Source: ABARES. Click on chart to view in large format.

It’s that time of year again when ABARES’ commodity forecasters weigh up the various factors affecting supply and demand and predict where they believe cattle prices will head in the next five years or so.

As anyone knows, trying to predict price trends next week, let alone next year, is a fraught with difficulty, and in some cases a drunk with a dartboard may have as much chance of success in accurately predicting future trends as an economist crunching the numbers on market fundamentals in Canberra.

However, unforseen future market shocks aside, most would agree that the key drivers of supply and demand that tend to influence cattle values in Australia are all pointing to a stronger price picture ahead.

Certainly ABARES thinks so, predicting this morning that weighted average saleyard prices for cattle should rise year on year through until 2018-19.

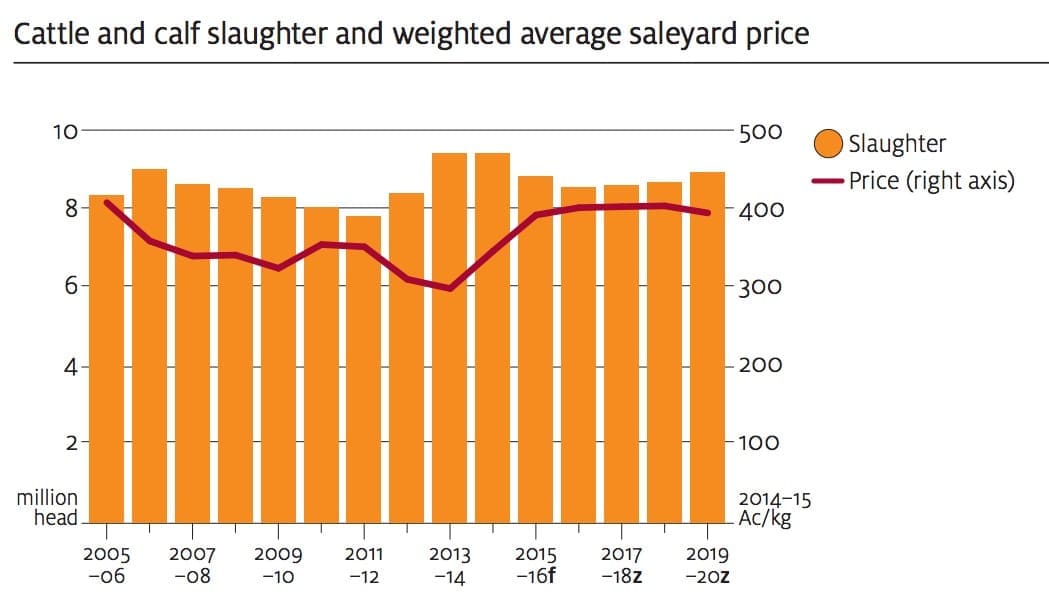

More specifically it believes the price of cattle for the current 2014-15 year will average 349c/kg (dressed weight), 19 percent above last financial year, before rising again by another 16pc next financial year to average 405c/kg dw.

“Producers are expected to commence herd rebuilding in response to improved seasonal and market conditions by retaining heifers and increasing demand for restocker cattle,” the ABARES report says.

“This will place further upward pressure on cattle prices, particularly for trade steers and medium cows.

“Additionally, strong export demand for Australian beef is expected to continue, supported by an assumed lower Australian dollar and tariff reductions in some major markets as a result of recently negotiated bilateral trade agreements.”

Cattle prices are projected to increase again in 2016–17 as herd rebuilding activities continue and cattle slaughter falls further.

Increasing international demand for Australian beef and veal is projected to keep cattle prices high in real terms in 2017–18 and 2018–19.

However, in 2019–20, with an expanded cattle herd, cattle prices are projected to fall in real terms as slaughter increases.

Slaughter trends

ABARES now believes Australian slaughter rates for the current 2014-15 financial year will total 9.5 million head, due to the continued drought-forced destocking that occurred in from July to December 2014.

During that time, slaughter of female cattle was 19 per cent higher year-on-year and male cattle slaughter was 4 per cent higher.

The high proportion of female cattle slaughtered was reflected in the fact that forecast beef and veal production for 2014-15 is expected to remain at 2.5 million tonnes, largely unchanged from the previous year.

Assuming average seasonal conditions in 2015–16, ABARES predicts Australian cattle slaughter to fall by 6pc to 8.9 million head.

Cattle numbers to fall then recover

After reaching a high of 29.3 million head in June 2013, the Australian cattle herd has dropped substantially due to the impact of drought on calving rates and forced destocking and herd reductions.

Determining the actual number of cattle that exist in Australia at any one time is a matter of informed guesswork, but for the present time at least both ABARES and Meat & Livestock Australia seem to agree that the herd is likely to total close to 27 million head by June 2015.

While calving rates are expected to recover in line with seasonal improvements, additions to the herd are likely to be offset by ongoing reductions caused by continued high slaughter rates and live exports.

As a result ABARES believes the herd will fall further from this point in 2015-16, before recovering in 2016-17 and gradually expanding in size back to the current herd size of around 27.2 by 30 June 2020.

The demand outlook remains strong, supported by a fall in the Australian dollar and tariff reductions on imports into Japan and the Republic of Korea.

The United States is forecast to be the largest market for Australian beef and veal in 2014–15, accounting for 34 per cent of total exports, compared with 22 per cent in 2013–14. Higher exports to Japan are also forecast.

Reflecting lower domestic supply, Australian beef and veal exports are forecast to fall by 5 per cent in 2015–16 to below 1.2 million tonnes, followed by a projected 3 per cent fall in 2016–17.

To read ABARES’ forecasts in more detail, click here to read the full report

HAVE YOUR SAY