Cattle loading onto a Wellard vessel.

KEY POINTS

- First half net profit after tax of $2.9 million

- $10.3 million turnaround from previous $7.4 million loss

- High vessel utilisation, increased cattle trading and cost savings behind improvement

- Weather and market challenges pose second half challenges

LIVE cattle exporter Wellard Limited has recorded its first half-year profit since listing on the Australian Securities Exchange in December 2015.

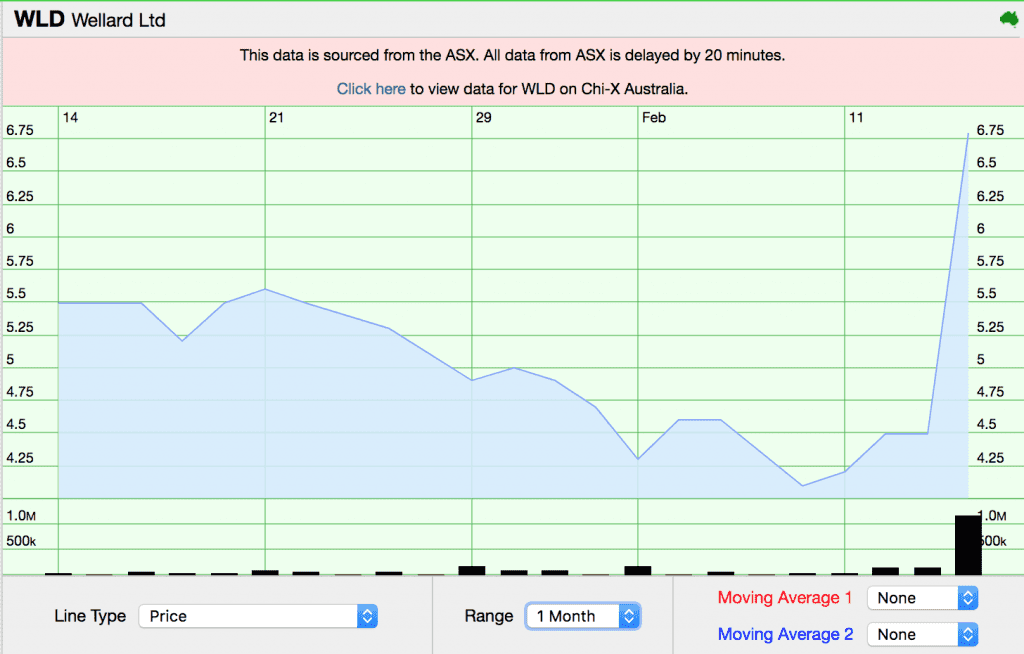

The company’s share price has responded positively to the improved result, lifting from 4.5c to 6.76c on the news of the improved result this morning.

Click on chart to enlarge

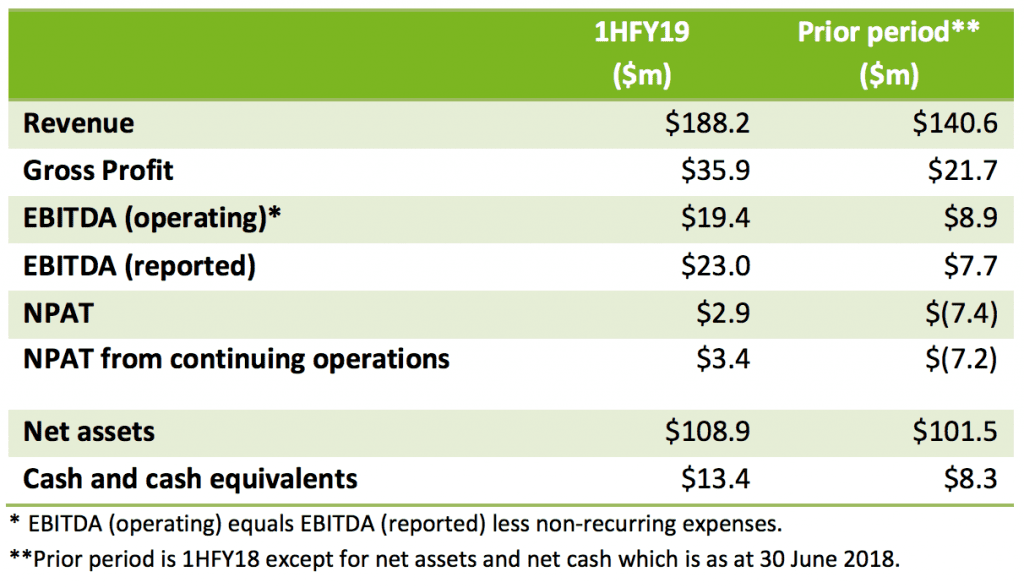

In its half-year results to 31 December, 2018, announced to the ASX today, the publicly listed WA livestock shipping and trading company posted a net profit after tax of $2.9 million, a turnaround of $10.3 million on the negative $7.4m result for the same period a year ago.

Wellard said high vessel utilisation, increased cattle trading and cost savings were behind the improved result, which saw revenue increase by 34 percent to $188.2 million.

However, it has also flagged potential challenges for the second half of the financial year, due to the ongoing shutdown of the major live export market to Turkey, continued trading challenges in key Asian markets such as Indonesia, and the impact that this month’s disastrous North Western Queensland floods are likely to have on cattle supply.

The statement notes that the company’s improved performance has enabled it to fund its own cattle purchases, and its continued focus on chartering and the associated reduction in working capital requirements has reduced its need to draw on its working capital facility.

The statement notes that the company’s improved performance has enabled it to fund its own cattle purchases, and its continued focus on chartering and the associated reduction in working capital requirements has reduced its need to draw on its working capital facility.

The company announced at its AGM in November 2018 that its trading facility with the Commonwealth Bank which had been extended to February 2019 would not be renewed. In today’s statement the company says it is confident of finalising negotiations with alternative working capital providers for a replacement facility to CBA prior to the commencement of the traditional Australian livestock supply season (more detail below).

Wellard’s statement to the ASX said the improved 1HY2019 result excludes the sale of non-core assets (Wellard Feeds business, the ‘La Bergerie’ Pre-Export Quarantine business and the Beaufort River Meats business) announced on 18 December, 2018, the proceeds of which would positively impact earnings and cashflow in the second half of the financial year upon sale completion.

The period includes an impairment of $3.5 million to the carrying value of the Group’s assets in China and $0.6 million of restructuring costs, both of which are non-recurring in nature.

Wellard said that for the second reporting period in a row it has achieved positive operating cashflow, booking a net operating cash flow of $25.8 million compared to negative $7.7 million in the prior corresponding period.

That helped Wellard boost its cash held from $8.3 million at the beginning of the reporting period to $13.4 million at its conclusion, while repaying $16.4 million in borrowings in the interim.

“It is pleasing for staff and shareholders that we were able to achieve a profit for the first time in the company’s listed history,” said Wellard’s Executive Chairman John Klepec.

“Excellent vessel utilisation, profitable cattle trading from Australia to South East Asia and continued cost savings were the key drivers for the improved operational and financial results,” he said.

“However, we are under no illusions that there still is considerable work required to reset the balance sheet, as well as to increase and provide greater repeatability of those operating results.”

“In particular, the temporary closure of cattle exports from South America to Turkey and pressure on importer and exporter margins in the trade of Australian cattle to Indonesia and Vietnam are external factors we need to manage very closely in the second half of the financial year.

“Current weather conditions in Australia, including flooding in Queensland, will delay some planned voyages, and it is not clear how much effect this will have on our full year results.”

Key elements of the 1HFY19 results relative to 1HFY18 results include:

Wellard’s full statement to the ASX this morning contiues as follows:

Operations update

The streamlining of Wellard’s operations into shipping and trading divisions is almost complete, improving the financial transparency and accountability of each division.

In the first six months of FY2019 Wellard vessels commenced 24 voyages (H1FY18: 21 voyages).

Third party exporters chartered 69pc of Wellard’s shipping capacity, with 31pc used by Wellard’s trading division. Although this was a slight reduction in third party charters compared to the prior corresponding period, charter revenue increased both in total (by 36.4pc) as well as a proportion of total revenue.

Wellard exported 95,036 cattle on 12 voyages during the period, a 21,383 head increase on the prior period.

“Increased northern Australian cattle availability and better trading margins were the key drivers of increased trading activity. The increase in the number of cattle traded by Wellard in response to a fall in Australian cattle prices in the first half of FY2019 demonstrated the advantages of the more flexible trading/chartering model the Company has implemented,” Mr Klepec said.

“Wellard is maintaining a market share of approximately 20pc in both Indonesia and Vietnam, so remains a sizeable participant in both markets.” Sheep processing volumes were down 6pc on the prior corresponding period due to restricted supply and high prices.

This will be the last full reporting period where Wellard’s Western Australian abattoir (Beaufort River Meats), its feed mill at Wongan Hills, and its Pre-Export Quarantine facility at Baldivis, are included in Wellard’s financial results – though they have been excluded from several specific financial measures in the Company’s interim report that detail results from continuing operations.

These assets were identified as non-core and are in the final stages of being sold (refer ASX announcement 18 December 2018).

The sale of these assets is expected to generate approximately $13.0 million worth of free cashflow (including working capital realisation).

In 2017 Wellard announced it has targeted a $10 million reduction in year-on-year operating and administration expenses in FY2018. That program has been very successful with expenses reducing by 28.3% in 2018, a saving of $18.8 million in FY2018.

The sustainability of those cost reductions is evident by a further $2.8 million reduction in operating and administration costs in 1HFY19, compared to 1HFY18.

There is likely to be a small increase in administration costs in the second half of the financial year associated with ongoing debt restructuring and redundancies associated with asset sales.

Wellard has maintained a strong focus on animal welfare and traceability throughout the year. No reportable animal welfare issues were recorded.

Although Wellard has limited exposure to the live sheep trade, the Company is conscious of the issues that the Australian live sheep export trade is facing and the stark reminder it provides for live cattle export industry participants that they must continue to meet community expectations with respect to animal welfare as well as investing in community engagement so that the sector retains the public’s confidence.

This remains a key area of focus for Wellard as it could have a long-term impact on a significant component of the Company’s business.

Balance Sheet

Wellard finished 1HFY19 with net assets of $108.9 million, an increase of $7.4 million from the 2018 financial year end position of $101.5 million.

The Company’s net debt position as at period end was reduced by $13.6 million, with both cash increasing and debt paid down. Cash on hand increased by $5.1 million to $13.4 million and debt reduced by $8.5 million to $136.4 million.

Despite a material improvement in the Group’s first half results, given its relatively high level of debt servicing together with the trailing nature of certain covenants, the Group continued to be in breach of banking and convertible notes covenants at 31 December 2018.

These breaches require the Company to categorise all long-term debt as a current liability, regardless of tenure. Loans and borrowings of $84.3 million in the absence of these breaches would have otherwise been classified as non-current liabilities as they are due to mature beyond 12 months from balance date.

The Group made all payments due under its working capital facility, ship financing facilities and convertible notes during the reporting period, and despite the breaches in financial covenants noted above, the Company maintains a working relationship with all of its financiers.

Update on working capital facility with Commonwealth Bank

As noted in the Chairman’s address at the Wellard Annual General Meeting in November 2018, the Commonwealth Bank has extended its trading facility to February 2019 and will not be renewed.

The Group’s improved performance during the current reporting period (enabling it to fund its own cattle purchases) and its continued focus on chartering with associated reduction in working capital requirements has reduced its need to draw on its CBA working capital facility.

The Group is finalising negotiations with alternative working capital providers for a replacement facility to CBA and is confident that funding will be available prior to the commencement of the traditional Australian livestock supply season.

Non-binding term sheets have been signed with alternative providers. A Standstill Agreement reached with Convertible Noteholders on 18 December 2018 remains in place until 31 March 2019.

Productive negotiations are proceeding towards a resolution of outstanding breaches on the convertible notes comprising several possibilities.

These include continuing early redemption of convertible notes, potential sale of a vessel, and refinancing and extending some or all of the notes.

The Board’s preferred position is to fully repay the convertible noteholders ahead of their original schedule.

Outlook

Wellard is managing several factors that are presently combining to present a challenging start to the second half of the financial year.

Three of Wellard’s 12 charter voyages in the first half of the financial year were to Turkey. Imports of cattle to Turkey remain suspended (see ASX announcement 31 December 2018) and therefore exporters are not currently chartering ships to transport cattle from South America to Turkey.

There is an expectation, but no guarantee, that this market will re-open early in Q4 FY2019, and present indications are that there will be considerable demand from Turkey for imported cattle, and therefore for ships to transport those cattle.

Exporters continue to achieve excellent voyage results on the state of the art, purpose-built vessels that comprise Wellard’s fleet.

Trading margins for Australian live cattle exports are challenging. While this is in part seasonal – reduced supply and tighter margins are created annually by the northern Australian wet season – the flooding across parts of northern Australia is likely to exacerbate the supply and price impact, and therefore trading margins, in the short to medium term.

The inability of our Asian customers to absorb higher cattle prices due to Government regulation and the cost competitiveness of alternative protein sources such as Indian buffalo meat, means that Wellard is actively managing its participation in the export of cattle to Indonesia, and will choose not to export to that market if trading margins mean the export of cattle is commercially unviable.

Consequently, Wellard did not trade cattle to Indonesia in December 2018, choosing to ship cattle to Vietnam or charter out its ships. Most of the cattle supplied to Vietnam originate from Queensland and any increase or decrease in heavy cattle turnoff as a result of flooding or other weather events will impact that market.

Nevertheless, there could be a pause in any supply for a period out of Queensland whilst growers and the country recover.

“Although we have delivered a profitable result for the interim period, we do remain concerned about the high cost of Australian cattle and the price sensitivity of Indonesian and Vietnamese customers, where the final retail pricing is Government controlled, will impact out full year results,” Mr Klepec said.

Live cattle exports to China remain a work in progress for Wellard, with progress impeded by regulations on heavy slaughter cattle and the non-issue of import permits for feeders. In response, the Company is seeking to implement a lower capital cost model in China where Wellard works in partnership with existing Chinese processors and retailers. This will allow the Company to release capital previously invested in a paddock to plate model that Wellard started building when market growth was predicted to ramp-up more quickly

Source: Wellard Ltd