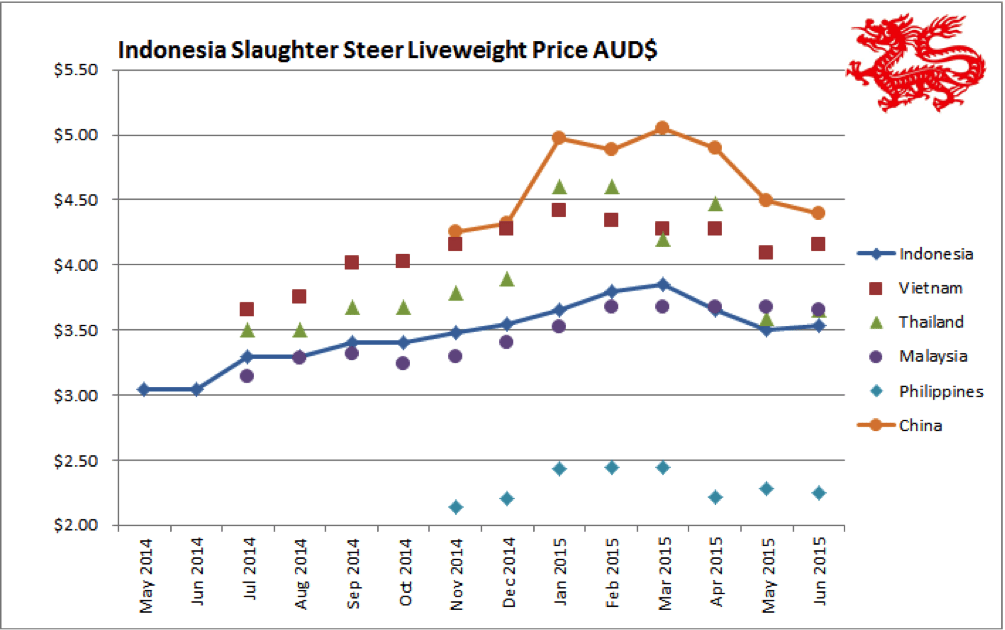

Indonesia: Slaughter Steers AUD $3.53 / kg live weight (Rp10,200 = $1AUD)

Ramadan commenced on the 17th June and so far there has been only limited additional demand and no significant movement in prices for the month of June except for a modest increase in supermarket prices around Jakarta.

The AUD price above has only moved upwards slightly due to a little weakening of the Rupiah cross rate. Large numbers of feeder cattle continue to be imported throughout June but this has now come to a sudden halt due the inability of the Indonesian Trade Ministry to issue the new Q3 permits.

I am advised that there are 7 vessels at anchor in Darwin harbour unable to load because they don’t have a permit to ship in the July-September Quarter.

If the permits are released today (Tuesday 7th July), cattle will not be able to load until the 8th due to the documentary trail but some ships will still have to wait even longer as there are not enough trucks or wharf space in Darwin to load 7 ships at once.

The Indonesian government unfortunately does not appear to understand that this delay will cost their consumers in the medium term. The delay to date is at least one week which means that shipping companies can only earn income for their ships for 51 weeks of the year instead of 52. As this seems to be a reasonably common event in Indonesia, shipping companies will have to factor this issue into their freight charges so everyone pays higher freight in the medium to long term and eventually this will be passed on to the consumer. The days of passing any extra costs back to the producer are now gone. After 40 long years where all additional costs were passed back to the producer, the new status of global supply and demand means that the customer is the one who will have to pay.

The peak consumption period at the end of Ramadan/beginning of Lebaran will be very instructive in terms of the capacity of the local herd to contribute to domestic slaughter cattle requirements. Australian cattle are only available in Sumatera and West Java so Central and East Java (about 60 million people) will be relying on local cattle and buffalo for their fresh beef needs. The price for local cattle in Central Java today is :-

- Rp41,000 per kg live weight (AUD$4.02) for Sumba Ongole bulls (bos indicus imported from Sumba Island)

- Rp43,500 (AUD$4.26) for Bali cattle Bulls (from Java and Bali)

- Rp42,000 (AUD$4.12) for locally bred ongole bulls (bos indicus) from Central and East Java

These prices will rise as demand strengthens in the next two weeks. If the domestic cattle herd is as big as the government hopes it is then the increase might be around 20+% up until Lebaran. If the local herd has shrunk to where most industry observers think it has then prices could spike by 40% or more. We will soon find out.

Prices remain high in North Sumatera as the inflow of feeders has not been as great as around Jakarta. Rates are still averaging around Rp38,000 per kg live.

As the Jakarta price is the main game in Indonesia I will continue to use Rp36,000 as the indicator price for June.

The Northern Territory Minister of Agriculture visited East Kalimantan 2 weeks ago and met with the Deputy Governor of the province to discuss the forthcoming export of breeding cattle from Darwin to Balikpapan. The province of East Kalimantan has an ambitious target for establishing breeder cattle grazing under palm oil trees and there are simply not enough local cows to expand the program at a rate which will meet their objectives. Northern Australia is the next stop for large numbers of breeders with the NT government getting involved at an early stage to ensure the outcome from the first shipment that will encourage many more.

Northern Territory Minister of Agriculture Hon. Willem Westra van Holthe (white shirt) and NT Indonesian Consul Pak Andre Siregar(red and blue bull rider batik rodeo shirt) having a photo opportunity with the lead Bali cow of a group of cattle grazing under oil palm trees in East Kalimantan.

Vietnam: Slaughter Steers AUD $4.16 / kg (VND16,700 to $1AUD)

Internal prices were generally steady across Vietnam but pressures are building from both internal and external sources.

The massive HAGL feedlot cattle numbers continue to overhang the market while those cattle which would normally be exported from Thailand to China via the Mekong are now being redirected to the east to Vietnam via Laos and Cambodia.

At the same time, imported feeders and slaughter cattle from Australia are increasing in price.

On top of all this, the regional rainy season has allowed planting to be completed in Cambodia so surplus draft cattle will soon be coming onto the market for export to Vietnam.

It seems like there is a crunch coming and there is probably not long to wait. Assuming China continues to close off the Myanmar border then the surplus slaughter cattle in Thailand will take only a few weeks to “flood” the supply lines into both north and south Vietnam. This bulge in supply is only likely to be short lived however, say 3-6 months if the Myanmar/Thai border at Mae Sot remains closed. Burmese imports are the primary source of local supply for the whole region and if imports from this source do not re-open then the glut in Thailand will disappear and the previous situation of inadequate supplies across the region will return.

Vietnamese processors report a significant reduction in the price of hides and offals resulting from reduced Chinese demand. A similar fall in demand for hides is also being reported in Indonesia.

CCTV installations for enhanced traceability continue across the Vietnamese supply chains and will soon be complete.

Thailand: Slaughter Steers AUD $3.65 / kg (Baht 26.0 to $1AUD)

Prices remain weak in Thailand as a result of the ongoing closure of Burmese imports via Mae Sot and exports via the Mekong to China. The excess supply that has resulted is now being redirected to north Vietnam via Laos and south Vietnam via Cambodia to Ho Chi Minh City. Retail prices however remain generally unchanged.

The best guess is that the Myanmar border closure at Mae Sot is more likely to be short term while the Chinese import halt in the north looks much more like a long-term issue. If Mae Sot reopens first then the oversupply in Thailand will continue and cheaper local live cattle should be the result across the entire SE Asian region. With all this uncertainty, the short-term prospects for further live exports from Australia to Thailand appear bleak.

Malaysia: Slaughter Steers AUD $3.65 per / kg (RM2.88 to $1 AUD)

Once again, little change in the Malaysian market. Prices are stable while the Ringgit has weakened a little following concerns about the Malaysian economy.

Philippines: Slaughter Cattle AUD $2.25 / kg (mainly cull cows & bulls)

All steady for the Philippines with minimal changes to all prices. Once again, my agent advises – no natural disasters, seasonal or political calamities – so that means good news for Filipino farmers and consumers.

For this month I have used the exchange rate of AUD$1 to Peso 34.7

China: Slaughter Cattle AUD $4.40 / kg (RMB 4.77 = AUD$1)

Prices continue to remain weak in the Beijing and Shanghai areas of China. Live cattle prices reduced again by RMB 1 in Beijing although retail prices are relatively steady. With so many issues influencing the massive market in China it is exceptionally difficult to get an accurate feel for the short-term movements in the trade. Some current issues include :-

- Chinese government crack down on Grey Route, smuggled beef. This trade involves more than 1 million tons per year.

- Chinese closure of the northern Myanmar border to live cattle ex Thailand causing severe shortages in the South West Yunnan province.

- Reports of falling prices for offals and hides in China

- China is in the process of reopening legal access to Brazilian and USA beef following closures for disease reasons.

- Imminent opening of the trade for Australian live slaughter cattle

- Reports of some Chinese domestic beef feedlots closing due to poor profitability.

Given all these conflicting influences, the only thing for certain is that the long term for China involves demand which is greater than domestic supply so import demand should remain strong. The details of timing and prices represent impossible guesswork but Australia remains the world’s best placed supplier to capture a healthy share of the cake with prices at the higher end due to our top quality live and box beef products.

USA: Feeder Cattle AUD$8.01 (AUD$0.77)

Yes, it’s true. This is not a tying error. Today’s feeder cattle price in the USA is $8 Aussie!

Anyone can check this by looking up these prices on the internet. Look up the US “5 area average” which is in indicator price like the Australian EYCI (Eastern Young Cattle Indicator) from 5 important cattle fattening areas of the USA – Texas/Oklahoma/New Mexico, Kansas, Nebraska, Colorado and Iowa/Minnesota.

Recent prices reports show that the fat steer indicator price is US$150.11 cents per pound live which converts to US$3.30 per kg live or using an exchange rate of 0.77 for the AUD a fat steer (about 600kg) price of AUD$4.30 per kg live.

The feeder cattle indicator price is US$2.80 per pound or US$6.17 per kg which converts to a spectacular AUD$8.01 per kg for a feeder steer weighing an average of about 360 kg live weight.

The feeder price is so much greater than the slaughter price for two main reasons. Firstly the supply of feeders has collapsed as the herd numbers are down to record lows and feeder heifers are being withdrawn from the market as producers commence herd rebuilding. The second reason is that feeding costs in the US are dramatically lower than in Australia with ration prices about US$190 per ton or AUD$246.

The loss that a feedlotter will make using these inputs is offset (hopefully) through complex risk management strategies including locking in prices for feeders, fat cattle and grain via futures trades or options on futures trades. Or take your chances and bet the farm that everything will work out OK. Some lot feeders obviously get better prices than the market indicator so this no doubt helps too.

The price of breeders has increased again following the breaking of the drought with average females bringing US$2,200 per head and good quality bringing US$3,000 per head or AUD$3,896 for a handy breeding cow.

This trend in higher prices is predicted to continue into 2016 with the cow calf producer finally getting the lion’s share of the supply chain margin. The changing of the margin share has also provided a new option for producers where some are beginning to retain ownership of the animal until slaughter, a choice that wasn’t available or attractive during the old days of oversupply. It just gets better and better and the best part it that the Australian cattle market is subject to the same fundamentals and will follow a similar trajectory once the drought has broken.

Given the massive price differential between Australian and US feeders, it appears that the business case for opening the live feeder cattle trade from Australia to the USA is getting stronger by the minute. It must be getting harder for the US cattle producer lobby to complain about unfair competition from cheap imports when they are getting US$6 per kg for their feeders and 320 million American consumers are paying historically high prices for their retail beef. Sea freight costs for live cattle from Australia to the US using the larger fast ships are roughly double those to Asia with a 60 day round trip time for a delivery into the Texas coast via the Panama canal. Freight for a 360 kg feeder from the east coast of Australia to the USA is approximately US$350 so if the feeder costs AUD$3.50 per kg live in Australia then the total landed costs in the Texas port will be in the order of US$1,320++ or US$3.70 per kg. Looks like there is room for a margin between this price and the current US domestic feeder rate of US$6 per kg.

My daughter was in New York last week and sent this photo from an upmarket downtown butcher shop. This retail price range of US$14 and $35 per lb converts to AUD$40 to AUD$100 per kg. Each price ticket includes the farm of origin.

Dr Ross Ainsworth’s monthly South East Asian reports are first published exclusively on Beef Central. To view more of Dr Ross Ainsworth’s previous Beef Central articles click here. To visit his personal South East Asia report blog site, click here.

Market price table for June 2015

(All prices converted to AUD)

These figures are converted to AUD$ from their respective currencies which are changing every day so the actual prices here are corrupted slightly by constant foreign exchange fluctuations. The AUD$ figures presented below should be regarded as reliable trends rather than exact individual prices. Where possible the meat cut used for pricing in the wet and supermarket is Knuckle/Round.

| Location | Date | Wet MarketAUD$/kg | Super market$/kg | Broiler chicken$/kg | Live SteerSlaughter WtAUD$/kg |

| Jakarta | Jan 2015 | 11.00 | NA | 3.50 | 3.60 |

| Feb 2015 | 11.00 | 12.75 | 3.30 | 3.70 | |

| March 2015 | 10.50 | 12.00 | 3.00 | 3.85 | |

| April 2015 | 11.00 | 15.00 | 3.60 | 3.65 | |

| May 2015 | 10.68 | 12.33 | 2.52 | 3.50 | |

| June 2015 | 10.78 | 14.60 | 2.94 | 3.53 | |

| Medan | Jan 2015 | 3.75 | |||

| Feb 2015 | 11.75 | 11.75 | 1.70 | 3.95 | |

| March 2015 | 10.00 | 12.00 | 1.40 | 3.90 | |

| April 2015 | 9.70 | 11.50 | 1.70 | 4.00 | |

| May 2015 | 9.32 | 9.90 | 2.14 | 3.69 | |

| June 2015 | 9.41 | 10.09 | 2.35 | 3.73 | |

| Philippines | Feb 2015 | 7.03 | 6.38 | 3.56 | 2.45 |

| March 2015 | 6.25 | 6.45 | 3.54 | 2.44 | |

| April 2015 | 5.80 | 6.02 | 3.47 | 2.22 | |

| May 2015 | 5.86 | 6.28 | 3.51 | 2.28 | |

| June 2015 | 5.88 | 6.40 | 3.17 | 2.25 | |

| Thailand | Jan 2015 | 9.60 | 11.20 | 2.80 | 4.60 |

| Feb 2015 | 9.60 | 11.20 | 2.80 | 4.60 | |

| March 2015 | 9.20 | 11.20 | 2.80 | 4.20 | |

| April 2015 | 9.88 | 11.07 | 2.77 | 4.47 | |

| May 2015 | 9.05 | 10.57 | 2.64 | 3.68 | |

| June 2015 | 8.85 | 10.76 | 2.69 | 3.65 | |

| Malaysia | Jan 2015 | 10.10 | 10.25 | 2.60 | 3.52 |

| Feb 2015 | 9.86 | 10.21 | 2.46 | 3.68 | |

| March 2015 | 9.92 | 10.28 | 2.48 | 3.68 | |

| April 2015 | 9.93 | 10.28 | 2.48 | 3.68 | |

| May 2015 | 9.82 | 10.18 | 2.46 | 3.68 | |

| June 2015 | 9.72 | 10.42 | 2.36 | 3.65 | |

| Vietnam | |||||

| HCM | Jan 2015 | 15.75 | 16.96 | 9.69 | 4.36 |

| HCM | Feb 2015 | 15.66 | 16.87 | 7.83 | 4.34 |

| HCM | March 2015 | 15.66 | 16.97 | 7.83 | 4.28 |

| HGM | April 2015 | 14.97 | 16.77 | 7.78 | 4.28 |

| HCM | May 2015 | 14.70 | 16.47 | 7.65 | 4.09 |

| HMC | June 2015 | 14.97 | 16.77 | 7.78 | 4.16 |

| China | |||||

| Beijing | Jan 2015 | 14.10 | 19.08 | 4.15 | 4.98 |

| Feb 2015 | 16.32 | 16.32 | 4.08 | 4.89 | |

| March 2015 | 14.73 | 19.28 | 4.21 | 5.05 | |

| April 2015 | 14.28 | 18.36 | 4.08 | 4.90 | |

| May 2015 | 14.29 | 18.69 | 4.08 | 4.49 | |

| June 2015 | 14.66 | 19.20 | 4.19 | 4.40 | |

| Shanghai | Jan 2015 | 18.67 | 18.67 | 4.98 | 3.52 |

| Feb 2015 | 18.36 | 17.55 | 4.08 | 3.47 | |

| March 2015 | 18.94 | 18.02 | 5.47 | 4.00 | |

| April 2015 | 18.36 | 20.00 | 5.31 | 3.98 | |

| May 2015 | 18.36 | 20.00 | 5.31 | 3.37 | |

| June 2015 | 18.87 | 20.55 | 5.45 | 3.98 |

HAVE YOUR SAY