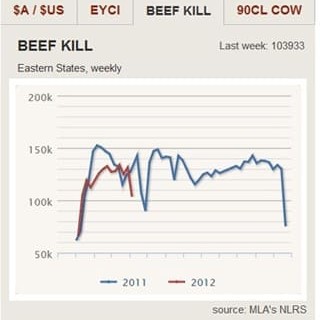

The start of a sequence of short killing weeks caused by public holidays took a predictable toll on nationwide processing activity last week, with the NLRS weekly tally for Eastern States diving 20 percent to 103,933 head.

The start of a sequence of short killing weeks caused by public holidays took a predictable toll on nationwide processing activity last week, with the NLRS weekly tally for Eastern States diving 20 percent to 103,933 head.

Numbers this week are unlikely to improve significantly due to Monday’s Easter holiday, and further disruptions lie ahead with Anzac Day (April 25) and Queensland’s Labour Day (May 7) also likely to exert an influence over throughput.

Last week’s kill was the second lowest of the year, exceeded only by the January 6 number of 66,556. As can be seen here on Beef Central’s weekly beef kill graph – published as part of our ‘Industry Snapshot’ indicators on the home-page – Easter fell a little later last year, but still had a huge impact on kill rates over a two-week cycle.

In fact the dive was heightened further last year by Easter Monday and Anzac Day falling on the same day, effectively leaving a rare three-day killing week.

Looking at last week’s kill performance, all states showed double-digit declines in numbers, despite easing in earlier rain-related access issues.

Queensland was the least affected, falling 16pc to 55,952 head.

There were some other contributing factors at play, including an extended 16-day closure at the dedicated grainfed Kilcoy Pastoral Co plant. At least two other large grainfed-oriented export plants, one in Queensland, the other in NSW, have scheduled longer-term reductions in kills of about 10-15 percent, Beef Central has learned, as businesses react to current ‘unsustainable’ losses in grainfed export beef.

Part of the reason why declines in Queensland kills were lower than other states last week may be the distinct change in seasonal movement in killable stock, combined with an attempt by processors to ‘bank’ some product earlier in the week, in anticipation of the loss of Easter Friday’s kill and upcoming short kills.

Cooler nights have now set-in in Queensland, and all processors are reporting cattle ‘on the move.’ Country from Dalby west to Bollon is showing signs of drying out, while country west of that region is still green. Slaughter cattle are generally in good to excellent condition and have maintained their finish despite the cooling weather and shorter days. Grown cattle weights generally have remained higher than previous years, with the excellent grazing conditions enabling producers to put extra weight into their cattle.

A significant development this week is that some SEQ exporter contacts are reporting kill access dates starting to extend outwards, as the flood of cattle starts. One contact is heavily booked, now only accepting cattle space for the week starting April 30.

NLRS reported Queensland saleyard cattle supply was 24pc higher overall last week, after Roma and Mareeba increased numbers after having rain affected yardings the previous week. NSW yardings fell 7pc, while Victoria’s were 16pc lower. SA supplies fell 20pc and numbers were back slightly in WA.

Grid prices ease again

Grid prices in Southeast Queensland last week produced another correction, declining a further 5-10c/kg in many categories as supply/demand factors other than rain take hold.

Most southern Queensland export plants this morning are offering 330c/kg for four-tooth Jap ox; 335c for milk and two-tooth; 325c six-tooth; 320c full-mouth; and 305-310c/kg for best cow. EU-eligible grassfed steers were generally quoted unchanged at 360c, MSA steer 350c.

Southern states record big corrections

Southern states showed even bigger kill declines last week due to Easter.

Numbers in NSW were back 25pc to 25,685 head, while Victoria was down 27pc to 13,885.

South Australia recorded a 32pc decline to 4869, while Tasmania eased 20pc to 3543.

Southern processors say slaughter numbers, particularly in Victoria/SA, are now getting hard to find, as the normal seasonal turnoff reaches its end. Expect to see more southern Australian plants scheduling fewer shifts, fewer cattle or dropped days in the near future.

Overseas markets

In international market developments, the US imported grinding beef market came back quite a bit last week, from earlier near-record highs. Trade in 90CL cow was quoted at A413c/kg on Friday.

Local interpretation of that is that it is in direct response to last week’s financial collapse of AFA Foods, one of the largest grinders in the US. It may also be due to general US consumer reaction to recent adverse publicity about Lean Finely Textured Beef, unfairly branded ‘pink slime’ in US media and social media channels.

The feeling is that US consumers may be avoiding hamburgers, generally, as a response.

Other market players felt it was as much a sign of uncertainty and confusion among grinders and importers, over where things might trend in coming weeks over the wash-out over LFTB.

This attitude might not last too long, one contact said.

In Japan, Agriculture & Livestock Industries Corporation data shows the nation’s imported beef inventory reached 76,000 tonnes at the end of February, the first time the inventory has fallen below 80,000t in four months.

ALIC expects it to fall further to around 70,000t in March and April due to the supply-demand situation, and a 40pc decrease in inventory that has not passed through customs.

HAVE YOUR SAY