This article has been prepared from a presentation delivered by financial and agribusiness consultant Ian McLean titled ‘Swelling debt and the cost/price squeeze’ at the recent AgForce regional forum in Roma.

Over the past decade, the Queensland beef industry has moved to a position where it is not making sufficient profits to cover interest costs.

Not only has total and average debt increased, but the number of businesses with debt has also increased. Wide variation in business performance exists, with some businesses still profitable in the current environment.

The perceived debt crisis in the Queensland beef industry is an issue that has been getting a lot of attention recently. Some say there is a crisis, and others say there is not.

The Queensland Rural Adjustment Authority has commissioned a series of surveys on total rural debt in Queensland since 1994, using data collected from commercial lenders. These surveys provide a good picture of the debt situation and how that has changed over time.

An analysis of changes in the levels and serviceability of debt

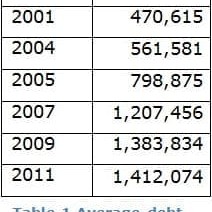

In the past 18 years, the debt of the average beef industry borrower in Queensland has increased by more than 500 percent, with most of the growth in this debt occurring of the last six years. In 2011, the average beef industry borrower had a debt of $1.4 million.

There are four main factors which cause increases in debt at an industry level:

- Low interest rates

- Prolonged droughts

- Increasing land prices, and

- Accumulated losses.

During the last decade, when we saw the increase in debt, the first three were all present.

During the last decade, when we saw the increase in debt, the first three were all present.

Low interest rates makes debt cheaper, increasing demand for it; prolonged droughts increase borrowing due to low income during droughts, feed costs and restocking following drought. Low interest rates and prolonged droughts also contribute to increase in land prices as producers purchase properties to be able to hold onto stock during dry times.

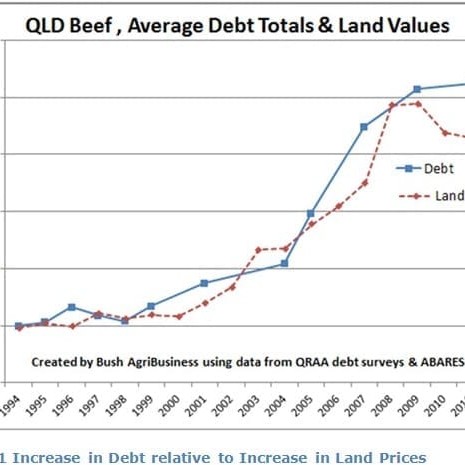

When the increase in debt over the last decade is analysed relative to the increase in land prices, it can be seen that the increases in both were largely in step, producers’ wealth increased significantly and debt increased with it, up until the correction in land values in 2009.

Since then, producers’ wealth has shrunk as land values have declined. This is shown in Figure 1, at left.

Since then, producers’ wealth has shrunk as land values have declined. This is shown in Figure 1, at left.

Serviceability of debt

An increase in debt in itself is not necessarily bad, particularly if debt is used prudently for productive purposes where the marginal return exceeds the cost of debt. Consideration needs to be given to whether industry can afford or service its debt in assessing if there is a crisis.

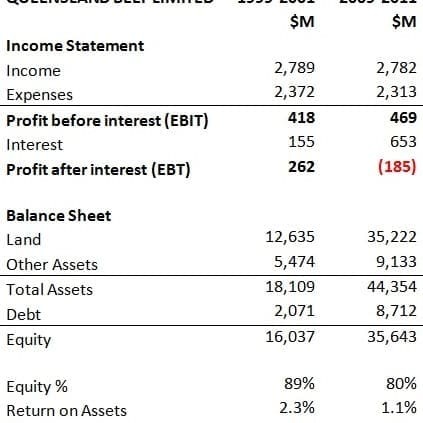

To look at how debt serviceability and business performance have changed over the last decade, information from the Australian Bureau of Agricultural and Resource Economics and Sciences and QRAA have been combined to create a consolidated set of accounts for the Queensland beef industry. This is shown in Table 2.

To look at how debt serviceability and business performance have changed over the last decade, information from the Australian Bureau of Agricultural and Resource Economics and Sciences and QRAA have been combined to create a consolidated set of accounts for the Queensland beef industry. This is shown in Table 2.

If the whole industry is viewed as one consolidated business, this is what its financial statements would look like.

This analysis is the average of two financial years at the start of the decade and at the end of the decade to look at the changes over the decade.

At the start of the last decade, the beef industry was:

- generating enough profit before interest to cover interest (2.7 times),

- paying 6c of every dollar of income out in interest,

- earning a return (before interest and tax) on assets of 2.3pc on average, before considering any capital gain.

This return on assets of 2.3pc seems low and it is important to note that business returns for producers come from two sources: operating return (business profit) and capital gain (increase in land value), with the latter usually being greater. This was definitely the case over the last decade.

The information in Table 2 is presented in nominal dollars and is not adjusted for inflation over the decade between figures, so the apparent increase is due to inflation.

When inflation is taken into account there has actually been a decline in profit over the period analysed. Another point to note is that a constant interest rate of 7.5pc has been applied to the QRAA debt figure, so the comparison shows the effect of debt changes independent of changes in the cost of debt.

By the end of the decade, the beef industry was:

- not generating enough profit to cover interest (0.7 times),

- paying nearly 25c of every dollar of income out in interest,

- earning a return on assets of 1.1pc on average, and experiencing negative capital gain.

Debt serviceability by the beef industry has fallen over the past 10 years. This has been caused more by interest increasing (through increased debt) than decreases in profit.

Did the Banks play a part?

Increases in land values increased the wealth and borrowing power of producers, the industry, as a whole borrowed against this increased equity.

The industry’s ability to afford more debt (through increased earning capacity) did not increase over the period, which has led to the situation where now the industry has more debt than it can afford.

The ultimate responsibility for the debt lies with the debt holder, who takes on the risk and returns associated with that debt. However the banks were also complicit in the situation. Just as producers borrowed largely against increased equity rather than increased earning power, the banks lent largely on increased equity rather than increased earning power.

The ultimate responsibility for the debt lies with the debt holder, who takes on the risk and returns associated with that debt. However the banks were also complicit in the situation. Just as producers borrowed largely against increased equity rather than increased earning power, the banks lent largely on increased equity rather than increased earning power.

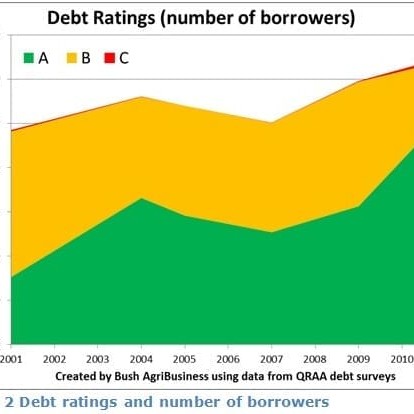

Analysis of the QRAA debt surveys shows that in 2001, when the industry as a whole was earning sufficient profit to cover interest, 31pc of beef borrowers were considered viable in all or most circumstances (A rating) by lenders.

In 2005, when the property market was booming, across all lenders there was one single beef borrower in Queensland considered not viable (C rating). In 2011, when the industry as a whole was not earning sufficient profit to cover interest, 80pc of borrowers were considered viable by lenders in all or most circumstances (A rating). This assessment does not reconcile with the profitability or debt serviceability changes in the industry shown above.

A deeper look into recent debt changes

Not only has debt increased but the number of businesses with debt has also increased.

Over the past decade, there were two significant increases in the number of beef borrowers. The first was between the 2001 and 2004 QRAA surveys when there was an increase of 16pc. From 2004 to 2009, there was a slight decrease in the number of borrowers, but there was another major increase from 2007, with a 19pc increase to 2009 and a further increase of 9pc to 2011, see figure 2.

There is no information on what the debt was used for, but the initial increase corresponds with increases in land prices.

The latter increase in numbers of borrowers occurred when the property market was in decline and sales had slowed, indicating perhaps that it was caused by new borrowers borrowing to restock, or fund continuing operations due to accumulated losses.

This increase in borrowers explains why from 2009 to 2011 the average debt per borrower increased only marginally, from $1.38m to $1.41m, while the total debt increased by $1 billion from $8.2 billion to $9.2 billion.

Looking further into the changes in debt from 2009 to 2011, if borrowers with debt rated C (not viable) are excluded, the average debt per borrower actually decreased from $1.38m to $1.33m; the average debt for those rated C increased from $0.6m in 2007 to $4.2m in 2009 and $7.6m in 2011. These C rated borrowers only accounted for 1.3pc of total borrowers in 2011, but they held 6.9pc of the debt.

Variation in debt and performance

There is wide variation in financial performance amongst all beef producing businesses and it relates to financial performance, not just debt. Client analysis by Bush AgriBusiness Pty Ltd shows there are four types of beef producing businesses:

- those without debt, they may or may not be highly profitable but are surviving without needing to borrow

- those using debt well to increase wealth and in a good financial position,

- those businesses making a profit before interest but making a loss after interest (similar to the whole of industry figures above), and

- those that are making a loss before interest, which is then compounded by interest.

What is the solution?

So what should producers do? It is essential for individual producers to have a good understanding of what their performance is.

Assess your situation: get a good understanding of what your debt, equity and profitability currently is. Look at the trends and volatility of your financial performance.

Increase profitability: there is a lot of variation in profitability of beef businesses. Even neighbouring businesses of similar size and land type can have vastly different performance. Knowing what your performance is and what your strengths & weaknesses are will allow you to focus on the areas that will lift profitability.

Restructure debt: have a look at the structure of your debt and if the package suits you. Is your overdraft getting into the black at least once a year? If not then it is being used as long term finance at a short term rate and savings can be made by moving debt to long term at a cheaper rate. Shop around to see if you can get a better deal.

Interest-only with discretionary principal payments: At times being able to pay interest only is necessary, as is the ability to pay large amounts off the principal when you are in a position to do so. Does your arrangement allow you to do this?

Asset Sales: Are there assets the business can sell to reduce debt? This depends on individual circumstance but businesses can be better off doing so.

Off-farm income: Can the business utilise its expertise and assets to generate alternate income? Or can the household earn alternate income. Don’t lose sight of the core business and there are no pots of gold at the end of rainbows.

Worked examples

Below are a couple of simple worked examples of solutions.

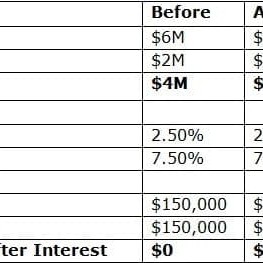

Worked Example One – Asset Sales

The fictional business has $6m of assets, with an ROA of 2.5pc, and $2m of debt costing 7.5pc. At the moment all profit is going in interest. It is able to sell $1m worth of assets to pay down debt.

The fictional business has $6m of assets, with an ROA of 2.5pc, and $2m of debt costing 7.5pc. At the moment all profit is going in interest. It is able to sell $1m worth of assets to pay down debt.

After the sale its assets are down to $5m and debt is $1m. It is assumed the ROA will fall slightly due to the business being smaller.

Even though profit has dropped, the interest has dropped more, so the business now has a profit after interest.

Worked Example Two – Increasing Profitability

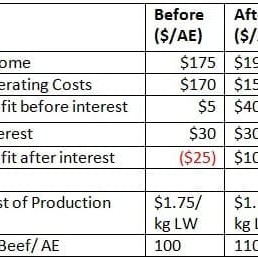

The second worked example is based on an actual business analysed by Bush AgriBusiness’s The Business Analyser. Its existing performance is in the before column to the left. At the moment it is not generating enough profit to cover interest.

The second worked example is based on an actual business analysed by Bush AgriBusiness’s The Business Analyser. Its existing performance is in the before column to the left. At the moment it is not generating enough profit to cover interest.

The strategy for this business is to increase productivity (kg beef/AE) by 10pc, primarily by holding-on to steers and selling heavier rather than weaners. As steers are retained breeder numbers will be reduced to make room for them.

This, along with improvements in labour efficiency, will reduce operating costs per AE by 10pc. If this is achieved the business increases profit per AE to a point where it can now meet its interest bill.

Summary

In summary, across the industry there is a debt problem, or more specifically a debt serviceability problem, caused by significant increases in debt without corresponding increases in profitability. Individual producers need to assess their situation and take necessary action.

![]()

- The Business Analyser is a comprehensive Business Analysis product developed by Bush AgriBusiness to help producers develop a clear understanding of how their business is performing, what its strengths and weaknesses are and where to focus attention to improve performance.

- There is assistance out there for people who may be feeling overwhelmed by their current financial situation. Talk to your family, your neighbours or services such as the Rural Financial Counselling Service, Beyond Blue or Lifeline.