A LOW-POINT in the current cattle price cycle around October next year is indicated in an independent analysis of price trends released last week.

Meat and livestock analyst Simon Quilty drew on previous Australian cattle price cycles, previous US live cattle cycles and international cattle prices as part of his assessment.

Two of the three pointed to the likelihood of a low-point in the cattle price cycle about October next year.

The fact that two methods point to a similar end date of October next year for the low in the cattle market is an interesting potential point of reference.

In recent discussion with producers, Mr Quilty has talked about a ‘soft’ landing and a ‘hard’ landing for prices, representing the potential influence of drought and/or stronger than expected global demand.

No drought in 2018 and strong global beef demand could see a soft landing in young cattle prices in a range from 460-520c/kg carcase weight, while drought and weaker global demand could see a ‘hard’ landing a range from 400-460c/kg, he said. By comparison the EYCI on Friday was 566.75c/kg.

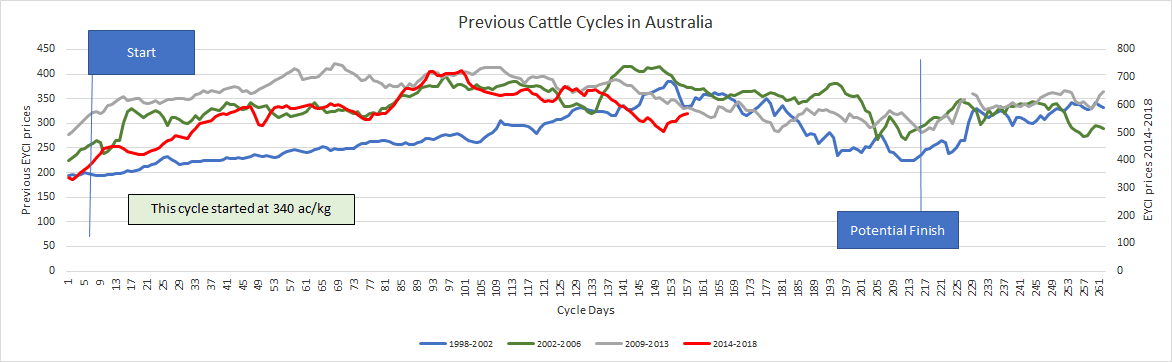

Previous Australian cattle price cycles

Click on image for a larger view

In comparisons with previous Australian cattle price cycles, the graph above shows where the current cycle sits in comparison with the other previous cycles, Mr Quilty said.

They cover the 1998-2002, 2002-06 and 2009-15 periods.

“The recent rain along the eastern seaboard, in particular for northern NSW and QLD, is likely to put the ‘cycle back on track’ for the bottom of the cycle next October,” he said.

“Should dry conditions prevail, however then the cycle could bottom-out 4-6 months earlier.”

In previous cycles, lifts in pricing like that currently being seen have not been uncommon for short periods but the eventual downward movement always eventually occurred in the past, the graph shows.

Mr Quilty said the duration of previous cycles range from 46-48 months, and October next year would be a 47-month duration in the current cycle.

“The price lows of previous cycles from the respective highs were -42pc, -36pc and -33pc which would equate to in this current cycle lows of 420.5c/kg , 464c and 485.75c (the high being 725c/kg last October).

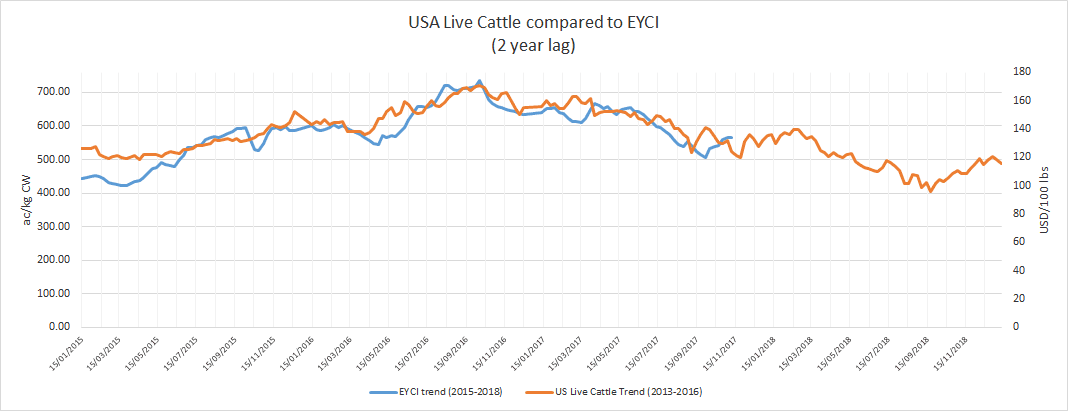

Comparing previous US live cattle cycles (2 year lag) with EYCI

Click on image for a larger view

The graph published above suggests the current rebound in Australian cattle prices was very similar to what happened in the US two years ago, Mr Quilty said.

“Should this remain true, it would imply a short-term lift in EYCI to about 580-600c/kg by next March (or earlier), before the continued downward trend to around October next year, which would translate to a low in the EYCI of 407c/kg,” he said.

“This is not a forecast but a trend that has remained stubbornly true for the last 30 months, and the equivalent potential EYCI price low of 407c/kg is my estimate of what this would equate to if this trend remains true.”

The peak of the US cattle cycle was November 2014 when it reached US$171/cwt, while the peak in the Australian cattle cycle was October, 2016 at 725c/kg.

The low of the US cattle cycle was October 2016 at US$95.90/cwt (a 44pc fall), which would equate to a low of 407c/kg in Australian cattle cycle terms.

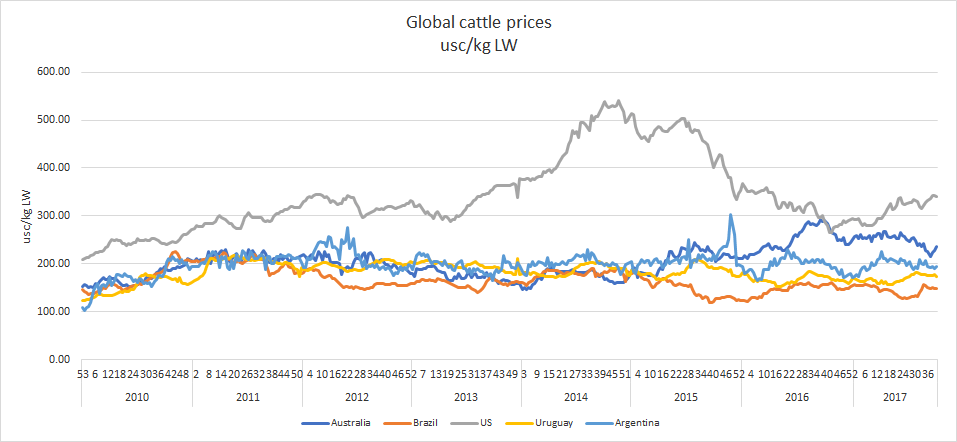

Comparing Australia with international cattle prices

Click on image for a larger view

The table above looks at comparing current Australian cattle prices with international competitors around the world, to try to answer the question of whether Australia’s cattle prices today are over or under-priced.

“The answer, I believe, is that Australia’s cattle prices are overpriced by 15pc when compared with the averaged price for US, Uruguay, Brazil and Argentina,” Mr Quilty said.

“Australia’s cattle prices should be at 460c/kg today, if they were to be in line with long term averages (these international prices have a two-week delay in them due to reporting cycles).

“What’s interesting to note is that Australia is under-priced compared to the US market – normally the long term difference is 37pc, but today we are 45pc below US prices – and given the sharp rally in US cattle prices in recent months this is not surprising,” Mr Quilty said.

“But compared to Uruguay, Brazil and Argentina, Australia’s cattle prices are overvalued by 22.6pc compared to these remaining countries.”

“When looking at the value of Australia’s EYCI today at 566.75c and where it could potentially head in the next 12-18 months, the trends outlined above continue to be sobering information for cattle producers,” he said.

Mr Quilty said the results from the analysis should be seen as a guide and not the ultimate factor in deciding views on Australia’s cattle market.

“Even the best crystal balls can get hazy or cracks can easily appear – I would always recommend seeking advice from your local agent and/or livestock adviser when selling cattle,” he said.

HAVE YOUR SAY