Cattle prices could fall ten percent by the middle of next year, the Australian Bureau of Agricultural and Resource Economics suggested at its annual Outlook conference in Canberra earlier today.

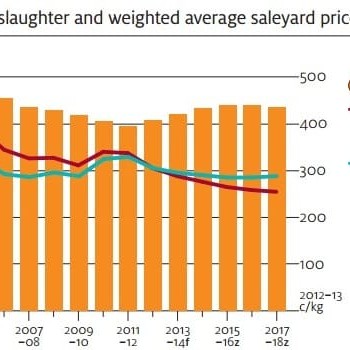

ABARES suggested the Australian weighted average saleyard price for cattle will fall 7 percent by July this year to 305c/kg, followed by a further 3pc decline to 295c/kg over the following 12 months (see graph below – article continues below graph).

A number of factors in domestic and export beef markets were likely to combine to pressure cattle prices, the economic forecaster said.

A number of factors in domestic and export beef markets were likely to combine to pressure cattle prices, the economic forecaster said.

Locally, lower demand for restocker cattle and increased supplies of slaughter cattle are expected to place downward pressure on prices for trade steers and heavy steers.

In export markets, average unit returns are forecast to decline because of lower demand for higher-value chilled cuts and increased demand for cheaper frozen manufacturing meat.

Additionally, the anticipated high value of the A$ is expected to continue to make Australian beef less competitive against products from some major competitors on international markets.

Prices of light steers and heifers in northern Australia are forecast to decline further in 2013–14, reflecting the Indonesian Government’s reduction in the live cattle import quota to 267, 000 head in 2013, compared with 283,000 head last year and 500,000 head in 2011.

Over the medium-term, ABARES suggested saleyard beef cattle prices will decline in real terms as cattle slaughter and beef production increase. Assuming favourable seasonal conditions, cattle prices are projected to stabilise toward 2017-18 as growth in cattle slaughter and beef production slows.

By 2018 the weighted average saleyard price for beef cattle is projected to be around 255c/kg in 2013 dollars.

Cattle slaughter and beef production to rise

ABARES forecasts cattle and calf slaughter to increase by 3pc this year to 8.1 million head, and a further 3pc next year to 8.4 million head.

In the short-term, the increase is expected to be underpinned by higher slaughter rates of breeding females as herd rebuilding efforts wind-down. Over the first six months of 2012–13 female cattle slaughter increased by 8pc year-on-year to 1.6m head. During the same period male cattle slaughter increased by 2pc to 2.2m head.

Over the medium term cattle slaughter is projected to increase to 8.8m head by 2017–18.

Beef and veal production is forecast to increase by 3pc in 2012–13 to 2.19m tonnes, and a further 3pc in 2013–14 to 2.25m tonnes.

In the short term, the increasing proportion of lighter females slaughtered is likely to result in beef production increasing at a slower rate than cattle slaughter.

ABARES says average carcase weights are likely to decline from the highs recorded in 2011–12 as the number of female cattle slaughtered increases, relative to male cattle slaughter.

Over the medium term production is projected to grow to around 2.3m tonnes by 2017–18.

After rising to its highest level in 30 years, the Australian cattle herd is likely to fall slightly from 2012–13 reflecting increased cattle slaughterings, particularly of breeding females. The national cattle herd is forecast to fall by 1pc in 2013–14 to 28.6m (including 25.9m beef cattle).

Over the medium-term cattle numbers are projected to decline gradually as cattle slaughter increases. Increased beef production is expected to lead to lower saleyard prices in real terms over the projection period.

Exports to rise

In the short term, ABARES expects beef export volumes to increase by 3pc in 2012–13 to 975,000 tonnes, and a further 3pc in 2013–14 to one million tonnes.

In 2013–14 Australian beef export earnings are forecast to increase to $4.72billion, driven by expected higher export volumes.

In the short-term, a mixed export performance is forecast in the three largest markets – Japan, the US Korea.

In Japan, higher supplies of US beef and low growth in consumer demand is expected to contribute to a decline in demand for Australian beef. In the US and Korea, a forecast decline in domestic beef production is expected to result in increased demand for imported beef, including from Australia.

In many smaller and emerging export markets, per person beef consumption is projected to continue rising over the outlook period, underpinning increased demand for Australian exports.

However, supplies of beef from two of the world’s largest exporters, India and Brazil, are expected to increase, leading to higher competition for Australian beef. Indian beef exports have grown rapidly in recent years and are expected to stay high in the short term, reflecting increased production and competitive pricing.

India’s largest beef export markets include many of Australia’s export destinations, such as Vietnam, Malaysia, the Middle East and the Philippines.

Brazilian beef exports are also expected to rise in the short term, reflecting increased production and improved competitiveness due to a depreciating exchange rate for the Brazilian real. India and Brazil do not hold a freedom from FMD disease status with the World Organisation for Animal Health (OIE), a requirement of Japanese, Korean and Taiwanese beef import markets.

Over the medium term Australian beef exports are projected to increase to 1.04m tonnes by 2017–18, reflecting increased demand from the US and some smaller emerging markets.

Growing competition in Japan

Australian beef and veal exports to Japan are forecast to fall 6pc in 2012–13 to 305,000t, and a further 5pc next year to 290,000t. In the short term, Japanese demand for imported beef is expected to increase, but relaxation of import restrictions to US beef is expected to result in increased shipments from the US at the expense of Australian beef, particularly higher-valued chilled and grainfed cuts.

The increase in the age limit for US beef to 30 months is likely to result in increased US shipments to Japan, with more than 90pc of US beef now eligible to be exported to Japan. Under the previous restrictions, less than 50pc was eligible.

Demand for Australian frozen manufacturing beef, unlike chilled beef, is unlikely to be significantly affected by the changed import rules because manufacturing beef from Australia sells at a significant discount to US beef.

With the value of the A$ assumed to remain high, the composition of Japanese beef imports is forecast to be around 58pc from Australia, 28pc from the US and 14pc ‘other’ in 2012–13. Australia’s share could slip to 55pc the following year, ABARES says.

The adverse impact of increased competition from US beef, particularly chilled cuts, is likely to be partially offset over coming years by a gradual strengthening in demand for cheaper frozen beef over the projection period.

Increased exports to the US

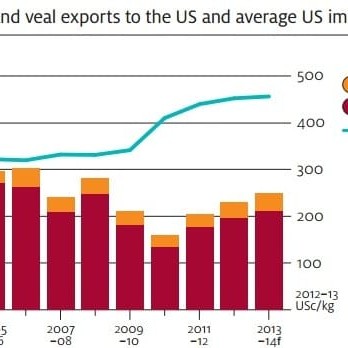

ABARES forecasts Australian beef exports to the US to increase by 12pc this financial year to 230,000t, and a further 9pc in 2013–14 to 250,000t.

ABARES forecasts Australian beef exports to the US to increase by 12pc this financial year to 230,000t, and a further 9pc in 2013–14 to 250,000t.

In the short term, increased exports to the US reflects lower US beef production and high US import prices for manufacturing beef. US production is forecast to fall by 1pc in 2012–13 to 11.6mt, and a further 2pc next year to 11.4mt.

This includes falling production of both high quality grainfed cuts and lower quality manufacturing beef. In the short term a forecast decline in US cow slaughter is expected to result in lower US supplies of manufacturing beef, resulting in increased demand for imports from Australia and NZ.

Prices of imported manufacturing beef in the US are forecast to rise by 4pc this year, and a further 3pc next year. Higher US import prices offer Australian exporters additional incentive to divert manufacturing beef to the US from other markets where shipments have fallen, such as Russia and Indonesia.

While frozen manufacturing beef will continue to comprise most of Australia’s exports to the US, shipments of chilled beef are also forecast to rise in the short term, reflecting declining supply from other major exporters.

Over the medium term Australian exports to the US are projected to increase to 275,000t by 2017–18. Strong US demand for manufacturing beef and declining domestic supplies are expected to result in higher prices in real terms for imported beef.

The US cattle herd is currently at its lowest since 1952 and is forecast to decline further over the medium term.

Growing demand in Korea

ABARES forecasts Australian beef exports to Korea to increase by 8pc in 2012–13 to 133,000t, and a further 5pc next year to 140,000t. Korean beef production is forecast to fall from its recent highs, while beef consumption is expected to continue rising, resulting in increased demand for imports.

In the short term Australian beef is expected to maintain the largest share of the Korean beef import market, despite increasing competition from the US.

The impact of the Korea/US Free Trade Agreement on exports of Australian beef to Korea is expected to be relatively small in the short term, but increasing over the medium term.

From 1 January 2013, the tariff on Korean imports of US beef was reduced to 34.66pc, compared with 40pc for Australian beef. Under the terms of the KORUS FTA, the tariff on Korean imports of US beef will fall by 2.67pc per year until reaching zero in 2026.

Assuming Australian beef remains subject to the existing tariff of 40pc, the difference in tariffs faced by Korean imports of Australian and US beef will rise to 18.7pc by 2017–18.

In the short term, it is unlikely the tariff differential of 5.34pc will significantly affect sales of Australian frozen beef in Korea, given the large discount it sells at compared with US frozen beef. However, the closeness in pricing of Australian and US chilled beef could result in growth in Australian exports of chilled beef beginning to slow.

The landed price of Australian frozen beef in Korea averaged 13pc lower per kg than US frozen beef over the first 6 months of 2012–13, while Australian chilled beef landed at an average of 6pc below US chilled over the same period.

Australian beef exports to Korea are projected to increase gradually over the medium term, reflecting ongoing growth in Korean beef consumption. If Australian beef continues to be subject to a higher tariff than US beef, growth in exports to Korea is likely to slow as US beef becomes more price competitive, particularly toward the end of the projection period.

China big growth prospect

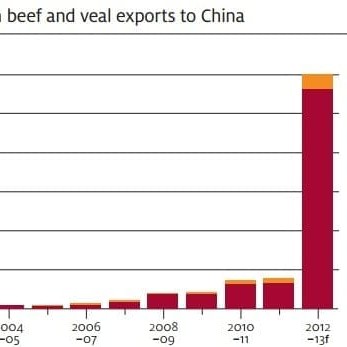

Australian beef exports to China are forecast to increase significantly this year to around 50,000t, with frozen beef comprising the majority of shipments. Monthly exports to China have averaged 6000t since September 2012, compared with 500t over the five years to August 2012.

Australian beef exports to China are forecast to increase significantly this year to around 50,000t, with frozen beef comprising the majority of shipments. Monthly exports to China have averaged 6000t since September 2012, compared with 500t over the five years to August 2012.

Increased exports to China have been underpinned by lower Chinese beef production.

Lower exports to Indonesia

ABARES forecasts Australian exports to Indonesia to fall by 32pc in 2012–13 to 26,000t, and a further 23pc next year to 20,000t, reflecting the Indonesian Government’s decision to reduce the allocation of beef import permits.

Over the medium term, the volume of exports to Indonesia depends on the trade policies employed by the Indonesian Government. Australia is likely to remain the largest supplier, ahead of NZ, Canada and the US.

HAVE YOUR SAY