Imported frozen Australian lean grinding beef is currently trading as much as 44c/kg (20c/lb) less than equivalent US domestically-produced fresh 90CL beef.

Imported frozen Australian lean grinding beef is currently trading as much as 44c/kg (20c/lb) less than equivalent US domestically-produced fresh 90CL beef.

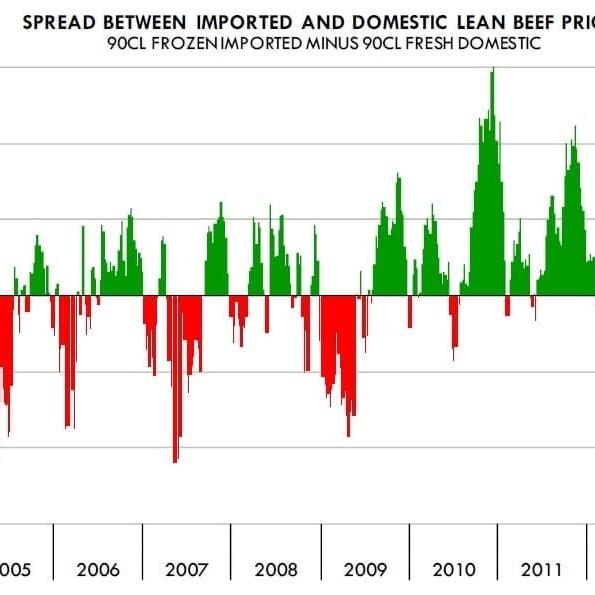

As can be seen in the chart at left, historically it is not that unusual for domestic beef to trade at a premium over imported product. However, this was not the case the last two years given a significant shortage of imported beef. This year, however, even as imported beef is tight, domestic product is trading at a big premium.

Beef Central first looked at the issue of imported versus US domestic price differentials in an article “Retail segment driving US/Australian 90CL price disparity” on June 12.

US analyst Len Steiner, from Steiner Consulting, suggests the current price spread is due to a range of factors.

One of these is large US supermarket retailers that are committed to using domestic-only beef, which have also removed Lean Finely Textured Beef from their ground beef formations. These companies are now having to pay substantial premiums to secure supplies of lean domestic 90CL product, Mr Steiner said.

Market participants indicated that even as demand for imported grinding beef is limited, demand for US domestic beef remains quite robust.

“There are a number of reasons why US retailers do not use more imported beef,” Mr Steiner said.

“Most do not want to use frozen imported for product going into the retail case because of yield issues. Also, for frozen patties, they still have to contend with Country of origin Labelling (CooL) regulations and the additional burden of tracking and labelling product correctly,” he said.

Other factors included:

- the dramatic decline in price of domestic US fatty beef trim – the principal raw material used in the manufacture of Lean Finely Textured Beef – which allowed end-users to pay an even bigger premium for domestic fresh lean product to be blended to make a typical 75CL or 76CL pattie or meat block.

- Foodservice operators limiting their grinding beef purchases and focusing more of their attention on other food options, including salads and chicken, which have higher margins.

“Normally the spread between domestic and imported beef tightens in the second half of the year,” Mr Steiner said.

“In the past, this used to be because supply of imported beef would decline, partly due to lower New Zealand kills. But if we are correct and the spread is more due to the effects of LFTB and CooL in the US, then we could continue to see domestic product trade at a premium to imported beef for the foreseeable future,” he said.

HAVE YOUR SAY