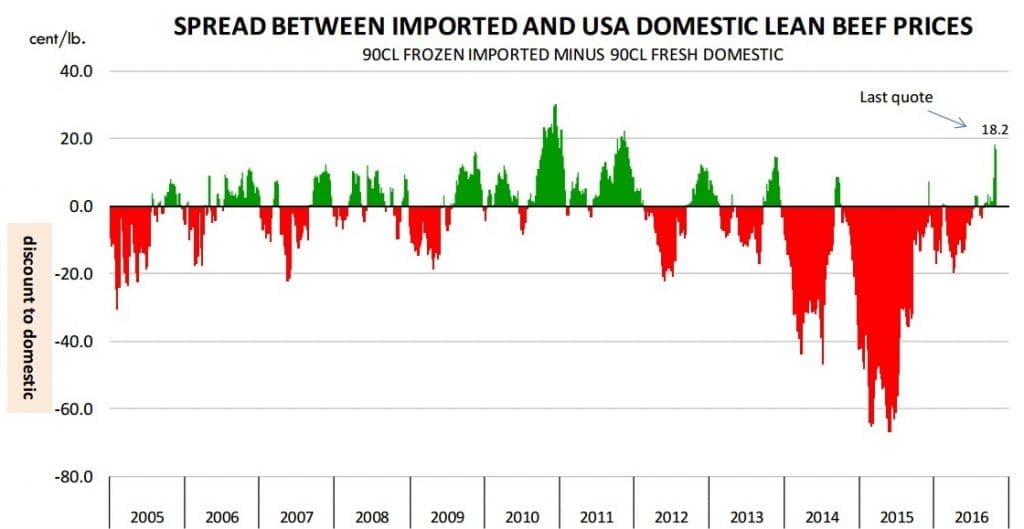

The price spread between imported and US domestic lean manufacturing beef has reached its highest level in five years, US analysts reported this week.

Prices on the US imported beef market have continued to push higher, driven by very tight overseas supplies on the spot market, stronger demand from importers trying to cover existing orders, and rising prices for domestic grinding beef.

Steiner Consulting quoted frozen imported 90CL boneless beef on Wednesday at US198-200c/lb, about 3c higher than the previous week and 10c higher than just three weeks ago. Compared to the same time last year, the indicator is down US28.3c/lb.

In A$ terms, the indicator is up A0.3c this week to 575.4¢/kg, compared with 603.7c this time last year, when the price was declining sharply from values above A750c/kg (see home page 90CL graph).

In its weekly imported beef market report, Steiner Consulting noted that while the turnaround in imported prices appeared quite sudden, the upwards movement was in line with trends seen in previous years when imported beef supplies have been tight.

In fact, the current spread between imported and domestic beef prices is a US16¢ premium for imported product – the highest level in the last five years (see graph below).

Source: Steiner Consulting

Worth noting also on the graph, is the huge discount (red area) that imported Australian lean manufacturing beef was selling for against domestic US product during 2014 and 15, driven both by heavy Australian manufacturing beef production, and a rampant A$ trading well above parity with the US$.

Stronger Australian dollar and low cow slaughter continue to limit Australia shipments to the US, with October volume down 47pc from a year ago (see yesterday’s October beef exports report). The majority of US imports from Australia are 90pc lean boneless beef for manufacturing purposes.

Supplies of 90CL boneless beef in the US come from two sources – imports and domestic cull cows. While imported beef volumes are down year-on-year, Steiner’s Daily Livestock Report suggests that US cull cow slaughter is 4.3pc higher for the year-to-date, compared to 2015.

While not all US cull cow beef is sold as 90CL boneless beef, the majority is, which has offset the decline in imported offerings.

“The current spread between imported and domestic beef, and similar premiums in the northern hemisphere autumn of 2012 and 2013 show the seasonal tendency for imported beef to trade at a premium in this period,” Steiner’s report this week said.

Imported beef supplies from Australia currently are even smaller than what they were in 2012 and 2013. Average monthly shipments of Australian beef to the US during Jul-Oct were 15,300t, about 20pc less than shipments during Jul-Oct 2013 and 14pc less than Jul-Oct 2012, the report said.

For all the increase in domestic US cow meat supplies during the last 18 months, availability of domestic grinding beef still is short of the levels seen in 2012 and 2013, Steiner said.

“Remember that at that time US cow-calf producers were liquidating the herd. Consider that average weekly cow slaughter in the US during Sep-Nov of 2012 was around 132,000 head per week and during the same period in 2013 the average weekly cow kill was 121,000 head per week.

“Based on cow slaughter rates through the end of October we estimate that this year US weekly cow slaughter during this same period will be around 112,000 head per week, 7.5pc lower than in 2013 and 15pc lower than in 2012.

The recent run-up in the price of imported beef reflected the tight supplies of lean grinding beef, especially in an environment in the US where there was an abundance of fat trimmings.

Normally, however, imported beef supplies improve in Q1 as more New Zealand and Uruguayan beef becomes available.

While some loads of Brazilian beef were shipped a month or so to confirm the opening of the US market to Brazilian product, more work needed to be done in areas like lotting (batch testing) system in Brazil, to expand the volume that is available.

“For now, Australia is opting to maximize shipments to Asian markets, with very limited supplies available to the US,” Steiner said.

US retail prices described as ‘sticky’

While ground beef prices at US retail have been declining in recent months, the pace of the decline has been significantly slower than what has been witnessed in the overall cattle markets in the US, Steiner said.

“Retailers so far have been resistant to lower prices more aggressively, as that directly impacts their overall revenue levels, especially when the price of other proteins is declining as well,” this week’s report said.

“The result is that during certain times of year the so called ‘sticky’ retail prices force prices at the wholesale level to decline even more than historical supply/price relationships would suggest. Fed steer prices in the US are now back to the levels we saw in 2010. Ground beef prices at retail, however, still are about 30pc higher than the 2010 average. As fed steer supplies in the US have increased, feedlots and packers have had to lower prices significantly in order to clear the market,” Steiner said.

Normally US consumer ground beef demand declines after Labor Day, in part because the start of the school year puts a strain on consumer finances but also because retailers present a more varied meat case after promoting ground beef aggressively during the grilling season.

“And with the price of ground beef at retail 30pc higher than what it was in 2010 there is no wonder that fat trim sales were weak, with prices dropping in the low 30s. Currently ground beef demand has shown some improvement, in part because hamburger patty manufacturers are building inventories for the holiday period. But once those orders are covered the worry/concern is that overall supplies will still be out of sync with what consumers are seeing at retail.”

“It will take time for retail prices to adjust. Once they do, however, we should see a less volatile market and also a market that better reflects the supply/demand fundamentals.”

Source: Steiner Consulting

HAVE YOUR SAY