149th Edition: July 2026

Key Points:

- NOAA has declared an El Nino, formed in June and tipped to strengthen into 2027, and across Indonesia, Thailand and the Philippines governments have moved from watching to spending.

- A dry year’s feed and disease stress lands on the part of the Indonesian trade already squeezed between a capped feedlot price and dearer Australian cattle.

- Manila is building home-grown foot-and-mouth and swine fever vaccine capability.

Regional Trends and Overview

Dr Michael Patching

The big story this month is a weather one. In June the US National Oceanic and Atmospheric Administration declared an El Nino had formed, and to my mind it is the single factor most likely to shape the Southeast Asian beef trade over the coming year. Indonesia’s weather bureau, BMKG, puts the dry-season peak across July to September, the FAO has flagged much of the region as high drought risk, and one local outlet has called it potentially the strongest in 75 years.

What matters to me is that governments are acting on it. A dry year hits this trade three ways at once, and unevenly. It lifts feed costs and squeezes feedlot margins. It raises disease pressure, since heat and stress are when foot and mouth and lumpy skin move. And it widens the import gap, because local production buckles first. Each market I cover is exposed on a different front. The years I keep coming back to are 2015-16 and 2023-24, neither kind to the live trade, and what gives this one its edge is that it lands with the Indonesian feeder trade already strained and Australia’s own supply turning at once.

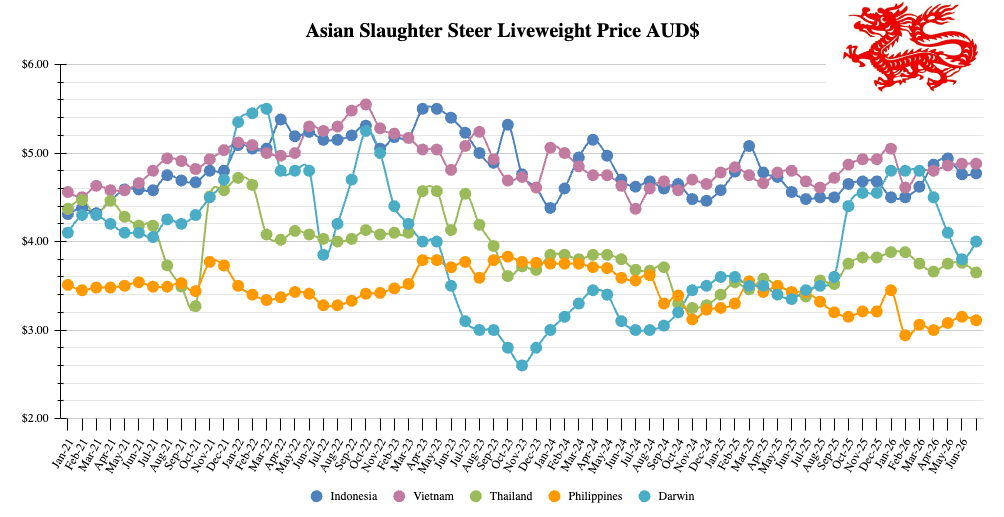

Regional Price Graph

Indonesia: Slaughter Steers $4.88 AUD per kg live weight (IDR 12,500 = $1 AUD)

Prices

Lampung slaughter steers are near IDR 61,000 per kg, the rupiah a touch firmer against the Australian dollar at around 12,500. Wet-market beef sits at Rp130,000 to Rp140,000 and buffalo above Rp90,000 as households trade down. The government watches all of it, which is the root of the feeder trade’s problem.

El Nino lands on an already-squeezed feedlot

Regular readers know the reference-price squeeze well enough, and nothing this month has eased it. The pressure worth flagging is on the other side of the ledger. Feed is the swing cost in any finishing operation, and Indonesian rations lean on cassava and locally grown forage, the crops a dry year puts at risk. With the finished price fixed and feed the one input still free to move, a dry season pushes the cost of gain the wrong way, and a thin margin quickly becomes none.

Feed banks: the buffer Australia has never had to build

Feed banks, or bank pakan, literally feed barns, are a government-run forage reserve scheme, and there is nothing like it here. You make and store feed while it is abundant so there is a buffer for when the dry season strips the pasture. In practice that means silage, fresh forage fermented in sealed storage, and hay, held at the farmer-group level for the lean months. This year’s government-led push is to activate 843 of these banks across all 34 provinces ahead of El Nino, alongside more drought-tolerant forage such as indigofera, gamal and lamtoro and high-protein elephant grasses.

Why it exists tells you a lot about the sector. More than 90 per cent of the herd sits with smallholders who cut and carry grass and crop residues day to day, with almost no stored-feed culture. In a normal year that works. In a drought the fodder collapses, animals lose condition, and you get distress selling and, at worst, stock losses, as in 2015-16 and 2023-24. Feed banks try to break that cycle by industrialising, at village scale, conserving feed for later.

Local Indonesian cattle are often fed grasses foraged from public land or the side of roads. These are not managed feed crops and often fail when conditions get tough.

Thailand: El Nino agriculture damage put at THB 62 billion

Krungthai COMPASS has put the coming El Nino’s cost to Thai agriculture at around THB62 billion, close to 0.31 per cent of GDP, into mid-2027, with the central dams already below the 30 per cent officials treat as critical and farm income tipped off about 8 per cent.

Thailand is the source of the cheap cattle that move, often informally, into Vietnam and undercut Australian animals there. A dry year that lifts Thai feed costs and thins the herd makes that competition dearer and scarcer, now with a weather driver behind the easing I flagged over the past year. I will watch to see whether it reopens Vietnam for us faster than any easing in the Darwin price.

Dry conditions in Thailand’s north has put pressure on crop yields.

Vietnam: Slaughter Steers $4.85 AUD per kg live weight (VND 18,700 = $1 AUD)

The number that matters in Vietnam this year is not the price, it is the flow, and there barely is one. On my read only a few thousand head of Australian cattle are left on feed in the whole country, if that. Price and the weaker dong did the damage, as I have covered, but the point this month is what happens when slow trade becomes no trade. What is different in 2026 to previous years is that the trade has effectively stopped for a sustained stretch.

When the flow stops, the approvals lapse

When Australian cattle stop arriving, butchers and traders do not wait. They source elsewhere, from local supply, Thai cattle, boxed beef, and the channels that moved Australian cattle wither. Those channels had already shrunk a long way, which makes this worse. The harder problem is the abattoir. Keeping a plant to ESCAS standard, audited and approved for Australian cattle, costs real money whether or not a beast comes through the gate. A processor carries that for a while on the promise of trade returning, but through a year with no flow the sums stop working, and plants drop off the list. It has to be rebuilt one approved abattoir at a time, which means if Australian cattle prices start to allow the trade to move again, rebuilding that abattoir throughput capacity could be a slow process.

Philippines: Slaughter Steers $3.50 AUD per kg live weight

The Philippines is where the demand side of an El Nino shows up most plainly. Analysts warn a strong event could lift reliance on imported meat, dairy and feed by 20 to 30 per cent, an extra PHP 40 to 55 billion, with cattle and carabao losses in the tens of billions of pesos as milk yields fall. Bukidnon cooperatives are already reporting milk-yield declines of 20 to 25 per cent. For us that widens the usual door for boxed beef, though Brazil will chase the same gap.

Manila places a bet on home-grown vaccines

Away from the weather, the Philippine development that caught my eye has nothing to do with drought. Manila is making a serious move on animal-disease vaccines. The Department of Agriculture has stood up a three-year, roughly PHP 140 million program with the Bureau of Animal Industry, the Philippine Carabao Center and a state university to develop African swine fever and foot-and-mouth vaccines at home, biosafety laboratory and all, and it expects its first commercial ASF vaccine, a live product developed in Vietnam by AVAC, in the third quarter. The ASF work could help a pork sector disease has battered for years, but the foot-and-mouth side matters more to us, since a neighbour building that capability on our doorstep is a biosecurity story worth watching, timelines aside.

Australia: Feeder Steers Darwin $4.00

At home the market is running at two speeds. Southern and eastern prices have recovered hard on autumn and winter rain, the young-cattle indicators back up, while Darwin feeder steers have held at around $4 per kg liveweight on Indonesian inquiry into July/August. Townsville, tellingly, has no live-export interest at all, priced out by local feedlots paying more than the boats can justify.

The trade has spent this year caught between an Australian live cattle cost base that will not fall far and an Indonesian ceiling that will not rise. A dry year in the region to our north does not loosen that vice. The one place it could break our way is the region’s demand for everything that is not a feeder steer, the second-grade cattle, buffalo, dairy and breeder cattle and the boxed beef into markets whose own production is faltering. The next few months will tell us whether the trade can lean into that while the feeder channel waits out the weather.

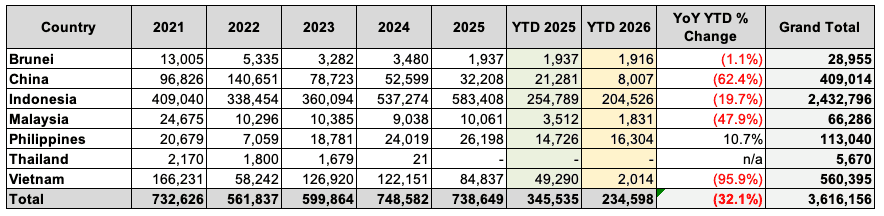

Year 2026 cattle exports up to end of April – comparison across SE Asean markets

Source: DAFF website

Note: 2026 data is year to date as at 30 June 2026; YTD 2025 covers the equivalent January to June 2025 period. YoY % change compares the two YTD columns. Malaysia includes Peninsular Malaysia, Sabah and Sarawak.

HAVE YOUR SAY