While the traditional pre-winter northern hemisphere US cow reduction is now in full swing, attention is now starting to focus on grinding meat supply in March/April next year.

While the traditional pre-winter northern hemisphere US cow reduction is now in full swing, attention is now starting to focus on grinding meat supply in March/April next year.

It's a time when US domestic cow slaughter normally eases, but demand is on the rise.

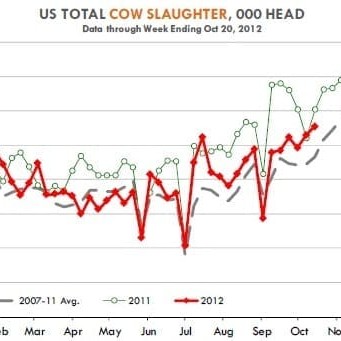

The recent surge in US cow slaughter was not unusual, analyst Len Steiner said in his weekly report on Friday. Each (northern hemisphere) autumn, producers had to decide how many cows they were willing to carry-over for the winter months.

Preliminary USDA daily slaughter reports show cow and bull slaughter is currently running at about 157,000 head – a level which has helped keep US domestic lean beef prices in check, for now, Mr Steiner said.

He estimated the cow component of that figure to be around 148,000 head per week, about the same as a year ago, but above 2010 levels.

Tight hay stocks and supplies this year due to drought was also a factor in US producer decision-making, and would continue to be so for the next three or four months.

“Those cows that don't make the cut normally go to slaughter within a tight two-month window between late-October and mid-December,” Mr Steiner said.

“Predictably, this is also the time of year when prices for lean grinding cow meat are at their lowest point in the year. Increasing cow meat supplies at a time when retailers are focused on turkey, ham and roasts equals lower prices.”

But if anything, USDA price data shows that lean grinding beef demand remains in good shape, regardless of the high level of cow kill.

Despite cow meat supplies near the highs established in the last two big liquidation years, US lean beef prices last week were running 14pc above year-ago levels, and 41pc higher than where they were two years ago.

“There are fewer cows available for marketing today than what the US had three or four years ago, and higher prices will be needed to convince producers to part with their animals,” Mr Steiner said.

Higher prices for calves out-front, given the shortage of breeders, had also changed the profitability calculations and the premiums for cows on the ground.

Prices stay firm, despite higher imports

US domestic lean beef prices remain firm (quoted last week around $2.07/lb for 90CL beef) despite higher imports of grinding beef.

US domestic lean beef prices remain firm (quoted last week around $2.07/lb for 90CL beef) despite higher imports of grinding beef.

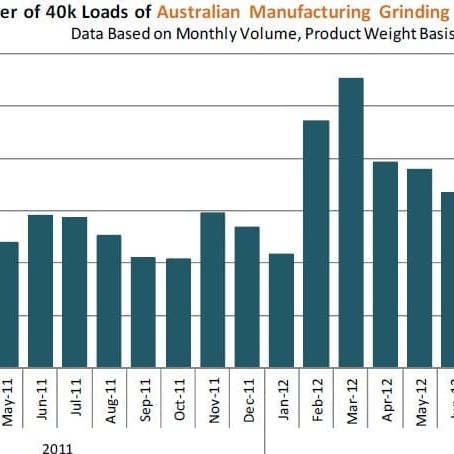

As can be seen in this graph, imported lean grinding beef shipments from Australia, the largest supplier to the US, were up 71pc in October compared with a year earlier, and in the last three months were up 47pc from last year.

Last year, imported lean grinding beef prices in mid-November were hovering around 203c (US East Coast) compared to around 210-212 last week – a 4pc premium to year-ago levels despite a net increase of +70pc in October shipments and an expected 10pc increase in shipments in November.

“Last year, US beef imports were particularly low, but the point is that US lean beef prices have been able to eke-out a 14pc gain, even as both domestic and imported grinding beef supplies have increased,” Mr Steiner said.

The main concern for US end-users, both on the foodservice and retail side, was what happens next (northern hemisphere) spring as domestic cow slaughter slows down, Mr Steiner said.

“Depending on the pace of the slowdown, which in turn will depend on pasture conditions and feed supplies, lean grinding beef availability will be a concern and we could see more fed cattle round cuts end up in the grinder,” he said.

Another key concern for the US industry in coming months is moisture. After two years of drought, US cow-calf producers will struggle this winter with tight hay supplies.

“In part this is driving the sharp increase in cow slaughter and we think there is a possibility that cow slaughter will remain high in January and February,” Mr Steiner said.

“US domestic cow slaughter should be lower in the spring as moisture improves, but as US beef cow producers transition from grass to hay, there is a fear more cows could come to market in January and February. Hay inventories are the smallest in many years and good quality hay remains a precious commodity.”

“The question is how big of an improvement will we see. Drought conditions continue across much of the US Midwest, especially the Western part in Nebraska and Iowa. It is still too early to talk about weather next summer, but it will be a key to the direction in lean grinding beef prices, especially during the summer months,” he said.

“We still think the key risk for the market is in March and April when demand picks up just as domestic cow meat supplies decline.”

Prices take toll on US exports

Meanwhile, the sharp increase in US beef prices continues to take a toll on US beef export volume.

September figures showed total shipments of US fresh/frozen and processed beef were down 12,300 tonnes or 16pc compared to a year ago. This was the ninth consecutive month that US beef exports have posted a year-over-year decline.

Limited beef supplies and the resulting high beef prices have negatively impacted US beef export volume.

Export revenues, on the other hand, remain strong and were only modestly lower compared to last year, despite the sharp decline in tonnage, CME’s Daily Livestock report suggested.

The total value of US beef exports in September was US$387m, down about 2.6pc from last year. Year-to-date, the value of US beef exports is up 1pc from last year.

Beef export volumes were lower across the board. Mexico remains one of the top markets for US beef but it has shrunk considerably in recent years, riven by a weak currency, significant food price inflation and a weak economy, forcing Mexican buyers to look for cheaper alternative proteins.

US beef exports to Japan, which has been one of the few growth markets so far this year, were about steady compared to last year. Lack of product availability, especially for high-demand items in Japan such as chuck roll and short plate, remains a concern.

Cattle age limit restrictions remain one impediment for increasing US shipments to the Japanese market, a limitation that is expected to be removed next year.

HAVE YOUR SAY