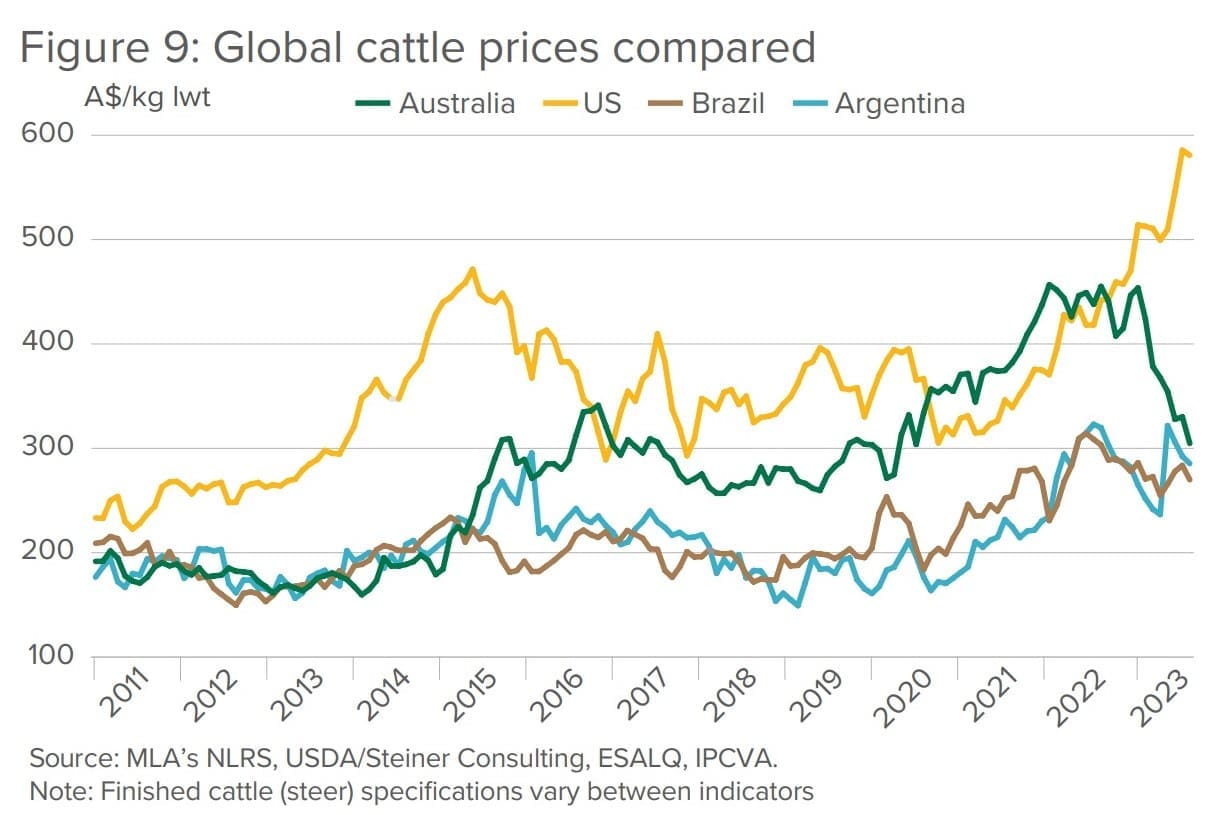

CURRENTLY at opposite ends of the drought/recovery cycle, a yawning gap has emerged between slaughter cattle prices in the United States and those in Australia.

When measured in Australian currency, c/kg terms, the price gap has never been wider over the 12 year period covered in the graph below – published as part of Meat & Livestock Australia’s mid-year Industry Projections report.

As highlighted in this earlier article published last week, US cattle prices have soared to record levels over the last few months, as supply hits the wall, following last year’s (and continuing into early this year’s) devastating US drought.

It’s producing exactly the same effect that the Australian beef industry experienced in its own post-drought recovery period, last year and the year before.

As supply gained momentum, the first half of 2023 saw rapid declines in Australian cattle prices that stand in stark contrast with prices in other major beef exporters such as the US and South America. US fed steer prices have now reached record peaks, while South American prices have remained consistent, with strong import demand from China underpinning prices despite high inflation in their domestic markets.

Click on image for a larger view

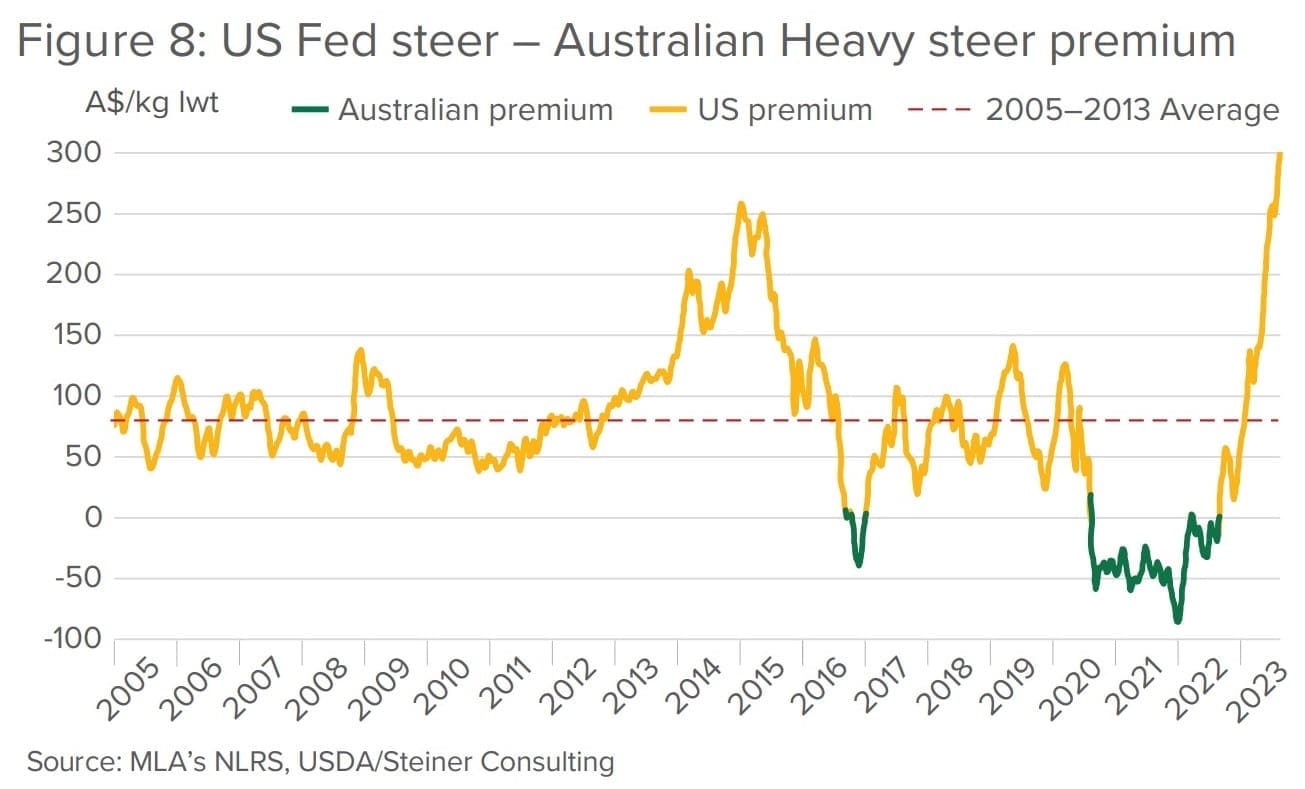

In late May 2023, the spread between the US fed steer index and the Australian heavy steer index reached A304¢/kg, a new record for the relative gap between the two indexes. Normally running between 50–100c/kg, large price movements in Australia have driven prices well out of this range since late 2022.

Worth noting on the two graphs above and below, however, Australia has had two periods (2020-22, and briefly in 2016, during the previous drought/recovery cycle either side of the Pacific) when it enjoyed the highest slaughter cattle prices in the world (among major exporters, at least).

However, it’s also worth noting that this comparison is standardised in Aussie dollars, and would look somewhat different if measured in $US or other currency.

The rapid increase in the US cattle premium since mid-2022 (yellow line) is due to increases in US prices and the decline in Australian cattle prices (green line) occurring at the same time, MLA said in yesterday’s report.

“Although slaughter remains at higher-than-expected levels in the US, declines in the beef cattle herd have raised questions about future supply among US lotfeeders and packers, creating an incentive to secure supply quickly and inflating the price,” MLA said.

The situation is reversed in Australia, with relatively high cattle stocks and a widely held expectation that supply will increase over the next several years.

This dynamic has increased the spread at a fast pace, and in the next several months the US side of the split is likely to continue growing – live cattle futures suggest that prices will continue increasing through to the end of 2023 and into 2024.

US slow-down

Despite some improvement of pasture conditions in the US recently (see today’s separate story quoting JBS’s feedlot general manager James Palfreeman, recently returned from a visit to North America), US beef production remained higher than expected in the first half of 2023. In turn, this has kept American exports higher than expected and led to changes in 2023 forecasts.

In October, the US Department of Agriculture forecast American exports at 1.39 million tonnes carcase weight and imports at 1.52mt. By April this year, those forecasts were revised to 1.59mt and 1.42mt respectively.

This shift means the global market has slightly more beef available than previously expected.

“At the same time, high slaughter means that the American herd has likely shrunk beyond what the industry expected, extending the length of time required to rebuild the US herd and therefore, decreasing future supply and inflating demand,” MLA’s Projections said.

US beef and veal production for the first quarter of 2023 was 3.1mt – 3pc below Q1 2022 levels. Slaughter only fell by 1pc over the same period, to 8.3 million head.

As such, most of the difference between 2023 and 2022 comes down to lower US carcase weights, which have fallen by 2pc to an average of 374kg cwt.

In January, 14.2 million head of cattle were on feed in the US – 4pc below 2022 levels and the lowest level since 2017.

Relatively high feed prices have increased the cost of gain for US lotfeeders, and higher prices for feeder cattle have squeezed lotfeeder margins.

Slaughter remains majority female, driving down average US carcase weights. The US female slaughter rate for Q1 2023 was 52.6pc – well above the long-run average of 47pc. Moreover, declines in beef cow slaughter have been replaced by increases in dairy cow slaughter, and the rate of heifer slaughter remains stubbornly high.

“Although slaughter is falling, the stubbornly high US female slaughter rate indicates that the US herd remains in a destock phase and means that the capacity of the herd to expand is further attenuated,” MLA’s Projections said.

“Undoubtedly, US production this year has been higher than expected. The effect of this in the short term has been reduced demand in the global economy relative to expectations, and thus slightly lower prices than could have been expected,” the report said.

In January 2023, the US herd was 89 million head (the lowest since 2014) and the beef cow herd was 29 million head (the lowest since 1964).

“In the longer term, high female slaughter means that the US herd will continue to shrink, lengthening any future rebuilding and limiting US production for the next several years,” MLA’s Projections said.

Aussie prices now close to South America’s

The graphs published above also illustrate that declining Australian slaughter cattle prices are now closer to prices seen in South America than they have ever been, since 2015.

Since 2015, a relatively consistent premium between Australian and South American prices has been seen, with Australian prices closer to US prices.

This reflects Australian beef’s appeal in terms of market access, traceability and quality control, alongside a more stable currency than commonly seen in South America.

“Recent shifts have brought Australian prices much closer to Brazil and Argentina, though still with a slight premium,” MLA’s Projections said.

“There is an equivalent premium for Australian beef over South American beef at the export level, which has not been eroded so far this year. This suggests that the underlying advantage Australian beef enjoys in the international market has been retained, but factors in the Australian market are causing the price declines rather than a fundamental issue with global demand.”

The good news is that the price difference versus US will help Australian beef’s competitiveness on international markets, at a time of growing supply.