Richard Koch, Elders

Richard Koch is an economist working with Elders. His regional cattle markets wrap follows a weekly hook-up with Elders livestock managers across the country.

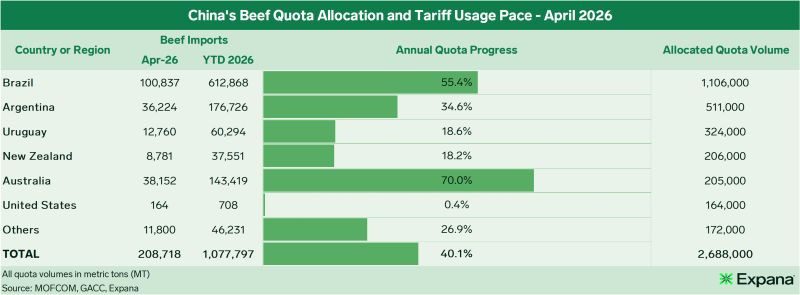

AT Monday’s Elders national livestock hookup one of the agents asked a question about what to expect from other suppliers once safeguard quota tariffs hit Australia/Brazilian suppliers in China and Korea.

China will formally announce that Australia has filled its quota any day now, while Brazil must be close to the 80pc figure at which point the Chinese Government will make an official announcement.

How will Argentina/Uruguay, NZ and the other nations that have only shipped around 30pc or 350,000 tonnes against their 1.2 million tonnes quota respond? Theoretically these countries could turn their attention to China, leaving opportunities for Australia and Brazil in other markets.

These are the latest available figures to April, with May statistics due to be updated on 20 June.

Firstly, the only viable option to replace Australian high quality chilled beef is the US, but most US plants have not had their Chinese export licenses renewed, and they have only shipped a fraction again their 164,000t quota. The Chinese Government could reinstate these processors which would create a viable alternative, but that would only further stretch tight US domestic supplies. Expect Chinese importers to push for this at some stage.

China’s CIFER renewed long-awaited export approvals for US beef facilities on May 17. The move covered 425 facilities in total, including 77 newly approved plants, while 38 facilities remained under suspension. A White House statement later said China will coordinate with US regulators to remove all remaining suspensions on US beef facilities.

There is a wider array of options to replace some Brazilian product in China. However, NZ won’t have much excess beef until its processing industry ramps up again after winter in Q4 2026.

Argentina/Uruguay could possibly increase export volumes, but they would need an incentive to redirect beef from current markets. With Chinese imports front-loaded and plenty of imported product frozen down in store across China, I’m not getting the feeling the Chinese market is screaming out for beef right now.

In a world without constraints and, given the incentive, these countries would move to fill their unused Chinese quota and could backfill their domestic needs with Brazilian product.

But it is not like turning a tap on and off. They would need to find customers, set-up distribution, supply beef of the right customer specifications. Do they have enough Chinese accredited/licensed plants? Is it worth shunning existing customers for a sugar hit into China, knowing Brazil will be back in after a few months?

Brazilian beef would flood secondary markets such as Philippines/Indonesia and backfill any gaps left in South America if Argentina/Uruguay chose to focus exports on China.

In Korea, with most of South America locked out due to FMD restrictions, US/Canada to step in, but its beef is more expensive than the equivalent Australian product and they may be best to keep their beef in North America, given they are already operating at a deficit that requires imports.

I asked Junie Lin who covers Asian pacific beef markets for Expana about the possibility that Korea may not enforce its TRQ, she replied “I’ve been asking packers and importers but there are no signs of waiver like they did in COVID.”

“Most markets players we spoke to have given zero indication of a repeated waiver for 2026, like they did in 2022 as a post-COVID019 economic stimulus recovery measure,” she said.

Clearly there are just as many questions about what might happen as answers.

NQ rates start to flatten as increase supplies comes to market

NQ Elders agents report physical markets across the region have come under a bit of pressure in the last couple of weeks, as supply increases seasonally. The heaviest and best cattle are mostly equal, but the next step down in quality, came under a little bit of pressure, back 10 or 15c/kg.

The other change in the northern market dynamic is the reappearance of the HGP discount at around 30c. When the market was charging, there was no discount. They were just drafting them and delivering them a different line.

The live export market has picked up a little bit back up to a $4/kg for a Brahman steer Darwin, with the Indonesian Rupiah coming back under 18,000Rp to $US over late last week at 17,700Rp/$US.

There is good inquiry going forward for late June and into July, but still no live export interest out of Townsville given strength of local feedlot pricing which puts cattle above Darwin rates (normally Townsville feeder steers trade at a discount to Darwin due to higher freight to Indonesia).

CQ season hays off, but prices anything but

The season across CQ is starting to hay off and they’re looking for rain, but there is still plenty of feed about.

Southern feedlots were very active on the feeder cattle buying at $5.25/kg delivered Moura & Blackhall which makes it $5.40-$5.45/kg Downs for a flatback feeder. With the strength in the feeder steer market, suitable heifers are starting to narrow the gap to steers to below 50c/kg.

With feeder and slaughter markets strong, weaners are making closer to $6/kg.

Processors chase grassfed steers that aren’t there in Northern NSW

There’s been a lot of inquiry for grassfed yearling trade steers across our network in northern NSW and prices are now north of $10/kg dw which is no surprise as Northern New South Wales normally supplies a lot of those cattle at this time of year. These cattle were sold out of the area a few months back due to seasonal conditions.

If you can find one, an Angus feeder is at $6/kg or thereabouts, for the equivalent 400-500kg black heifer, you are looking at $5.40 to $5.50/kg.

We are hearing some stronger 100-day quotes for October, which now seem to be tracking higher with the feeder market. We’ve had a good seasonal turnaround across a fair percentage of the state, but it’ll take time before we see any numbers. Southern supplies will start to kick in around August/September.

Source: NLRS

This chart shows the narrowing in the spread between feeder steer and heifers national saleyard indicator values in c/kg liveweight

Money draws more lightweight cattle to market across the south

In Victoria, more rain from 10-60mm, depending on what part of the state you’re in. Some water has started to run into dams, but it needs to keep raining.

Our agents report that they have been getting one frost a week for the last three or four weeks, but this Monday’s frost was the heaviest so far. It is getting to that time of year, where the frost will counteract the rain.

The cattle job’s flying with little black restocker steers making nearly $7/kg, somewhere in Gippsland.

Feeders are $5.50 to $5.60/kg but they are few and far between.

There are some lightweight calves appearing just purely chasing the money. There were 5000 cattle booked for the store sale at Mortlake today and another 5000 at Ballarat tomorrow. Most of these cattle don’t need to be sold but the money is drawing a few out. Once we get through the next few weeks it’s going to get very, very quiet.

Prices start to tease cattle to market in SA

SA had more rain over the weekend across most of the south of the state, and there is a fair bit in the forecast over the next week. Adelaide is meant to get 75mm of rain over the course of the next four or five days.

There was an 800 head store cattle sale in Dublin Monday that included a large draft of cattle from pastoral areas west of Port Augusta that got good support from the SA network. A bit of a mixture of bullocks, bully calves, heifers and steers.

Sales numbers went from 200 to 400 to 800 head over a few days as prices kept rising and sold to strong interest. Restocker steers and heifers $4.80-6.20/kg, restocker heifers $4.40-5.40/kg. Feeders $5-5.70/kg for steers and $4.80-5.50 for feeder heifers. $4/kg for a slaughter bullock and $3.80/kg for a kill heifer.

The season is as good as we’ve seen for a long time. Everyone’s up and about.

Solid rain front sweeps through WA and pushes up store prices

Good rain north of Perth and right through to pastoral areas from a strong cold front that came through last week and covered almost all agricultural regions across the state.

On the slaughter cattle pricing front, no changes with cows $7.40/kg dw over the hook or $3.60 to $3.80/kg in the yards. Heavy bulls, $3.70/kg in the yards, $7.20/kg dw direct to abattoir.

Yearling steers to the paddock from 280-380kgs solid at $5.50/kg, topping out just short of $6. Heavy steers +400kg are averaging out at $5.20/kg. Heifers 280 to 400kgs also solid at $5/kg.

Everyone’s chasing cattle and the volumes are light seasonally and prices are showing no signs of slowing down.

Rain in Tassie starts to replenish irrigation dams

Good rain across virtually all of Tassie last week, anywhere from 30-60mm and expecting more of the same this week, which augurs well particularly for the southern part of the east coast where they need that run off to start filling irrigation dams.

It’s starting to look very promising season wise.

Cattle prices holding well, over the hooks around $8.70/kg dw for program yearlings and $7.20 to $7.30/kg for cows, rates are starting to firm up as the seasonal cull finishes up.

The store cattle market is very solid. Heavy steers +400kg anywhere from $4.90 to $5.30/kg for black steers. Medium weights 300-400kg, $5.50 to $5.80/kg and light weights under 300kg up to about $6/kg on the better end.

Heifers have been the real big improvers over the last couple of weeks. Can’t get a heifer for under $4.80/kg with most around $5.10 to $5.20/kg on the heavy end.

HAVE YOUR SAY