Click on image for a larger view

AS the book closes on stud and commercial bull sales for the year, 2023 will be remembered as a tough time for many bull breeders, delivering significantly lower average prices and catalogue clearance rates compared with the previous two years.

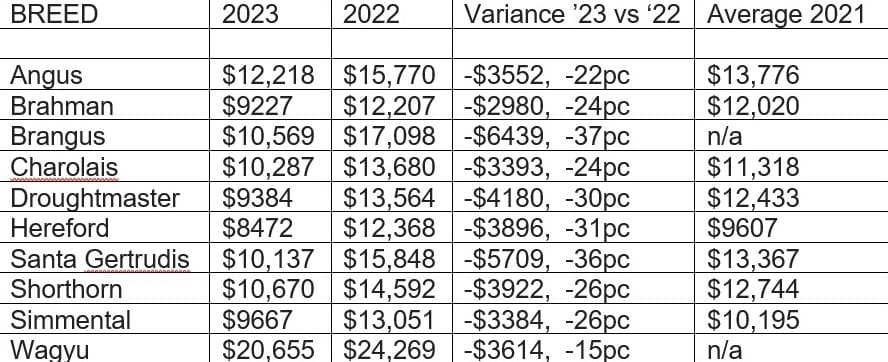

With final sales for the year held last week, Beef Central’s annual summary of the performance of ten major beef breeds’ sales performance published today shows average prices for breeds down anywhere from 15 to 37 percent this year. Sale numbers (with a couple of significant exceptions) were back by anywhere from 4pc to 12pc.

Today’s report includes this item focussing on prices paid for bulls, and a second item digging a little deeper into the number of bulls sold, clearance rates (where available), and the reasons why.

Data on sales Australia-wide is provided for auction sales only – either physical on-property or multi-vendor sales, or online – but does not cover private paddock sales, where statistics are impossible to monitor.

Data was provided in some cases by breed societies themselves, while Beef Central collated numbers in others.

Click on image for a larger view

Seasonal, cattle price impact

Clearly, the big drivers of the decline in bull prices and numbers sold this year has been the combination of deteriorating seasonal conditions as the year went on, and allied with that, the rapid decline in store and slaughter cattle prices, as supply exceeded demand and capacity.

That, in turn, clearly undermined bull buyer confidence, as BOM’s pessimistic outlook for the summer season occupied the minds of buyers everywhere.

That, in turn, clearly undermined bull buyer confidence, as BOM’s pessimistic outlook for the summer season occupied the minds of buyers everywhere.

For breeds holding both autumn and spring sales this year, the general trend in prices was down, as the year went on and commercial cattle prices deteriorated.

On top of that were some market-specific issues that impacted certain segments of the seedstock industry. A good example was the temporary suspension of the Indonesian live export trade out of northern Australia in August, due to concerns over Lumpy Skin Disease. Uncertainty over the immediate future of the Indo live trade did nothing to support demand or pricing for Bos Indicus derived bulls over the following few months.

Five year averages a better benchmark

While this year’s price results (see table and graphs) reflect a somewhat dramatic fall in average bull value over 12 months, any direct comparisons with last year may be seen as somewhat misleading.

Fuelled by the run of great seasons and record high cattle prices, 2022 bull sale results reached levels that history may ultimately see as an aberration. For this reason, it may be better to benchmark this year’s results against an average of the previous five years.

As an example, Angus bulls this year ($12,218 average) fell 22pc in comparison with 2022 ($15,770). However when compared with the Angus five-year average for years 2018-22 ($10,130) this year’s result is in fact more than $2000, or 20.6pc above the five-year benchmark. That makes the direct comparison 2023 vs 2022 look much less dramatic.

That pattern is reflected in most breeds where longer-term results are available.

Click on image for a larger view

Looking at the longer term price trend graph of average prices over the past ten years published here, it can be seen that despite this year’s sharp decline, most breeds have still had their third best result in history – exceeded only by 2021-22.

While this report is not intended as a breed-to-breed comparison or ‘popularity’ contest, it’s worth highlighting some of this year’s achievements.

Wagyu again topped the average price standings, despite selling more than twice as many bulls at auction this year as it did last year (see separate report on numbers sold).

Wagyu auction bulls this year averaged $20,655, based on data collected by Beef Central. That was down 15pc or $3614 on last year, when the breed averaged $24,269.

Next highest by average price was Angus, averaging $12,218, down 22pc in price on last year. Only eight or ten years ago, Angus were among the cheapest bulls on average being sold in Australia, based on average breed price, marking a remarkable change in demand and price expectation since then.

Four other breeds managed to maintain average prices this year above $10,000. They included Brangus ($10,569), Charolais ($10,287), Santa Gertrudis ($10,137) and Shorthorn ($10,670).

- Time and available resources limited the scope of this year’s report to the above ten larger beef breeds, each responsible for at least 680 auction sale bulls this year. Other breeds wishing to add their 2023 results are welcome to use the reader comment facility at the base of this page.

2024 Autumn bull selling season call to action for studmasters

Bull breeders wishing to promote their Autumn 2024 bull sales via ads on Beef Central’s genetics pages, daily email alert or home page early next year should contact business development manager Matt Hatchard at matt@beefcentral.com or phone on 0437 870 127. Ad spaces are starting to fill up, so we recommend making contact early to avoid disappointment.

Soon after Christmas, work will also start on compiling our full list of 2024 Upcoming Autumn 2023 Bull Sales, appearing as a searchable list in Beef Central’s genetics section. We remind studmasters to submit their 2024 autumn sale dates early next year (via this form), if they are not already provided by respective breed societies.

A number of beef breeds have re-set their record prices for bulls and registered females during 2023. Click this link to access Beef Central’s comprehensive list of breed records.

To all our loyal and enthusiastic bull sale advertising clients – many of whom have stuck with Beef Central for a decade or more – we thank you for you ongoing support and wish you, and all readers a Merry Christmas and Happy New Year.