HEIGHTENED uncertainty about the supply outlook for lean grinding beef out of Australia over coming months is contributing to imported beef prices in the US described as ‘very firm’ last week.

The 90CL imported grinding beef indicator (see Beef Central home page graph) was quoted last week at A649c/kg, 46c/kg or 8pc better than this time last year. In US currency terms, last week’s price of US221c/lb was US19c higher than year-earlier figures. Normal seasonal decline in cow slaughter in New Zealand is another contributing factor.

Current prices of imported 90CL product in the US are up 5pc from March levels, bucking the trend normally seen in June. More on this topic below.

Current prices of imported 90CL product in the US are up 5pc from March levels, bucking the trend normally seen in June. More on this topic below.

However current US end-user demand appears to have shifted somewhat, with increased interest for 90CL and 85CL product over leaner bull meat.

Lower prices for domestic US fattier beef trimmings, lack of availability for these categories and a slight seasonal bump in bull meat supplies all contributed to the narrowing spread between lean and extra lean grinds, Steiner’s weekly report last week indicated.

“Market participants continue to point out the lack of offerings from Australia as packers there appear to be quite well-sold for the next 7:45 days, and there is heightened uncertainty about the supply outlook in August and September,” Steiner’s latest report said.

Those nominated months largely reflect slaughter in Australia July and August – regularly discussed in Beef Central’s weekly kill reports as being particularly difficult for procurement this year.

Lower prices for fed cattle in the US appeared to have had little impact on the current market for manufacturing beef. Demand in the US market was described as mixed, with some market participants complaining about market conditions while others reported a continued good flow of orders.

Spot supplies remained particularly tight, and in the short-term this was supportive the market, last week’s report said.

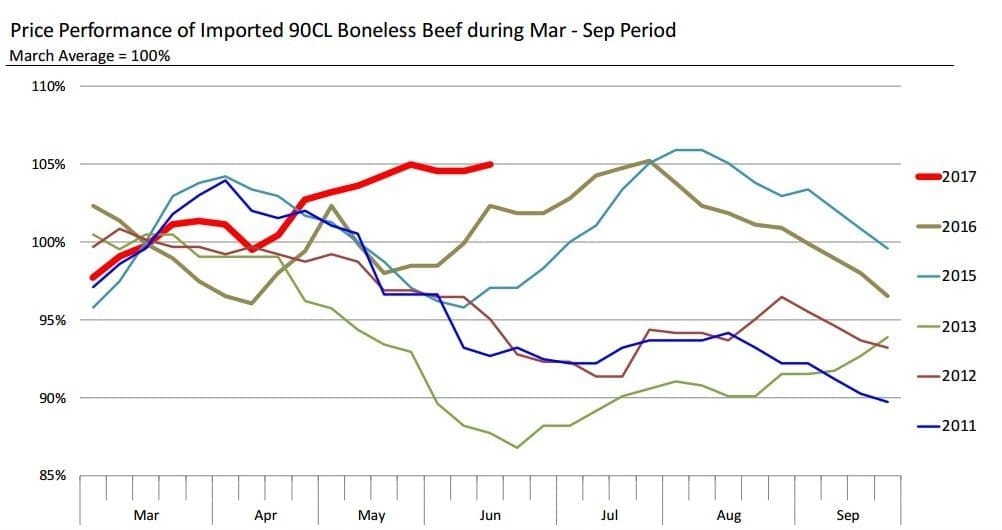

2017 goes against six year trend

Steiner’s chart published here (click on image for a larger view) shows the trend of imported beef prices for the spring and summer (northern hemisphere) months in the US for the past six years.

Because prices move around from one year to the next, prices were indexed in percentage movement terms, relative to March levels, rather than shown as absolute price levels. For example, prices in 2013 by June were down almost 14pc compared to the March average of that year, while in 2016 the three-month price decline was much smaller.

“The point of this chart is to show that generally June imported prices tend to be lower than March levels, which makes sense. After all, we see a surge in beef shipments from NZ during May while early (northern hemisphere) spring demand normally settles down,” Steiner said.

“This year, however, has been different, and we did not see much of a break in price, and currently the price of imported beef is about 5pc higher than the March average.”

In most years prices for imported beef continue to gain in July and August, largely a supply effect due to the seasonal decline in slaughter in NZ and Uruguay.

US food service demand concerns

There continues to be a lot of debate about business conditions in the food service sector (restaurants, hotels and the like) in the US, Steiner reported.

“While retailers have generally been more adept at adjusting prices in order to stimulate foot traffic, larger chain restaurants have struggled and the trend has been down. Foot traffic, one of the main metrics, has been trending lower since 2014 and it has been in contraction territory for the past 12 months.”

While all respondents in a survey indicated that traffic was lower in April 2017 compared to the same period a year ago, the situation was particularly concerning for fine-dining and the quick casual restaurant segment.

“Fine dining likely needs little explanation, it is the high end of the foodservice industry and has the largest checks,” Steiner said. “The decline is often blamed on the proliferation of entertainment options in the US and the propensity of younger people to forego splurging on fancy dinners and rather opt for less formal dining out experiences.”

‘Quick casual’ is part of the broader quick service restaurant category (QSR), but is used to distinguish those businesses that are a bit more ‘upscale’ than the traditional fast food chains.

An example in Australia would be the successful Grill’d premium burger chain which now has 124 stores operating across Australia.

“Quick Casual was a high-flying concept in the US a few years ago, but it has been challenged in recent years by the proliferation of independent restaurants that boast even fancier décor and high-quality ingredients,” Steiner said in its latest report. “Low interest rates likely have further added to the pressure, encouraging more entrepreneurs to jump into the fray.”

Fed cattle slaughter last week in the US was 500,000 head, the second largest weekly slaughter for the year and 3.4pc above year ago levels, Steiner reported.

“So far in Q2, weekly fed cattle slaughter has averaged 3.6pc under last year. However, much of this increase has been offset by lower fed carcase weights, which often have been 2.5- 3pc below year-ago levels. Weights are slowly recovering but they still remain about 2pc under last year.”

US Packers continue to aggressively process cattle thanks to some of the best margins in years, and this should continue to keep front-end supplies current. US fed cattle futures declined sharply last week on speculation that weaker demand and a huge basis (difference between forward cattle and current spot market) would incentivise both packers and feedlots to keep the marketing rate up.

Lower prices for fat beef trimmings also indicating that retail ground beef demand could slow down dramatically in July.

Source: Steiner Consulting

HAVE YOUR SAY