THERE’S been a big surge in value in grinding beef exports to the US and other key markets over the past month – and it hasn’t all been driven by Argentina’s recent withdrawal from the beef export trade.

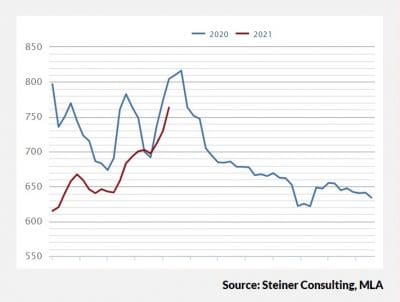

As Beef Central’s home page dashboard graph shows (see image at left), prices for 90CL grinding beef into the US last week were quoted in Aussie dollar terms at A763.2c/kg (landed US CIF), up almost 66c/kg over the past four weeks, and continuing a dramatic rise of about 150c/kg since the start of the year.

As Beef Central’s home page dashboard graph shows (see image at left), prices for 90CL grinding beef into the US last week were quoted in Aussie dollar terms at A763.2c/kg (landed US CIF), up almost 66c/kg over the past four weeks, and continuing a dramatic rise of about 150c/kg since the start of the year.

Current numbers are easily the highest seen for Australian grinding beef since the extreme, but fairly short-lived spike in demand out of the US around May last year, caused by mass closures of US beef processing plants due to COVID-related illness among workers. At one point about 40pc of US meat processing capacity was removed, either through plant closures or strict operating limitations.

An Australian meat trader told Beef Central yesterday that there were significant differences between the big price movements for manufacturing beef being seen this month, compared with the same period last year.

“Last year, the really big price rises seen for trimmings took place in US domestic supplies (caused by US meat plant closures), which caused Australian imported prices to get ‘dragged along’,” he said.

“The Australian imported prices last year rose sharply, but never got to the real extremes seen in US domestic supplies, at US300c/lb plus,” he said.

“But this year, the trend is different – price is being driven by imported supply, not US domestic. On current trends, it’s looking like imported 90s are heading towards US300c/lb.”

As of yesterday, in US currency terms, quotes on 7-45 day imported product, ex dock, were around US279c/lb FOB, up from 258c/lb a month ago and 234c at the bottom of the cycle in early March. At the height of the market spike last year, prices reached US261.8c/lb. Yesterday’s 95CL bull meat quote was at 299c/lb – now perilously close to breaking through the 300c milestone.

“We’re ahead of prices last year already, in US$ terms – but remember, this time a year ago, the $A was worth only around US65c, versus US77c this week,” the export trader said.

The all-time record high for Australian lean manufacturing beef prices was at the end of 2019, when China went crazy in purchasing everything it could find, driven by African Swine Fever impact on protein supply. That saw the market for Australian imported 90s reach US314c/lb, based on Yellow Sheet records.

The export trade contact said unlike last year’s price surge, and that in late 2019 – which were both dramatic and sudden – the price rise in export manufacturing beef seen this year had been ‘reasonably steady and constant.’

“Certainly, the recent Argentinean withdrawal from export for a month has contributed – but the current price surge started weeks before that, around late April, and in fact has risen steadily since the start of the year,” he said.

Reaction from customers over Australian lean trim price movements had been mixed, with some saying they could not buy at current rates.

“They are not committing at the moment, and that’s part of the problem,” the trader said. “They miss out this week by sitting on the sidelines, and then the asking prices look even steeper next week,” he said.

“But some very large US players in the trim have been active in the past week or so, and there are always users who need frozen imported in their mix. A lot of US plants are simply not set up to do boxed frozen trim.”

“Yes, some end-users will use as much domestic US fresh trim as they can, because domestic US fresh 90s are still 10-20c/lb behind imported equivalent in price (this week around US260c/lb), but many still need that frozen imported in the pattie manufacturing process,” he said.

Imported trim has been priced above equivalent US domestic all this this year and the tail end of last year, since Australian supply started to tighten as slaughter numbers fell.

Demand remains high, as US COVID recovery gathers pace

Despite current trim price levels, beef demand remains very strong in the US market, and especially so heading into the Northern hemisphere summer barbecue season.

“The US is getting back on its feet after COVID. Some 132 million Americans are now fully vaccinated, and close to 50pc have had one jab – so food service is getting back on its feet after the huge collapse last year,” the trade contact told Beef Central yesterday.

“So this current price increase for manufacturing beef is being driven both by growing demand – not only in the US, but also in North Asia – as well as supply constraints.”

He said all proteins – not just beef – were in strong demand in the US at present, as consumers ventured out again to eat.

“If I was a betting man, I’d say there is still more upside for Australian imported beef prices into the US in coming weeks and months,” the trader said.

“New Zealand’s (very seasonal) cow slaughter is about to run out of puff, any week, and other customers, like Japan, are also very strong on 90s currently. It’s not just a US play, with some reports suggesting US270c/lb CIF for 85s being sold into Japan this week out of Australia – virtually in line with what 90s are worth into the States. Other lesser markets, like Indonesia, are also back in the market.”

When the Argentina beef export suspension story broke last week, all Australian China-licensed beef plants apparently got calls from Chinese contacts, but apparently little business was written, based on current asking prices.

Current meat price trends in export is also helping push cow prices higher, with all-time records for direct consignment heavy slaughter cows seen on southern NSW and South Australian processor grids over the past two weeks, at 585c/kg and 595c/kg respectively.

Steak cuts at record levels

Steiner Consulting’s most recent weekly imported US beef market report suggested that US wholesale beef prices continued to ratchet higher in the past three weeks, as Memorial Day holiday demand and restaurant industry reopening has created a significant ‘bullwhip’ effect along the supply chain.

“Packers continue to be very hard-sold on a number of key items, with prices for some steak cuts now at record levels,” Steiner reported.

“Spot supply is extremely tight and small buyers that usually rely on spot market are finding it very difficult to source product.”

Limited imported beef supply and seasonal improvement in demand had caused lean grinding beef prices to move higher. On the other hand, heavy carcase weights and lack of lean beef (for blending) had caused domestic US fat beef trim prices to collapse.

Drought conditions and poor pastures were forcing some US cattle herd liquidation, implying higher beef prices longer term.

“Market fundamentals and market inefficiencies have contributed to the recent bout of beef price inflation,” Steiner said.

US cattle slaughter is not that far from where it was back in 2019, with recent weeks higher than the same week last year.

“Fed cattle weights were running as much as 5pc higher than the same time in 2019 so overall beef supplies are higher than what we saw back then. However, beef exports are also much stronger than they were back then. The announcement from Argentina that it would suspend beef exports for 30 days caught many by surprise, but it was something market was already fearing.”

Chinese buyers, which count Argentina as their second largest supplier, suddenly were very active, with more than 9000t of product booked for the week ending May 13.

US sales to China have accelerated in the last 12 months, and if Argentina decides to curtail its export program, Chinese buyers may become even more active in the US market, Steiner suggested.

Bull-whip effect

“We think another part of the reason for the sharp run-up in the value of a number of meat protein items is the bull whip effect,” Steiner said.

Familiar to supply chain analysts, the bull whip effect refers to the tendency of long supply chains to amplify the impact of real shifts in consumer demand. This can happen both in a positive or negative direction as participants along the supply chain react to anticipated changes by either increasing or reducing inventory levels along the chain.

“Imagine all the players involved in servicing a retail or foodservice operation: manufacturers, processors, distributors, re-distributors and traders. The cumulative effect of all their efforts to manage anticipated increases/decreases in consumer demand results will amplify the level of demand at the packer level,” Steiner said.

Rising COVID pressures last winter caused supply chain participants to stay very thin through January, something that was apparent in the freezer stocks reported by USDA.

“Suddenly, all those participants are now looking not just to make up for the shortfall but also build additional safety stock,” Steiner said.

“For imported beef suppliers, this should be a very important consideration as they look past the next month or two and plan for sales in the fall and winter. While we think demand has indeed improved, it is important not to confuse the bullwhip effect with actual consumer demand.”

HAVE YOUR SAY