PRICES for imported lean grinding beef in the US market were very firm last week, driven by limited supplies in the spot market, growing consumer demand for grinding beef, high asking prices from Australian processors and sparser than expected offers from New Zealand.

Steiner Consulting’s weekly imported beef market report suggested the imported 90CL beef indicator increased US2c from the previous week levels, to US208c/lb CIF (up A8c, to A603.98c/kg CIF).

That’s the highest price seen, in A$ terms, since a brief spike in July last year.

That’s the highest price seen, in A$ terms, since a brief spike in July last year.

Brazil offers for the moment remain very thin in the US market, largely because the Brazilian export industry continues to wait for final USDA approval of phyto-sanitary testing arrangements. Without such protocols in place shipments from Brazil will likely remain very limited, going to cook-only facilities, Steiner said.

Prices for US domestic lean grinding beef also have been trending higher and this has been an additional recent factor bolstering the value of imported product.

“It is not unusual for US lean grinding beef to move higher into the spring, it happens every year and this year is no different,” Steiner said.

Grinding beef demand on the rise

Current prices have advanced at a faster pace in March than would normally be expected from the seasonal tendency alone.

“From discussions with market participants and also activity in other markets, our general impression is that grinding beef demand in the US is much better than a year ago,” Steiner’s report said.

This may be in part the result of warm weather in many heavily-populated US areas.

“It is not just grinding beef that is doing well at this time. From steak cuts, to chicken breasts, to pork chops and pork butts, US retail prices have increased at a faster pace than one would expect for early March,” Steiner said.

Seasonally, lean grinding beef prices in the US tend to firm into early April and then drift lower into the summer. In the last three years the price decline into May and June has been more pronounced than the seven-year average.

Other market factors

More limited offerings from New Zealand is another part of the story. In part this has been attributed to big rain across NZ this month, which has led to slower than expected slaughter.

“For now it appears that NZ suppliers are willing to offer product for May delivery but are uncertain of product availability. One would think that the delay in slaughter could lead to higher slaughter and increased availability in late May and June but, for now offerings are reportedly quite thin,” Steiner said.

The latest data available for NZ slaughter for week ending February 11 showed a figure of 52,352 head, up 14.8pc from the extremely low levels of a year ago but 7pc under the five year average. Cow slaughter for the week was 16,955 head, down 10pc from the previous year.

USDA last week issued an update of its post estimates of Australian supplies in calendar year 2017. Different from MLA estimates which use a mid-year marketing point, USDA issues calendar year forecasts so they are consistent with both US projections but also projections for other parts of the world.

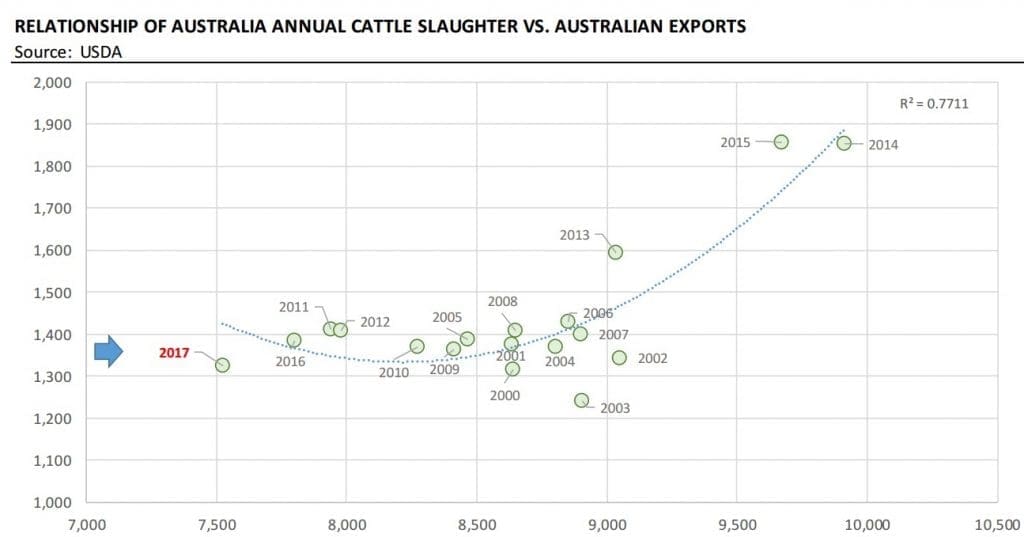

Click on graph for a larger view

Steiner’s chart published here shows the relationship between Australian slaughter and Australian beef exports, which clearly has a non-linear function.

The reason for this is the fact that domestic beef demand tends to be fairly inelastic. Once slaughter exceeds certain thresholds, the excess supply has to go entirely into export channels, hence the sharp increase in exports in 2014 and 2015.

Note the 2017 forecast at lower left. USDA’s current projection is for cattle slaughter in 2017 to be the lowest since at least 2000, estimated at 1.325 million tonnes, on a carcase weight basis. (This contrasts with Australian data which is often on a product weight basis – hence less volume).

USDA currently projects Australian beef exports to be down 4.3pc in 2017 from year-ago levels. It expects Australian beef exports to the US to drop to 320,000t (carcase weight basis), 5pc less than a year ago and 45pc lower than in 2015.

“Our opinion is that USDA forecasts are quite optimistic at this time,” Steiner said.

“Already we are seeing increased competition for Australian product in a number of Asian markets. A stronger US dollar and more beef available from South America could contribute to more Australian beef coming into the US, but during the first two months of this year the trend certainly has been for Australian beef to go to other destinations.”

Source: MLA

HAVE YOUR SAY