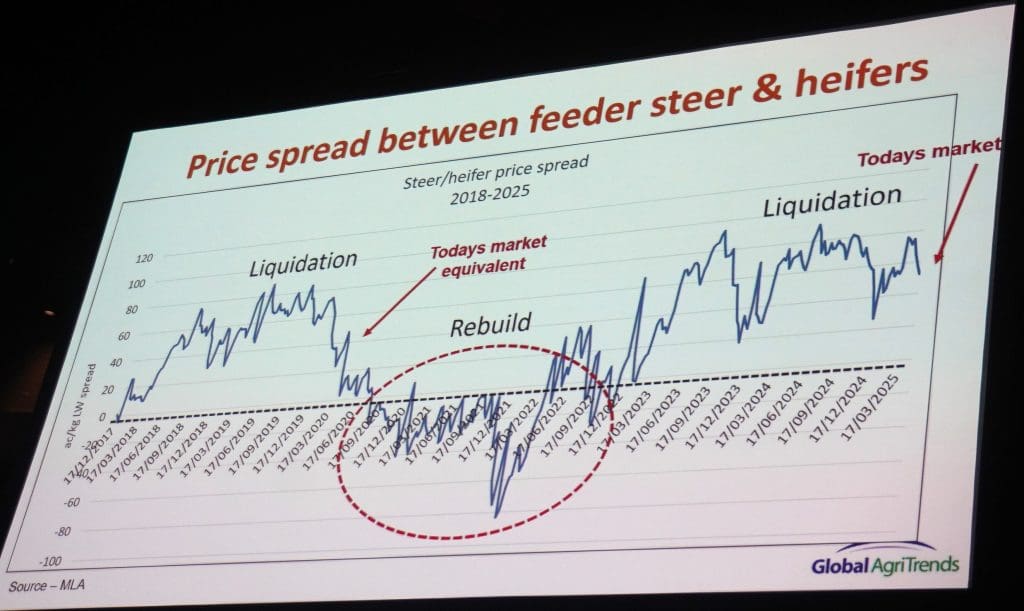

He said an important way to measure liquidation was the price spread between steers and heifers. When steers are ay a premium, when it gets to 60-80c/kg liveweight, it represents liquidation. Conversely, when heifers start to trade at a premium to steers, it’s a period of rebuild.

Today, the steer/heifer spread is about 60c/kg, but could move to breakeven by July, with heifers at a premium during the back end of this year, he said.

Reflecting the sharply contrasting seasonal conditions north and south, the spread last week in Queensland was 44c; in NSW it was 68c; and in Victoria 86c.

“To me, it’s going to be a staggered rebuild,” Mr Quilty said. Queensland will be the first to start rebuilding, followed by northern NSW, with Victoria and SA the last.

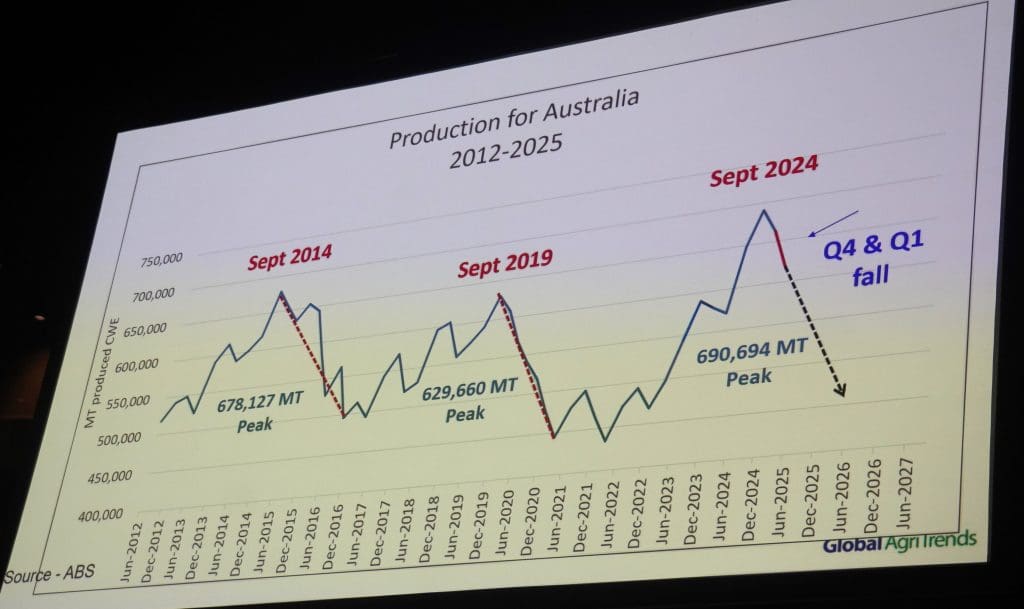

As the graph above shows, Australia hit peak beef production in September quarter last year (ABS figures), but overall – despite some recent healthy monthly export volume figures, production was starting to fall, quarter by quarter.

By the back end of this year, Mr Quilty expects production volume will be less than what’s been seen over the past two or three quarters, as the south goes into rebuild.

“Why is that important?” he asked. “Because tighter supplies and record global prices eventually starts to see the price benefits passed back to cattle producers, as competition increases with less cattle available.”

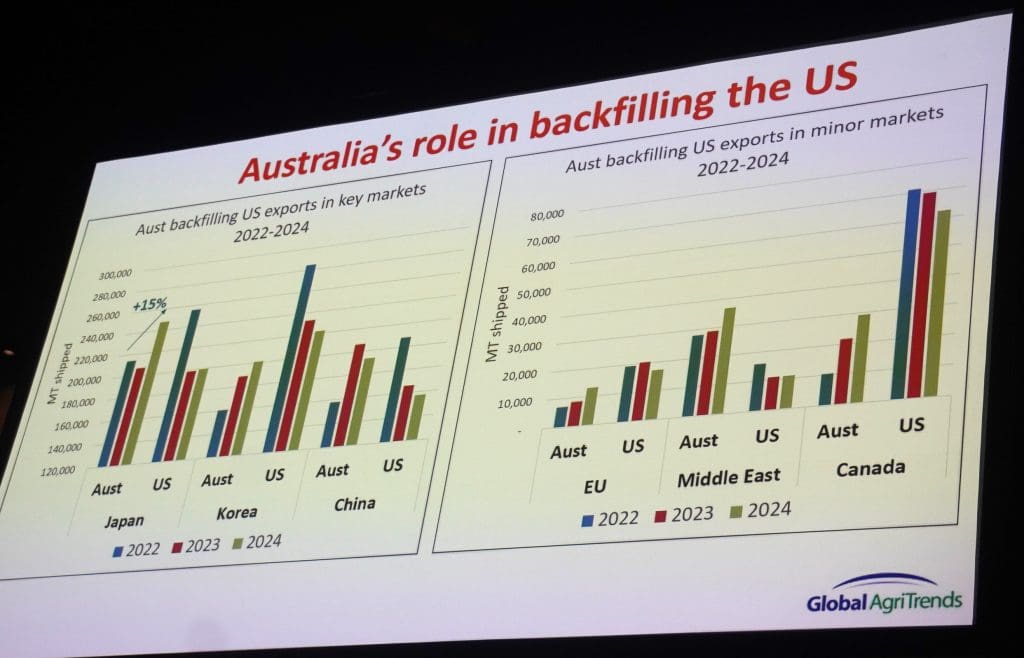

Australia fills important back-filling role

With the US herd now in liquidation for three years, the US was challenged in terms of supplying all of its domestic and export markets.

“As a result Australia has performed an important role in back-filling into global markets. America’s supply into Japan is back 22pc compared with two years ago. At the same time Australia picked up 15pc, and filled the void. The same held for Korea over the last three years – increased our volume by 24pc, while the US fell 22pc.

China was the same, where Australia lifted supply 22pc in volume, while the US fell 25pc, and similar things happened into the EU and elsewhere.

Mr Quilty said US beef prices in these markets relative to equivalent Australian beef was traditionally ‘a lot higher.’

“But I can tell you now that as we back-fill in those markets, that US beef price is not going to fall – but we are going to go up to the US price level. Currently, in China, Australia is at a 34pc discount to the US in our export values into that market. But as US supply disappears, Australian beef will go up in value, as the need increases.”

At the same time, Chinese beef cold storage inventories had fallen 20pc over the past 12 months.

“Let’s hope that continues, because the tighter that is, the greater the demand,” Mr Quilty said.

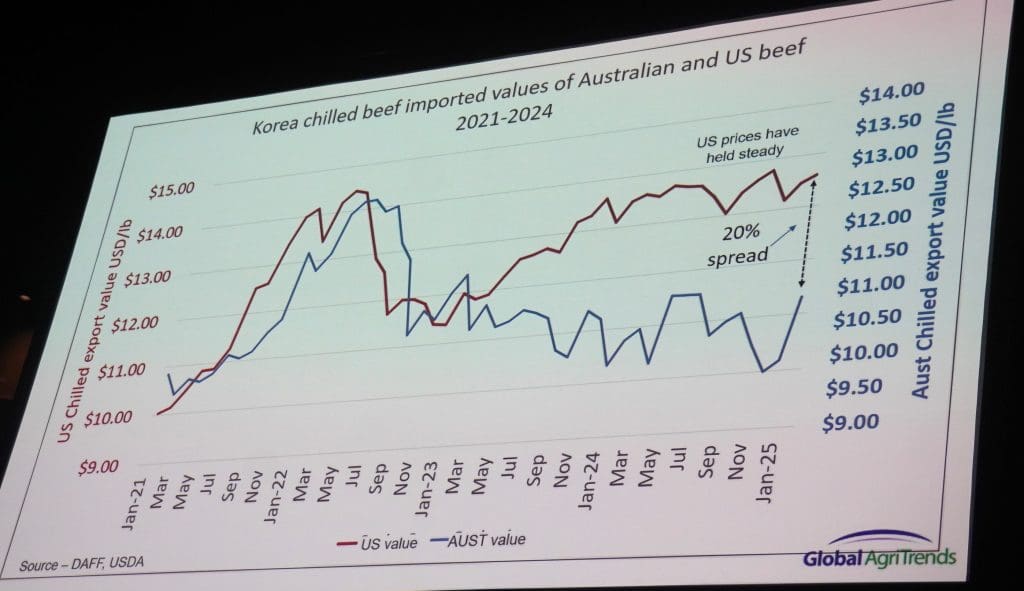

Backfilling by Australia was also happening in Korea.

There was currently a 20pc spread in export values between the US and Australian beef.

“Once again, the expectation is that Australia will be able to rise, and fill that vacuum. Back in 2021-22, we were at parity with American beef, pricewise. That will happen again, within the next 12 months, I believe,” Mr Quilty said.

What was exciting about Korea was that the country had been slaughtering its domestic Hanwoo cattle at a furious rate. The Korean Government forecasts domestic slaughtering to be down 3pc, for the first quarter this year, and down 19.4pc for the final quarter this year.

“Once again, it looks incredibly good for Australia,” he said.

Good overview of the world supply of beef at the moment.

Thanks Beef Central and Simon Quilty for the data presentation.

As with all subjective assumptions moving forward based on current geo-political (tariffs & trade war), domestic politics and future weather events the underlying economics of supply v demand always remain.

Using these likely events the outlook is positive.

However with record exports and our inability to fill the US shortfall on our own, AUD devaluation against the USD, where is the correlated rise in cattle prices here?

Sure SE Australia is in drought bringing more numbers in and our export customers had stockpiled meat most notably China but their reserves have now droppped 20% or more.

To me the answers lie with the lack of competitiveness in the processing plants industry who are all now also vertically integrated. They are looking to buy marketshare through holding export pricing especially instead of lifting pricing to fill the supply void.

It seems that its always here in Australia that retail meat prices increase but not so for Australian supplied retail meat sold overseas.

Thank you for such a comprehensive overview of the cattle industry. Please keep me posted 👍