Richard Koch, Elders

Richard Koch is an economist working with Elders. His regional cattle markets wrap follows a weekly hook-up with Elders livestock managers across the country.

THE past three months has reinforced that Australia has a predominantly grassfed production system with a grain finishing component that turns grass into beef that is mostly sold into a global market (Australia exports about 80pc of its beef production).

The predominance of our grassfed production system means that our cattle markets can sometimes behave independently of the global beef complex, because our costs of production are governed by grass availability ie. our costs of production can vary widely.

Since March, our markets have largely been influenced by local factors, as firstly, we ran out of grass and then conditions turned and now we have abundant grass to feed, creating a rollercoaster for cattle prices.

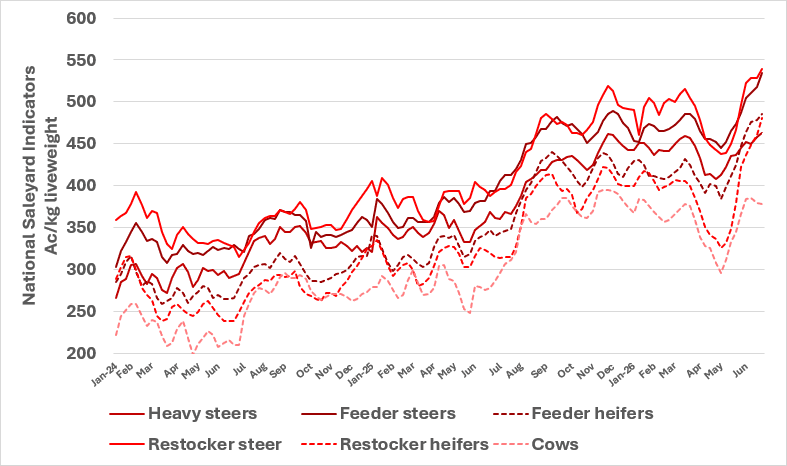

Source: MLA

This chart shows national saleyard averages for major cattle categories

The change in conditions since the end of April is of a scope that we may not see in another generation. There is hardly a region across Australia that is not firing – the mild winter has put our grassfed production system on steroids.

Given graziers are basically getting their feed for free they have the flexibility to hold on to animals to feed to heavier weights (withholding cattle from processing) and outcompete the feedlot sector as a fattener.

A consequence of our grassfed system running the show, is that competition for cattle from graziers can squeeze processing and feedlot margins. Processors are feeling the pinch of higher prices with talk that some east coast operations are looking at dropping weekend shifts and considering 4 day weeks while feeders are talking about red ink and leaving pens empty.

Export market conditions toughen

In contrast to local cattle markets, beef export market conditions toughened again last week with the announcement that we have officially filled 90pc of our beef quota to Korea. New sales to Korea effectively will be subject to the safeguard tariff of 24pc (vs 5.3pc in quota tariff) with the remaining quota already dealt with beef on the water.

Expana’s Asia-Pacific expert Junie Lin said in her APAC beef report published Friday that “The broader Australian beef export sales pace levelled off under downward pricing pressure this week. While some sellers-maintained firm offers amid high cattle costs, a series of price-taker transactions surfaced well below mainstream market levels. Australia’s export sales to Asia were “instead directed predominantly toward Japan this week”.

Attention will now turn to how Brazil reacts to it nearing safeguard levels into China. Expana reporting on Brazilian sales into China said “A mid-June lull has firmly taken hold as the buying window for pre-quota Brazilian beef effectively shuts. Spot market activity ground to a near-complete halt this week since most buyers had already completed their strategic volume bookings ahead of the looming quota exhaustion.” In recent weeks we have seen Brazilian exporters start to pivot towards the US market, lowering offers to win business. Expect an official announcement as early as next week that Brazil has filled 80% of its China quota which effectively means that the quota will be filled by product already on the water.

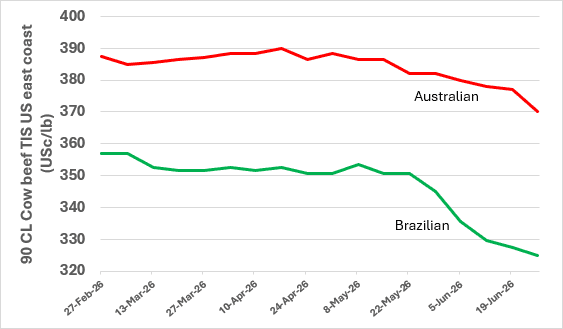

Significant fall in cow beef export values to the US

Australian 90CL cow beef export prices to the US fell 7USc/lb this week to 370USc/lb – its lowest price this year and the heaviest weekly fall witnessed in sometime. Although most of the impacts on Ac/kg returns were cushioned by the lower $A, competitive tension is building in the US with ample offerings from both Oceania and South America and US buyers comfortable with their current coverage and not interested in extending given changing market dynamics.

As Steiner reports “US beef sales start to slow-down after Labor Day while simultaneously domestic US lean beef supply starts to improve. Add to that dynamic the fact that Australia has now filled its Chinese beef quota and faces a tariff wall and Brazil will soon have to deal with the same issue. This is now clearly affecting buying sentiment.”

This chart shows 90CL cow beef values TIS in USc/lb, US east coast.

Expect to see slaughter cattle values (heavy steers and cows) soon influenced by falling international beef values as heavy QLD supplies start to come to market over the next few months.

Recently Ripley Atkinson from StoneX said “the numbers of bullocks in northern Australia has increased by 56pc or 507,000 head in the past 12 months as per MLA’s Beef Producer Intentions Survey. A clear indication that northern producers are opting to retain cattle to grow out to kill weights, to utilize the strength of the season. Cow numbers in the north are also up 17pc or 988,000 head.”

Slaughter cattle are more directly influenced by current international market conditions whereas feeder and restocker cattle are more reflective of what the markets expect the future value of cattle to be in late 2026 or early 2027 when China and Korea quotas open again.

Direct to works quotes eased again last week as processors react to margin squeeze and in anticipation of an increase in northern supply as the new financial year ticks over and ahead of some inevitable winter temperatures. Buyers were also starting to become a bit more discerning than in recent weeks.

Discussions with Elders agents revealed there were a few gaps appearing in an otherwise solid national cattle price matrix, mainly in the north, with slaughter cattle availability seasonally limited in the south.

Northern market cops a check

According to Elders agents, the northern market copped a bit of a check last week at Charters Towers. Cow prices were 20 to 25c/kg cheaper. Heavy steers were cheaper too but the offering was mostly full mouth Brahman steers that weren’t going to hit the top of anyone’s grid, but nonetheless, they were a bit subdued compared to recent months.

There was a store sale at Charter Towers on Friday with 2,000 head and it was significantly cheaper. Brahman steers under $4/kg again from $4.25 to $4.30 a week or two ago. It is probably a signal that processors and feeders are a little more comfortable supply wise than they were and the processors are becoming a bit more selective as margins get squeezed, they would rather kill a heavy 600kg southern cow than a Brahman cow that would dress out around 220-230kgs.

The live export market out of Darwin bucked the trend in prices across the north and firmed to $4.05-4.10/kg, largely because there haven’t been many Queensland cattle coming across and the live exporters are being forced to compete for the available NT supply.

Feed is still green in CQ

A full month into winter and our agents report there is still green flag coming through in buffalo country out at Blackhall. There is only one more proper cold month of July left of winter in CQ with gardeners across the region starting to prune in August.

Feeder cattle are very vibrant sitting around $5.45 to $5.50 the Downs.

There are some gaps starting to show up in the Weaner cattle market. This probably reflects the number of lighter weaners available chasing the big money available lately. Saleyards were full of them last week, with buying support coming from NSW and southern producers looking for stock to put on grazing crops to slow them down.

NSW/VIC /SA wintry yardings dominated by weaner cattle

Market conditions through NSW/VIC/SA were similar with pasture conditions improving and more rain on the way. Slaughter cattle prices are being propped up by the lack of available supply of export weight cattle.

Cows are very good still holding $4 to $4.40/kg. Heavy steers up to that sort of $5/kg with heavy heifers are generally about 30 cents behind that.

The southern feeder market is still holding up well with heavy feeders worth $5.50 to 5.90/kg. Anything lighter $5.70 to mid $6’s/kg and feeder heifers 40 to 50c/kg behind the steers at $4.70 to $5.30/kg and lighter heifers $5.40 to $5.90/kg. Feeders are setting the pace, and the blacks are pulling a premium.

Calving’s been good, the calves look magnificent, it’s going to be very interesting what weight we’ve got in them come December for calf sales.

Quiet in the west

Things have quietened right off in the west with conditions across the state generally very good. The cropping season is set up well if it keeps raining.

Cattle prices have remained extremely strong across all the cattle classes. A few more pastoral cattle – store condition steer and heifers – coming to Muchea in the last couple of weeks and are selling well. All the other sales around the place are normal for this time of year; volumes are down, prices are up.

Tassie temps remain above average but snow forecast this week

Winter temperatures have been above average with few frosts which has encouraged past growth across the state. However, this week’s forecast rain and snow may test things.

Very little saleyard activity at this time of year with most prime cattle sales are over the hooks with program yearling and grassfed Jap steers $9/kg dw up 20c/kg plus in a week. Quality beef Cows in the saleyards making $4/kg plus which is a 20c/kg rise from last week. Works are under the pump numbers wise probably a month earlier than usual. They generally take a week off in September for maintenance.

HAVE YOUR SAY