If you read The Cost of Doing Nothing on Beef Central a couple of weeks ago, about our 714-hectare model farm in North East Victoria – thank you.

The general idea came from overhearing people talking about skipping fertiliser to save money, and it got me thinking about what is the true cost of doing nothing. Do you actually save money, and how does it affect production longer term?

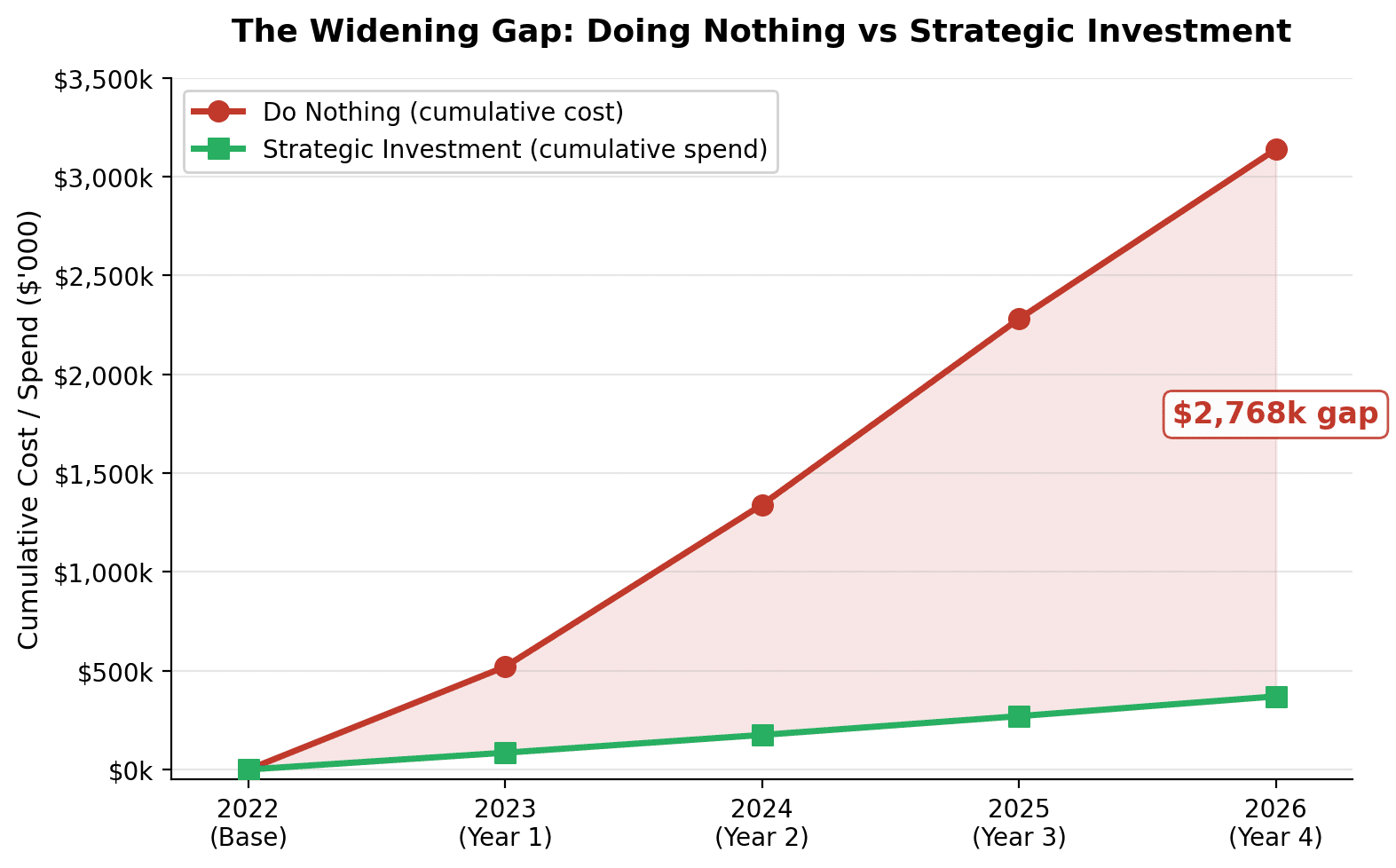

So I built a farm model based on a 714-hectare property in North East Victoria running 10,000 DSE on mixed granite and alluvial country, and went about simulating a few years of production using Victorian Farm Monitor Project data as the base. What the model showed me was ‘doing nothing’ destroyed $3.13 million in value. The soil acidified, the clover vanished, the aluminium poisoned the root zone, and the farm collapsed to 40% of capacity.

Then, within a few days the Strait of Hormuz closed, sending our long-term input prices sky high with no real way of knowing if this is a short-term or a long-term disruption.

So what is the current cost of ‘doing something in 2026’, and as farmers, can we still afford to do something?

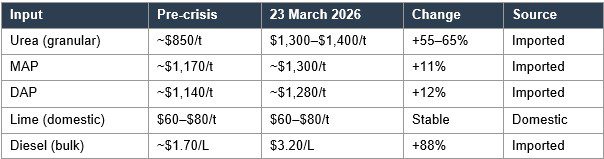

Input Prices: Pre-crisis vs now

Australia imports 69% of its urea from the Middle East. That supply line is severed. The last vessels to exit Hormuz before the conflict are berthing this week. After that, resellers aren’t taking orders until replacement cargoes arrive from Southeast Asia. China stopped UAN exports on 13 March. The RBA hiked twice to a cash rate of 4.10%.

I’m sure everyone is having the same thoughts and conversations at the moment. Should I wait and sit this out, or should I bite the bullet and take a long-term view?

Waiting is a strategy

Waiting is a strategy. It’s just not the one people think it is.

When you say “I’ll wait for urea to come down,” what you’re actually saying is: I’ll let my pasture produce 4,500–5,000 kg DM/ha instead of 10,000–11,500. I’ll buy hay at 30–40 cents a kilo of utilised dry matter instead of growing it for under 10 cents. I’ll turn off lighter animals into the commodity end of the market – the exact segment under pressure from Brazil and the China safeguard, instead of quality feeders into a market where those animals are up 26–41% year-on-year. And I’ll let the soil pH keep dropping toward 4.8 while the aluminium creeps up and the phalaris roots get shorter.

That might seem like waiting, but you end up paying three to four times as much per kilogram of dry matter, have lowered productivity and fertility in cattle, and compound a remediation bill that’s now being financed at 4.10% plus. The problems multiply and you end up deferring a cost that gets bigger every year.

Three options for 2026

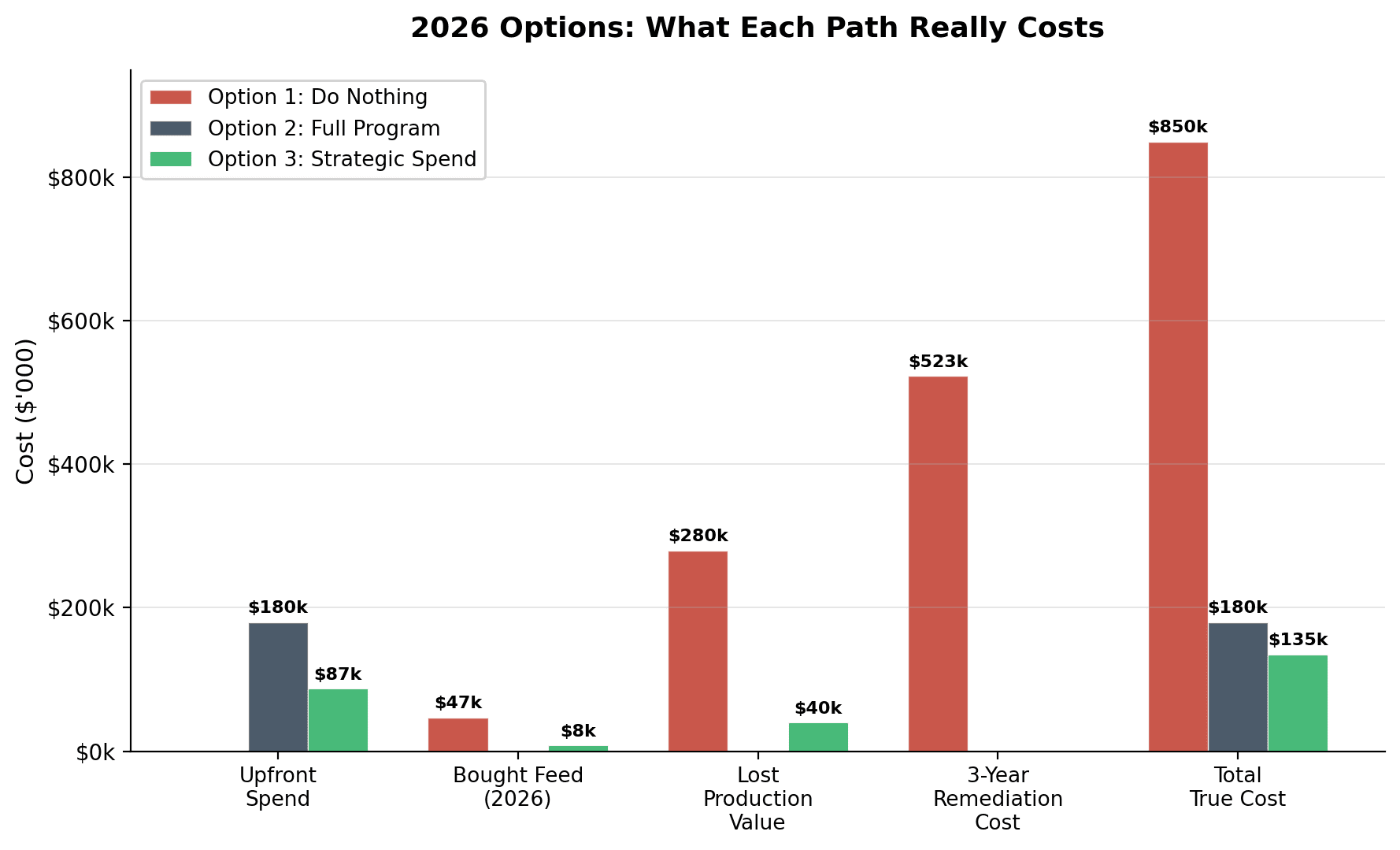

On our model farm we currently have a few options for 2026, but which is the best one? The model runs off the same 714 hectares, same North East Victorian region, same soil types from Part 1.

Option 1: Do nothing. Skip fertiliser again. “Save” $54,000 in 2022 dollars, which is worth about $42,660 in 2026 purchasing power after 21.4% cumulative inflation. Meanwhile, spend $35,000–$60,000 on bought-in feed at three to four times the cost of growing it yourself, produce lighter animals weaners and lower cattle fertility. Compound the capital reset bill from Part 1, which is now being financed at 4.10%plus instead of 3.35%. The $3.13 million cost hasn’t improved, it’s gotten worse.

Option 2: Full program at crisis prices. Capital lime on all the acid country. Maintenance phosphorus on all 714 hectares. Nitrogen across the farm at the equivalent of $1,400/t urea. Total bill: $160,000–$200,000. That’s a bill that’s tripled from 2022. It’s confronting, and it assumes you can actually source the urea – which right now, you probably can’t.

Option 3: The one I chose. Concentrate the spend where the return is fastest. Accept that some things have to wait. Here’s what that looks like:

Option 3: The strategic spend

Lime the acid country. Non-negotiable. $43,000–$57,000 on 285 hectares. Lime is the one input that hasn’t been touched by the Hormuz crisis – it’s domestic, it’s stable, and it’s protecting the single most important thing on the farm: the pH. Every year you defer lime on granite soil is a year closer to the aluminium cliff. Once you’re below 4.8, you’re not managing a healthy pasture anymore, you’re managing one affected by aluminium toxicity. No amount of phosphorus or nitrogen will work if the pH is wrong. This is the highest-return investment available in 2026 and it’s sitting right there at $60–$80 a tonne.

Phosphorus on the best country. The heavy soils near the creek lines – higher clay, higher CEC – produce 50%+ of the farm’s dry matter. A maintenance application of single super on the best 200–250 hectares is a sensible spend even at elevated prices. Phosphate hasn’t spiked as hard as urea and supply is currently more stable. Cost: $20,000–$30,000. The light granite hills? They can wait 12 months, provided you’ve limed them. Lime buys you time and time buys you options.

Legumes instead of urea. This is the year to soil test your clover and invest in inoculation. $15 a hectare for sub clover this autumn returns more nitrogen per dollar than any bag of urea at current prices. A 30% clover content supplies 30–50 kg of nitrogen per hectare per year. That’s free nitrogen, produced by biology, not by a factory on the other side of a war zone. Cost: $4,000–$6,000.

No urea. At $1,400/t – if you can even get it – blanket nitrogen on pasture doesn’t stack up. If there’s an absolute need to put nitrogen on then liquid UAN is still available as an alternative, it runs at 32% N, lower volatilisation risk, and CSBP still manufactures Flexi-N locally. But you need spray or dribble bar gear, and China’s stopped exporting UAN too, so supply is tightening. For most pasture operations, the honest answer in 2026 is: let the legumes do it.

Total: $67,000–$107,000. Roughly half the full program, which isn’t ideal, but it’s still ensuring your soil isn’t being mined.

| For every dollar you “save” by skipping fertiliser, you’ll spend three to four dollars buying feed, losing production, and fixing the damage later.

Hay is more expensive because diesel is $3.20. The remediation bill is more expensive because interest rates are 4.10%. And the cattle you’re NOT producing are worth more than they were -feeder steers up 26%, heavy steers up 41%, so the opportunity cost of an unproductive farm has increased too. Diesel prices are temporary, a flow cost that hurts this season’s margins but doesn’t compound. Urea prices are temporary, they’ll correct when shipping routes reopen. Soil degradation is permanent. Once pH drops below 4.8 and aluminium poisons the root zone, you’re looking at years and hundreds of thousands to fix it. That’s not a cost you can defer. It’s a cost that grows every year you try to. The gap between doing something smart and doing nothing is wider in 2026 than it was in 2022. Not narrower. |

We’ve been here before

In 2022, urea hit $1,600 during the Ukraine shock. Diesel went through the roof and a lot of people talked about pulling back.

Benchmarking data from the Livestock Farm Monitor Project shows the producers who came out of that period strongest weren’t the ones who did nothing. They were the ones who did exactly what I’m describing here: they limed what they could, put phosphorus on their best country, deferred nitrogen, and leaned on legumes. They didn’t spend full dollar on every hectare, but they didn’t walk away from the soil either. When prices corrected in 2023–24 and cattle values lifted, those farms had the carrying capacity to capture the upswing. LFMP data for Northern Victoria shows the top-quartile operators maintained stocking rates 20–30% higher through the recovery than producers who had pulled back entirely, and their cost of production per kilogram of liveweight was lower, not higher, because they were growing feed instead of buying it.

The farms that did nothing came into the recovery with bare paddocks, acid soils, and a remediation bill that ate everything they’d “saved.”

The realistic answer

I’m sure there are a lot of people asking whether this is really the right time to be spending $80,000 on fertiliser when the news is full of war, fuel shortages, and interest rate rises. That’s a fair question, and it deserves a better answer than “the soil science says so.”

The realistic answer is: we’re not spending because we’re comfortable, we’re spending because doing nothing costs three to four times as much over the next three years. The $80,000 isn’t a luxury. It’s the cheapest path forward. The expensive path is the one where we buy feed at 30–40 cents a kilo, turn off lighter animals, and then face a $523,000 remediation bill at interest rates we can’t predict.

In Part 1, I wrote that doing nothing isn’t regenerative. It’s extractive.

In Part 2, the message is simpler: doing something in 2026 is harder, more expensive, and more confronting than it’s ever been. But the cost of doing something, even a strategically reduced something, is still a fraction of the cost of doing nothing. And the opportunity cost of missing the upswing, because your farm couldn’t produce when the market needed it most, may be the biggest cost of all.

Data sources

ABARES March 2026 Outlook, Episode3 Fair Value Model & Cattle Pricing, Simon Quilty / Global AgriTrends, ACCC Fuel Price Monitoring, MLA Cattle Projections & NLRS, UNCTAD Strait of Hormuz Analysis, RBA March 2026 Statement, LFMP Northern Victoria, Argus Media / Grain Central Fertiliser Reports, Fertilizer Australia. Prices as at 23 March 2026.