AS THIS week’s regular Eastern States kill report shows, beef processors are beginning to struggle to maintain slaughter numbers after two relentless years of drought.

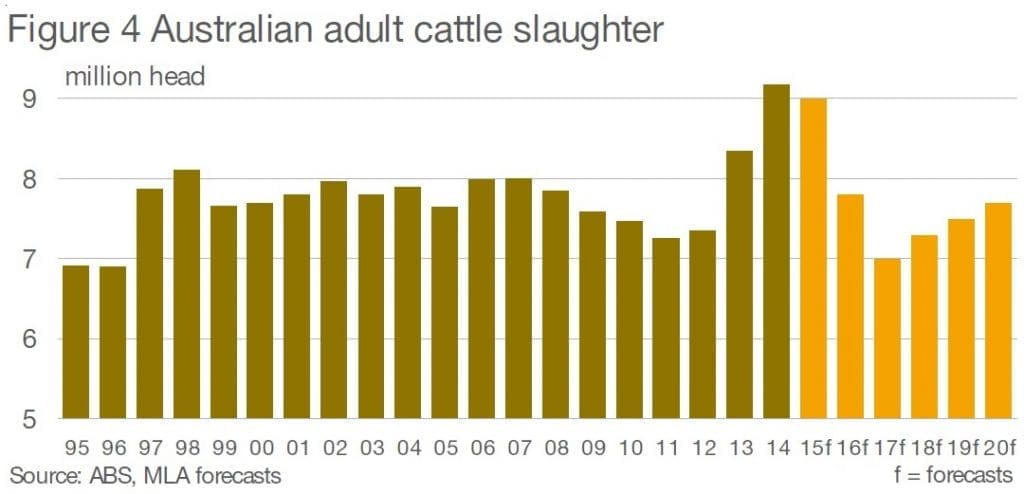

The situation is only going to get worse, with Meat & Livestock Australia predicting a slowdown in slaughter volume during the final quarter this year, before much tighter cattle supplies next year see adult cattle slaughter fall off a cliff to 7.8 million, down about 1.2m on the current year.

The situation gets worse in MLA’s projection for the following year, as the impact of drought on fertility and productivity echoes-on through the industry, with a kill predicted for 2017 at a pitifully low 6.9m head.

If these scenarios are anywhere near accurate, what does it mean for processing operations in Australia in coming years?

History may provide insight

As is often the case, history provides some guidance as to what may lie ahead, in how processors manage, and compete for, a drastically smaller pool of slaughter cattle.

We’ve dug into our dusty records and found some distinct similarities between the circumstances now bearing down on the red meat supply chain, and what happened in processing in the 2009-10 years.

In 2010, MLA records show the national beef herd shrank by almost 1.5 million head (5 percent) to 26.5 million head due to drought. For next year, MLA has a projected national herd figure of 26.1 million head – down a massive 11pc since the drought began in 2013.

“The smaller pool of cattle will put the Australian beef industry in a very interesting situation over the next five years, especially at the processing end, with slaughter in 2017 likely to be down 23pc from the 9m head slaughtered this year,” MLA’s most recently quarterly Outlook analysis says.

It’s important to put the 2010 versus 2016 comparison in some context, however. Back then, the A$ was considerably higher than it is today – averaging US91c for the year. Also, beef export demand that year was nowhere near as strong as what it currently is, or is likely to be next year.

But equally, at the other end of the value scale, cattle prices in 2010 were nothing like today’s values. The EYCI figure in July 2010, for example, was around 350c/kg. Today’s its 566.5c/kg.

Despite those differences, we think there is some information to be gleaned from processor reaction to a very tight cattle supply situation in that 2009-10 period that may provide some insight as to what happens next.

A number of things happened across the processing industry during the 2009-10 period of poor cattle supply, and lower processor profitability.

A number of smaller independent processors closed permanently. In Queensland, the list included Killarney and Pittsworth.

In an interview with this writer, Teys Bros managing director Brad Teys described the processing environment at the time as a “war of attrition.”

Small operators were not the only ones being hit by pressures, however. Some of the nation’s biggest beef factories also showed the signs of stress.

Teys’ Lakes Creek plant at Rockhampton started its 2010 kill very late in the season, and only then on a four-day weekly roster. Its sister plant at Biloela dropped kills from 750 head/day to 550.

For the 2009 calendar year, Teys produced at least 15pc less beef by volume than in earlier stronger years like 2005 and 2006, with a ‘lot of days off’ recorded during the season, Brad Teys said at the time.

The nation’s largest processor, Swift Australia (now JBS Australia) also wound-back its killing operations in 2010.

The company’s northernmost plant at Townsville, most directly exposed to competitive pressure for livestock from live export, shed 267 employees at the start of the year, dropping weekend shifts and reducing kills by about one-third. Swift pointed out at the time that the move would strip about $14 million in wages annually out of the local economy and $70 million when the flow-on effect was added.

Even Swift’s flagship Dinmore plant near Brisbane dropped from 11 to 9 shifts over a five-day week, in light of the livestock supply and demand challenges.

If those events are anything to go by, circumstances next year and the year after are likely to be worse.

Kills may drop to 130,000 head

“The 2009 and 2010 years were f*ing hard,” a respected former senior meat processing executive told Beef Central yesterday.

He suggested, based on current expectations, that somehow, eastern states weekly kills would have to ‘lose’ another 30,000 head per week during the cattle shortage period next year and perhaps the year after that. That’s based on current kills around 160,000 head, suggesting a slaughter figure of just 130,000 head, or thereabouts.

How big is that adjustment? To put it into some sort of context, its roughly equivalent to the permanent closure for the next two years of JBS Dinmore and Teys Beenleigh.

But for that sort of adjustment in processing rates to occur across Eastern Australia, something obviously has to ‘give.’

Our processor contact agreed with Beef Central’s basic summary of the sequence that may unfold heading into next year to manage that, as follows:

The first aspect to change is processors jettisoning weekend shifts and overtime, that extend killing capacity during times of gross oversupply like that experienced over the past two drought years. That’s already happened.

The second is dropping normal weekly shifts, to better-align kill capacity with available supply. That’s already happening in southern Australia, where considerable numbers of processors are already operating on four-day and even three-day weeks, as cattle supply runs short. Even further north, large plants like JBS Scone have skipped a series of Friday shifts in the past month, as the full effect of the big reduction in herd size starts to filter through the supply chain.

For plants with double-shifts daily, there’s the prospect of reverting to a single daily shift, without compromising efficiency too drastically.

The third is temporary or even permanent plant closures – either adding ‘dark days’ during the normal seasonal plant closures for maintenance, or closing for weeks, even months, at other times of year. There’s no shortage of examples of that happening in the past, when cattle were short, and cattle prices became prohibitive.

Late seasonal starts after the Christmas/New Year break could also be on the horizon. Instead of returning to working by mid-January, some northern sheds might not recommence their kills until well into February. In the tough 2009 year, for example, the first week’s kill at JBS Townsville was in week 11 (effectively, mid-March). Such a cycle was somewhat routine years ago, when plants were under less pressure to maximise utilisation. Equally, large southern plants have had limited yearly down-time over the past couple of years, but that may now change.

One action processors are very wary of is opening a plant for a season, only having to close it again due to lack of supply. That’s because many awards and agreements require a month’s notice to staff, which can cost processors a fortune if they have to close again, unexpectedly, when cattle run out.

Fourth is strategic plant closures of sites owned by multi-site processors. Given what lies ahead, it’s been suggested to Beef Central that companies like JBS or Teys might consider closing one plant for a period, in order to ‘preserve’ a higher (and thus more efficient) rate of throughput at another, within the same geographic region. A similar pattern is being seen in the US, facing 40-year lows in its beef herd size, where major beef processors including Cargill and Tyson have recently shuttered large, modern beef plants in order to support kills at other company-owned sites. “The realities of the beef business have changed, and we must continue to change with it to remain successful,” Tyson’s Steve Stouffer said. “US cattle supply is tight, and there’s an excess of beef production capacity in the region.”

There’s a view now emerging that processors are now nearing their financial threshold on slaughter cattle price – meaning there may not be a lot left in the tank to compete with, as cattle supply gradually recedes. Most hopes now rest on what happens with world meat prices. If exporters can successfully push meat prices to another level from where they currently sit, there may yet be another step left, in upwards cattle price movements.

Service kill competition likely to grow

Beef Central’s processing contact sees the likelihood of several other events occurring, as cattle supply pressure grows over the next two years.

Service kills is a good example. Service kill has become acutely difficult to find over the past two years, as processing infrastructure owners have quickly understood that they could make a lot more money on the trade, killing and exporting their own cattle, rather than providing a fee-for-service kill for others.

Beef Central itself has had numerous calls from stakeholders over the past two years wanting to know where they might possibly get a service kill done.

It’s led to a number of long-term ‘tenants’ being kicked-out over the past two years, as plant owners moved to allocate their entire kill capacity to company-owned cattle. But as plants find it harder to fill kill rosters next year, it’s entirely possible that far greater competition might again re-emerge for service kills for larger brand supply chain managers.

Who’s going to fall over?

Given the financial and productivity challenges outlined above through declining slaughter numbers, the question might be asked: Who’s going to fall over?

In the past, during tough supply times like this, it’s tended to be single-site plants in less well-located areas to supply, lacking supply chain integration or marketing strength, who perhaps operate in a narrow market segment.

Plants not being well-upgraded for efficiency could be another factor, as could plants more heavily exposed to live export market competition. Queensland’s Morex Meats and before that, KR Darling Downs are perhaps prime examples of the sort of businesses that could not sustain the pressure.

We’ll let readers draw their own conclusions.